Turbocharged transformation: Picking the winners of the digital revolution

Several long-term winners can provide investors with access to the digital transformation of enterprise businesses – a multi-decade structural trend turbocharged by the pandemic.

As the American proverb goes: “The only difference between stumbling blocks and stepping stones is how you use them.” While investors have faced a once-in-a-century stumbling block at the hands of COVID-19, the pandemic may prove to be a stepping stone to significant investment opportunity.

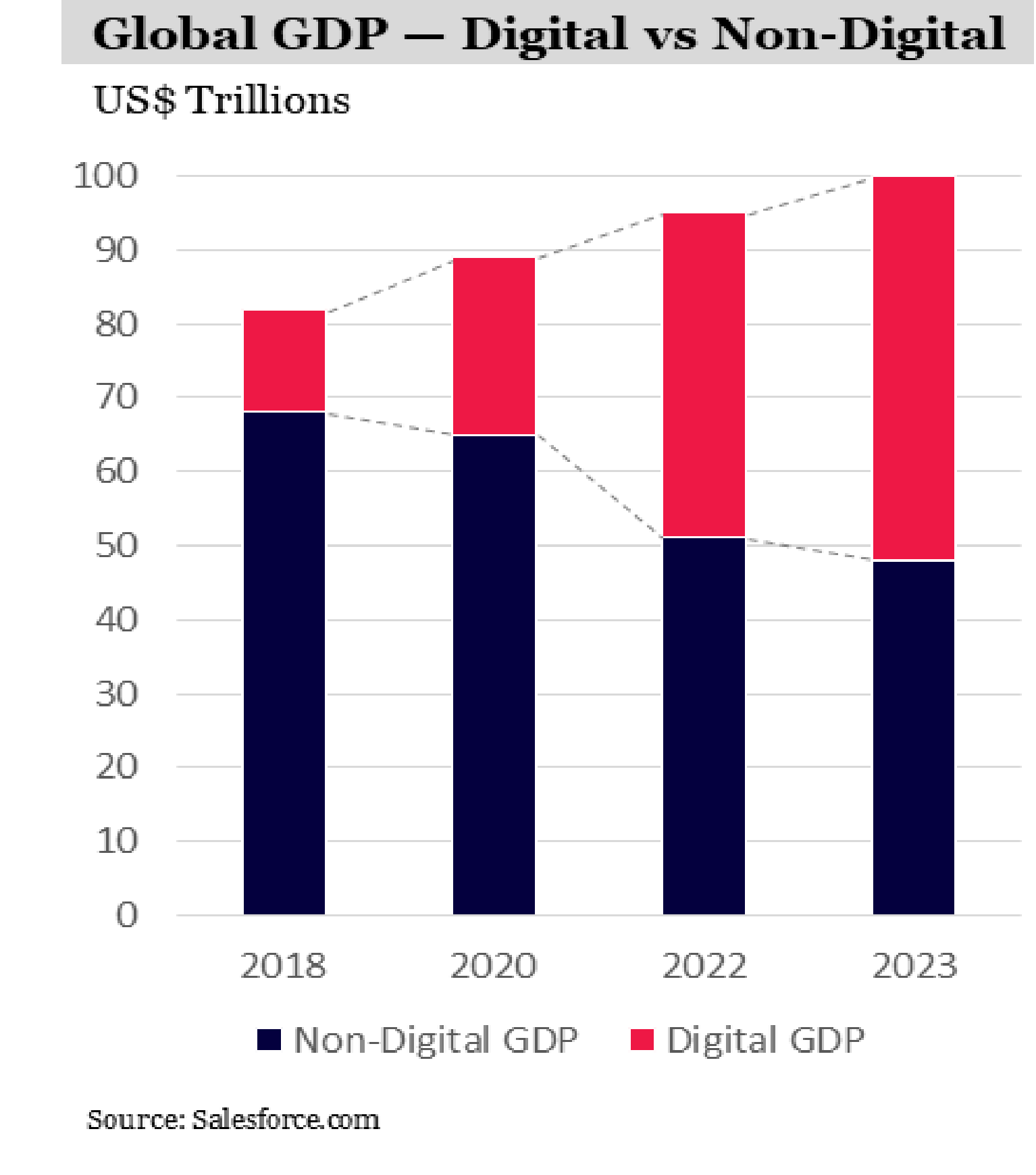

Every business is now a technology business. This was a fringe view just five years ago and yet is exceedingly ubiquitous today. Leadership teams in businesses from all industries and around the world now understand the benefits of cloud-based technology infrastructure and software-based applications that can be purchased in a scalable way as services.

