Are you an investor or are you a speculator?

Way back in October 2011, I penned the following piece in The View as world share markets entered bear market territory.

The 2011 crisis had commenced in August when the US lost its AAA credit rating (some 9 years later it still has not gotten it back) and world capital markets were in turmoil as they seemed to be falling into a “Greek default” induced calamity. Many commentators at that time were suggesting that investors should sell out of the equity market with the GFC a recent memory.

The parallels with today’s headlines in the mainstream press are everywhere to be seen. The current equity market correction, driven by the coronavirus, Covid-19, has given rise to the rerun of classic headlines like “Billions wiped off equity markets”, “Blood in the gutters” and the well-worn “Panic selling by investors”. The utilisation of the description “investors” rather than “speculators” gives the impression that rational people are frantically giving up their long held investments and therefore you should too!

The economic and social disruption caused by the coronavirus will continue for many months. It cannot be dismissed as an aberration. It will result in world economic data for (at least) the first half of 2020 being very weak. Australia may well have two quarters of negative growth.

Concerns that major international events could soon be cancelled (think of the Olympics due to commence in Tokyo on July 24), that international tourism will sharply decline, that manufacturing supply lines are becoming frozen, etc, are all true and they paint a difficult short term outlook.

However, whilst I will not claim that there is never a good time to sell equities and re-allocate to other asset classes, I categorically believe that there is never a good time to panic and sell equities.

Equities (and never more so than today) offer exposure for investors to benefit from long term world growth emanating from the interaction of two structural growth cycles at present.

The first cycle is haphazard and not as robust as it used to be, but it does exist. It is the long growth cycle of the “developed world” as it now drifts in and out of mild growth, slowed by ageing populations but benefiting from two way trade with the “developing world”.

The second concurrent and more powerful cycle is that of the “developing world”. This cycle will endure for many more decades as hundreds of millions of people will steadily emerge from poverty into a better quality of life. This second cycle is propelled by trade, industrialisation, urbanisation and technological developments. This powerful cycle will periodically be checked by short-cycle downturns.

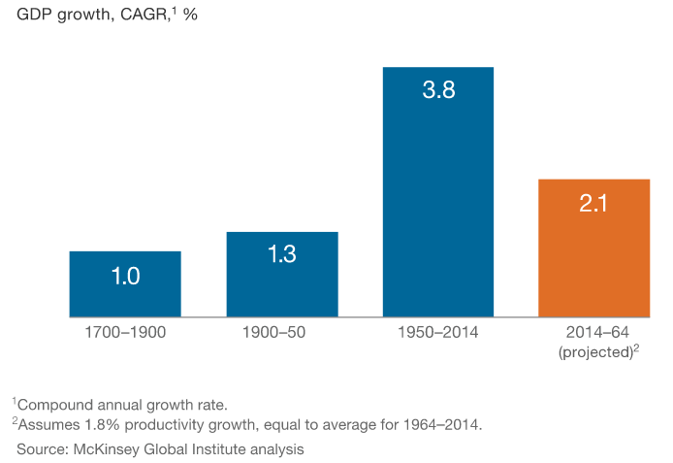

The developing world growth cycle will continue to drive the developed world cycle, so that total world growth continues to grow as it always has. Global growth will continue – albeit at a slower pace than experienced during the 64 years from 1950 to 2014, when it grew by 3.8% per annum.

The global economy is still growing, just not as fast as previously

Source: McKinsey Global Institute

Clearly the coronavirus is a serious and fast developing problem for short term world growth. It will severely check both trade and the movement of people. However, it is very likely that it will be contained, managed and ultimately defeated, as has every other confronting virus in the past, including influenza, measles, Aids, SARS, MERS, Ebola, Zika virus and many others.

If the world does not defeat the virus, then all thought processes regarding investing for the future will become irrelevant. We should all go home and spend what time we have left with our loved ones.

Source: Financial Times

Some speculation of what may happen in coming weeks or months

As always, I believe the shorter term is harder to predict than the longer term, and more so when forecasting market movements and human behaviour.

However, observations of the past, particularly the last ten years, give us clues as to what the global central banks and governments will likely do if emotion and hysteria start dominating markets.

Clearly the world’s major central banks will want to avoid a market meltdown that will in turn lead to economic recession. The central bankers have not spent ten long years printing money and manipulating interest rates so that oxygen kept flowing to markets, to suddenly give up and watch equity markets collapse.

Given that central bankers have been prepared to buy government bonds, corporate debt, mortgage-backed securities and property securities (as in Japan), why would they now decide that equities are a no-go zone?

Source: Financial Times

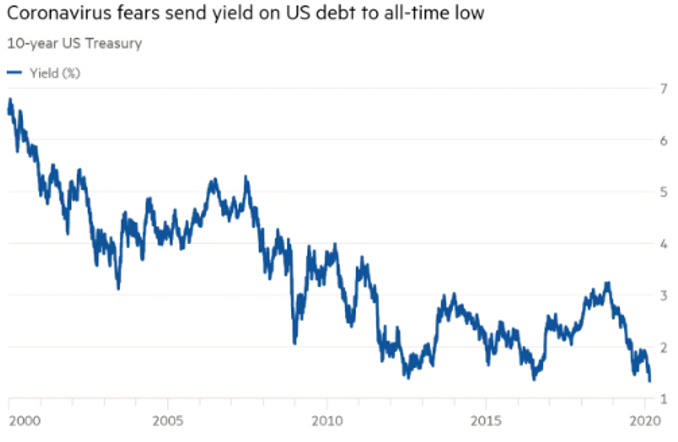

However, before central bankers intervene, they probably would regard the deflation of excessive valuations in most equity markets as desirable. A “healthy correction” may well be the collective view of central bankers, but they should be equally concerned with the excesses and illogic of major bond markets.

