Transurban: Weakness is a chance to accumulate

The now famous “toll bridge” reference to investing was made famous by Warren Buffett. This is not to say that you should literally invest in a toll bridge, but rather in the type of investment that works much like one. They make great growth investments when you can find them at the right price.

As the name implies, if you are heading along a toll bridge or road, and you come to the toll stop, you must pay it. And if this bridge or road makes life easier for folks, well, you can expect them to pay the toll on a regular basis.

We view Transurban as such an investment. The company boasts an impressive suite of toll road assets along with an impressive pipeline. In Australia in particular, Transurban is truly in the box seat when it comes to financing, planning, constructing and managing these essential infrastructure assets as federal and local governments struggle to balance their already overstretched budgets.

The company recently expanded its capital base by $1.9b via an equity raising supplemented with additional debt facilities to be in a position to fund the planned West Gate tunnel project in Melbourne’s West as well as providing further balance sheet flexibility. Transurban also recently released its 1H 2018 results, another solid performance

First Half 2018 Results

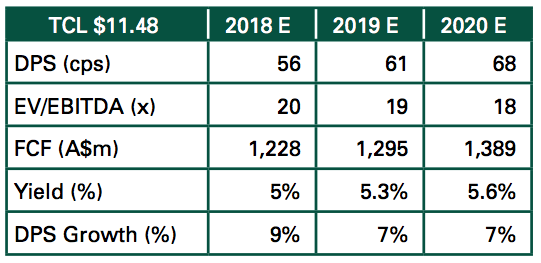

TCL delivered on low double-digit earnings and cashflow growth in 1H18 and reaffirmed the FY18 dividend guidance of 56cps (up 8.7% on the pcp). We are expecting the company’s portfolio and development pipeline to deliver a minimum 7% growth pa (a conservative estimate we believe) in distributions to shareholders.

EBITDA growth of 11.6% was another impressive result with the Melbourne assets in particular the standout – 17.5% growth. Brisbane and Sydney were a bit softer with 3.6% and 10.3% EBITDA growth – fee revenue issues, slower revenue growth and higher than anticipated costs on the M2 and M7 cited as the causes. We simply view this as room for upside at the year end. TCL’s definition of free cash flow of 28.3 cps beat consensus estimates by about 6%, fully covering the 28 cent distribution.

Capital investment & funding

TCL expects to contribute ~$6.3b of capital across FY18-22 on committed growth projects with peak spend across FY18-19 (~$3.5b). Beyond this, the pipeline of potential investment opportunities across its markets remains solid (in particular the USA, Maryland).

The next major opportunity being NSW Governments 51% WestConnex selldown (unconditional bids due mid-2018). The company continues to demonstrate its investment discipline, long-term investment horizon, and core skills. Post the 1H18 capital raising we view TCL’s debt capacity for further investment as strong, with 10% funds from operations to total debt ratio well above the 7.5%-8.0% required by S&P for its BBB+ credit rating.

Share Price Trading & Outlook

Many in our market have labelled Transurban as bond-like or a bond proxy. That is to say a rising interest rate environment will equate to a negative effect on share price performance. While some of this is true we believe sporadic weaknesses in the TCL share price off the back of interest rate expectations is simply another opportunity to accumulate the stock.

The company has a demonstrated ability to provide long-term reliable, growing cashflow and distributions to its shareholders over the life of its toll road concessions - estimated at approximately 30 years. TCL is also in the box seat to continually extend these concessions as a bargaining chip during negotiations with State and Federal governments (here and in the US).

We view the $11.48 share price as inexpensive given this outlook and risk profile with many analysts in the market providing $14+ share price targets.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

1 stock mentioned

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Trusted and Confidential Asset Management Advisors

Founded in 2003, Leyland Private Asset Management is an independently owned firm specialising in Australian Stock Market and Fixed Interest Investments for individuals, companies, self-managed super funds, institutions and family offices.

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Why my mum might help pop the CBA bubble

Elston Asset Management

Equities

Is the end of globalisation the end of global equity investing? The follow up...

Arteqin Capital Limited