As part of this, businesses understand:

- The need to leverage their data in sales, marketing and customer service functions.

- That systems must be scalable and work seamlessly across multiple devices, and for employees who could be located anywhere in the world.

Customers are increasingly demanding more too: retailers need to sell effectively across multiple digital channels. And businesses of all varieties are increasingly interacting with their customers via chat (bots). This list is nearly endless. And this was before the world was struck with the COVID-19 pandemic.

In a matter of weeks, entire workforces needed to work from home. Demand for digital collaboration tools skyrocketed. One of the category leaders, Zoom, peaked at more than 300 million daily meeting participants, compared to just 10 million in the months prior. The US News and World Report noted that Zoom is being used in 96% of top US Universities as entire college campuses made the shift to online classrooms.

Microsoft Teams grew to 75 million daily active users, up from 20 million at year-end 2019.

Likewise, Tencent’s enterprise communications app WeChat Work served 250 million monthly active users in May, up from just 60 million pre-pandemic.

It is beyond dispute that the digital transformation of the enterprise is a structural trend that has recently accelerated. And we remain in the early innings of this trend.

As ServiceNow CEO, Bill McDermott, said late last year: “Cloud is a once-in-a-generation technology that allows you to get significant improvements in user experience, in speed and agility, in efficiency, in productivity and compliance... Cloud today feels to me like mobile felt in 2012, we are about one-third of the way into this.”

And not all structural trends are created equal. This particular structural trend is:

- global, not local

- dominated by software – the economics of which are extraordinarily favourable (essentially zero marginal cost of reproduction and distribution

- leverages the power of large pools of data to create valuable network effects.

Furthermore, there are a small number of businesses in this space that have developed complete ecosystems. These have positive network effects and advantages in scale, data and M&A.

We have previously examined these characteristics in significant detail in our 2017 white paper: Who are the businesses of the future?*

The combination of an established ecosystem business model, within this accelerating, global, economically favourable trend, provides investors with compelling opportunities. And this is especially true in the context of an interest rate environment that will likely remain subdued for a long time. We examined why this is the case and the resulting implications in our 2019 white paper: Low Rates, Assets Inflate*

Mission critical ecosystems...

