Profiting from a better balance sheet

Removing a company's debt burden can mark a turnaround for the share price, and in this wire, we discuss this and highlight three examples including one currently in play.

Three key risks

We always frame our idiosyncratic (stock specific) decision making around three key risks, namely operating, financial and corporate governance risks. These are the most likely risks to bring about a poor decision at the individual company level.

The one risk that we find the easiest to mitigate is financial risk (touch wood). Paying close attention to the leverage, interest coverage and debt characteristics (maturity profile) should mean no unforeseen events that derail the share price.

Often, the problem with interest cover lies in operating cash flow, or an inability to roll over debt at maturity, or as per the GFC, the world freezes up and nobody lends to anyone.

Historically stocks that are too highly leveraged trade at discounts to stocks that have appropriate gearing.

We have found many instances where the financial risk has been removed (a capital raising, asset sale, or significantly higher cash flows) the share price (equity value) will be re-rated as a direct result of the debt overhang being removed.

We have also found that companies with too much debt spend a lot of management time focusing on this issue, with cost-cutting, head count reduction, renegotiating maturity dates and often take their eye off the more strategic and arguably more important issues such as employee engagement, customer satisfaction, market share and new business opportunities. But when a company is weighed down by too much debt, it does become all-consuming, to the detriment of the future cash generation.

Three examples

We have highlighted here three examples over the past 8 years where we have (in different roles) added significant alpha (performance) by investing at the point in time when companies no longer had an insurmountable debt burden. All three companies actually operate in industries with relatively predictable cash flows (Elders does have some commodity price (cattle) exposure) while Capitol Health is a Diagnostic Imaging provider. It has high fixed costs (radiologists) but with the right staffing levels and volumes, generates predictable cash flows.

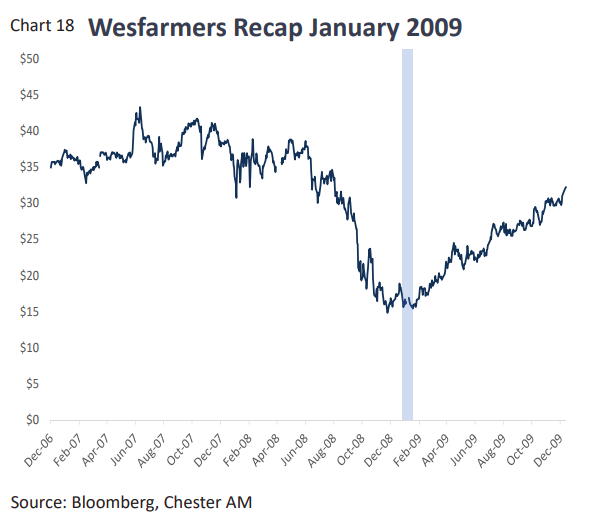

Wesfarmers

Wesfarmers raised AUD2.8bn close to the bottom of the GFC (along with many other companies), the share price did close 2009 at AUD32, or a 124% gain from the equity raising price. The gain was partly due to the imminent removal of any financial risk, and with it, a higher equity valuation, and partly due to improved operating performance at Coles and the coal division.

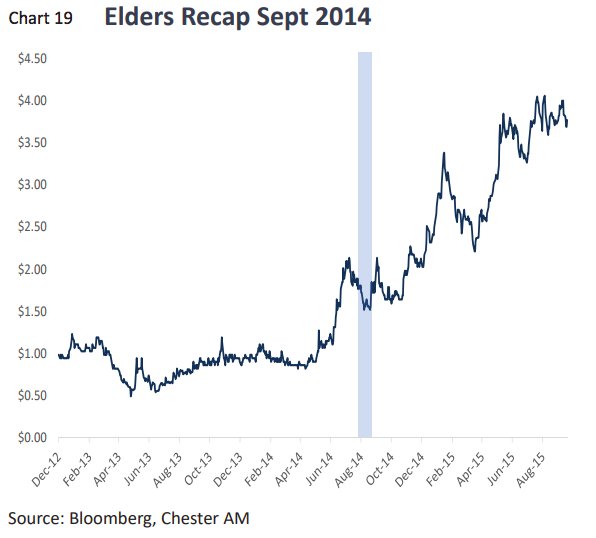

Elders

Elders Rural Services had been hamstrung for years by Futuris, particularly the Automotive and Foresty businesses, which bled cash. Selling these assets, shoring up the balance sheet and reducing corporate overheads ensured that Elders Rural Services could start competing in its core business again. The share price rose 124% from the September 2014 capital raise over the next 12 months.

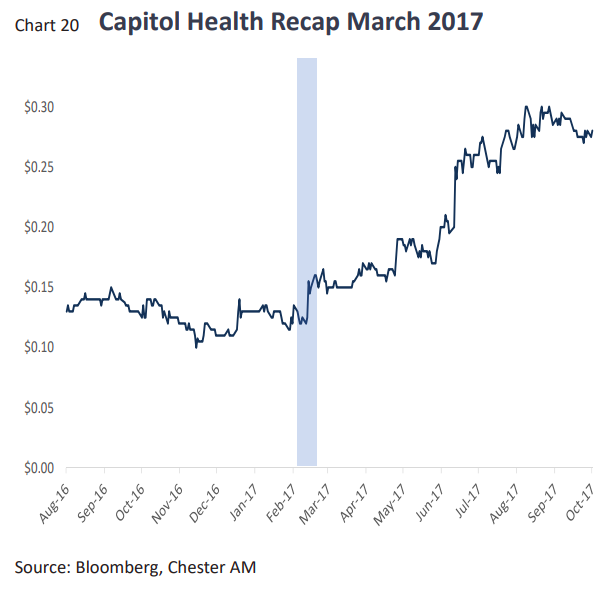

Current example: Capitol Health

Capitol Health (CAJ) had been the victim of aggressive gearing by a former CEO who went on a buying spree to gain market share. With a downturn in the industry, volumes fell as did CAJ’s ability to service that debt. Removing that debt overhang in March 2017 has seen the share price rise 100% over the past 6 months. Through an asset divestment, it is now in a net cash position with volumes looking much stronger.

One of our screens internally looks at companies that have a significant debt burden. We have a narrow subset of 4-5 stocks that look extremely interesting should they be in a position to remove this financial risk.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

3 stocks mentioned

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Rob recently founded Chester Asset Management after 7 years at SG Hiscock where he was PM of the SGH Australia Plus product that delivered in excess of 10% outperformance per annum over 3.5 years.

Comments

Comments

Sign In or Join Free to comment