Token Telstra buy-back Mark II

On 11 August 2016, Telstra announced it would return $1.5B in capital to shareholders, $1.25B in an off-market buy-back and $0.25B in an on-market buy-back. The off-market buy-back is similar in structure to the $1B 2014 Telstra buy-back. We still believe this is pretty much a token buy-back. At $1.25B it represents less than 2% of Telstra’s current market capitalisation, and so we expect the buy-back will be fairly heavily scaled back (the 2014 buy-back was scaled back by 70%). And similar to the 2014 buy-back, our estimates suggest this buy-back will likely be only significantly worthwhile for zero taxed Australian investors such as pension phase superannuation and charities, although value for taxed investors will ultimately depend on individual circumstances. For a zero taxed pension investor, we currently estimate that the buy-back will be worth approximately 8% more than selling Telstra into the market, assuming the buy-back goes off at the maximum allowable 14% discount to market price.

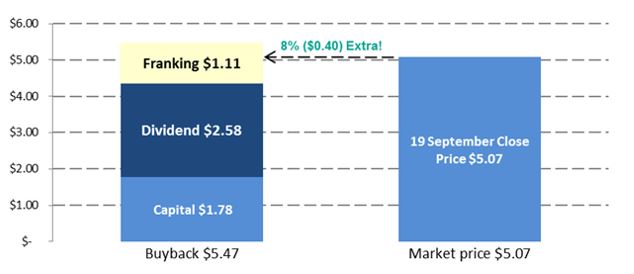

(The above is based on the September 19, 2016, closing price of $5.07 as market price – refer Chart 1.)

The actual value of the buy-back will depend on where the share price of Telstra is trading at the conclusion of the buy-back, and the final buy-back discount to that market price. In 2014 we saw the value of the buy-back decline from initial estimates, primarily because the Telstra share price declined between the announcement date and the buy-back conclusion date, resulting in a declining fully franked dividend component. On our estimates, the 2014 Telstra buy-back ended up being of marginal value (approximately 3%) for pensions phase investors, and of no value for higher taxed investors.

We recommend investors seek their own personal taxation advice.

Chart 1 provides an estimated illustrative example of the value of the Telstra buy-back for a pension phase superannuation investor. We have estimated the buy-back for pension phase superannuation funds using a $5.07 “market” price for Telstra. According to the 11th August Telstra announcement the actual market price for the purposes of the buy-back will be the “weighted average price of Telstra’s ordinary shares on the ASX as Telstra may determine in its discretion over the five trading days up to and including the date the Tender Period closes” (30 September 2016). Using $5.07 as “market” price, a 14% discount would equate to a $4.36 buy-back price. With the capital component being $1.78, the other $2.58 would represent a fully franked dividend, which would have a $1.11 franking credit attached. For a tax-exempt Australian investor, we estimate the buy-back at a 14% discount would be worth approximately $5.47 (disregarding the time value of money), representing about $0.40 or 8% more than the $5.07 “market” price of Telstra.

Chart 1. Estimated value of the 2016 Telstra buy- back for tax-exempt investors using September 19, 2016, closing price.

Source: Plato, Telstra

The value of the buy-back for other investors will depend on the tax situation of each investor. However, we normally expect buy-backs to be of most value to tax-exempt investors, so we expect it to be worth less than the 8% number for higher taxed investors. We would recommend individual investors seek professional tax advice based on their individual tax circumstances.

While the 2016 buy-back looks somewhat better that the 2014 buy-back, it still falls short relative to previous buy-backs such as the 22% benefit of the 2011 BHP buy-back. The reason why the Telstra buy-back is of lesser value to the BHP buy-back is that the capital component is quite large relative to the expected buy-back price. Notwithstanding this, given the 2014 Telstra buy-back was heavily oversubscribed, resulting in a 70% scale-back of tendered stock at the maximum 14% discount, in our view, we would similarly expect this Telstra buy-back to be heavily oversubscribed and likely to be priced at the maximum 14% discount. So while we believe it might be worth approximately 8% for zero taxed pensioners, this 8% will only be on shares which are successfully tendered.

In our analysis, we have assumed the Telstra buy-back will go off at the maximum discount of 14%. While unlikely in our opinion, if the buy-back goes off at a smaller discount, then it will be worth more than our above estimate for a pension phase superannuation investor.

Contributed by Plato Investment Management: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006.

Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street Global Advisors, responsible for over $10B in active and enhanced equity investments. Earlier he held various positions at Westpac Investment Management, including Chief Investment Officer, Head of Equities. During his time at Westpac he was also instrumentally involved in the mergers of BT and Rothschild.

Don has a strong interest in responsible investment and governance. He has a PhD in Finance and a Bachelor of Commerce with First Class Honours from UQ, and a University Medal.

1 topic

1 stock mentioned

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006. Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street...

Expertise

Don has over 25 years investment management experience. He founded Plato Investment Management Limited in 2006. Prior to Plato, Don was Head of Active Equities, Asia Pacific and a member of the global Senior Management Group at State Street...

Expertise

Comments

Comments

Sign In or Join Free to comment