Whilst central bankers have caused the bond market bubble, they must surely be surprised (if not bemused) that some bond yields continue to drive deeper into negative yields. For instance, and remarkably this week, German thirty year bonds once again went into negative yield territory as coronavirus hysteria took hold of equity markets.

In thinking about the financial health of an investor, I wonder whether they will be subjected to more financial risk or stress from contracting the coronavirus or from being invested in a negative yielding bond for ten or twenty or thirty years?

Clearly as bond yields move lower, well below inflation and in some instances further into negative territory, the relative value of equities, given the long term growth trajectory of the world, becomes obvious. As equities fall in this coronavirus correction, their relative value opens. A one year decline in earnings, however significant, is still preferable to a low or negative yielding bond. More so when taking a 5 or 10 year view.

Most important in periods of panic is the understanding that equities are perpetual investments. Good quality equities will return to growth after a setback. They did that after two world wars. They did that after an estimated 50 million people died in the Spanish Flu pandemic of 1918-19. They will recover and recommence to generate profit and cashflow. They will return to paying and growing dividends. Compare this to a negative yielding bond that is not perpetual and has a return profile that if held to maturity is negative!

Markets are driven by the sentiment of people buying and selling, and they (or we) are fickle much of the time. We become more desperate and terrified as prices fall, and happy through to ecstatic as prices rise.

The central bankers know this, and they will tactically exploit this at some critical point in the future. Remember that they have proven for almost a decade that they can convince even the smartest money or asset managers of the world that negative yielding bonds are a desirable or appropriate investment for their clients.

Also, fiscal policy will swing into action and governments will use tax changes and monetary payments to stimulate or support consumers and businesses during a downturn.

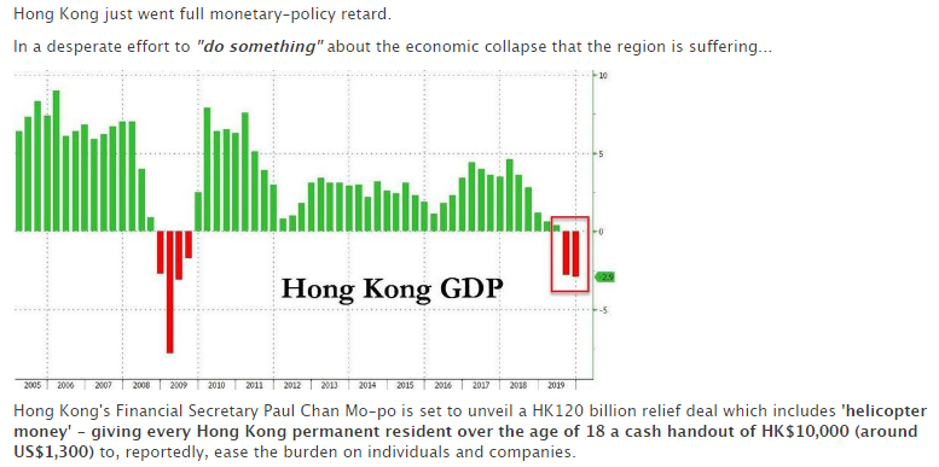

For instance, this week the Hong Kong government declared that all adult permanent residents in Hong Kong will receive HK$10,000 (A$1,950), and companies will receive a guarantee on loans taken out to pay wages and taxes. This is an example of “helicopter money” and it was previously used in Australia by the Rudd Government during the GFC.

Source: Zero Hedge

In Australia, we note that the Government has relented on its promise to produce a budget surplus in FY20. We predict that if the coronavirus continues to affect the Australian economy into the June quarter, substantial tax payment relief will be given to small and mid-sized businesses. This would help business cashflows at a time when stock levels are falling, or consumer sentiment is challenged.

There is much that can be done by sensible fiscal governance but there is little that the RBA can now do through monetary policy other than a comprehensive QE strategy to ensure liquidity is plentiful in the financial system and that banks do not restrict essential credit to mid-sized and small businesses. If there is a significant short term cashflow drain on small businesses then the RBA will need to underwrite part of the loan book of banks and that would be a sensible use of QE.

It will be a confronting few weeks and possibly months for markets. Apart from the coronavirus, the US election, Middle East tensions and the US China trade deal remain as significant unknowns. However, the likely behaviour or responses of central banks and governments in dealing with the turmoil in markets is more predictable.

Is that a reason to be bullish in the short term? No. But it is a reason to remain calm, not panic and invest logically at a time when markets are being driven by wild fear and speculation. The long term outlook for world growth looks good and that is what investors, rather than speculators need to focus upon.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities.

Clime is a management and advisory business for mainly SMSFs.

1 topic

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

John has 35 years experience in funds management and corporate advisory services. Prior to establishing Clime, John’s roles included ten years at NRMA Investments as the head of equities. Clime is a management and advisory business for mainly SMSFs.

Comments

Comments

Sign In or Join Free to comment