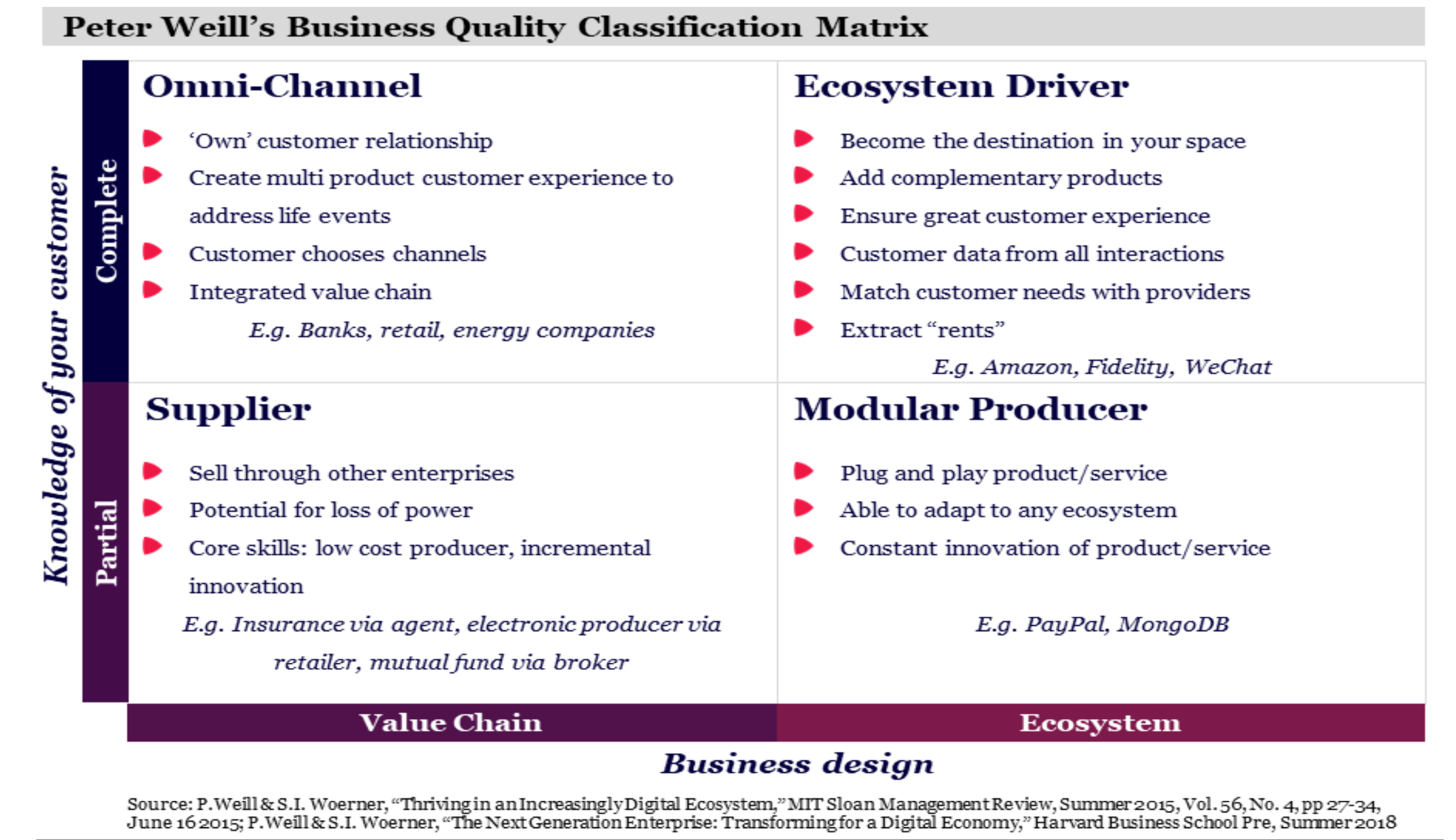

Five years ago, Peter Weill and his colleague at MIT Sloan School of Management conducted research into the impact of digital transformation on businesses and made an insightful discovery: in a period of digital disruption, businesses that focussed narrowly on linear value chains were at a disadvantage, and those that thought more broadly about their business ecosystems were more likely to be successful. Specifically, those businesses that he identified as “Ecosystem Drivers” were most likely to be the long-term winners. Weill, an Australian and chairman of MIT’s Center for Information Systems Research, developed a framework to categorise companies by business model. The framework places companies on a two-by-two matrix.

The vertical dimension represents knowledge of the end customer, and the horizontal dimension represents business design, ranging from being part of a value chain to participating in an ecosystem to solve customer needs.

Companies can then be viewed as belonging to one of four business models:

- supplier

- omni-channel

- ecosystem drivers

- modular producers.

Suppliers have a partial knowledge of the end consumer and operate in the value chain of another powerful company. For example, electronics goods producers that sell through retailers. As digital transformation makes discovery and distribution easier, suppliers are likely to lose power and prices come under pressure. Suppliers need to move to an omnichannel model to survive and prosper.

Omni-channel businesses reach customers across multiple channels with multiple products and provide a seamless experience – they “own” the customer relationship and control an integrated value chain. Omni-channel operators, like banks, invest to gain better knowledge of the life events of their customers. This means establishing relationships with other suppliers that complement, or even compete with, their own services.

Ecosystem drivers become a destination for customers to solve a life or business need in a domain and extract “rents” from other members of the ecosystem. Companies like Apple and Google are successful ecosystem drivers.

Modular producers provide products and services that adapt to a variety of ecosystems. Unlike ecosystem drivers, however, they do not see all the customer data. This means they operate in a hypercompetitive environment and need to continually innovate and provide value for money to succeed. The few successful modular producers, like PayPal in digital payments, make significant profits while the rest struggle to survive as commodity players.

Weill’s research showed a statistically significant difference across the four quadrants when it came to four key performance measures. These included two financial measures – growth and profit margins – and two measures for future performance – customer experience and time to market.

Weill found that companies that generated more revenues from managing ecosystems and that have better customer knowledge tend to perform better.

Ecosystem drivers were the dominant outperformers with 32% higher revenue growth and 27% higher profit margins than their industry averages; modular producers were more profitable and grew quicker than omni-channel companies; and suppliers were weakest in all categories.

Weill’s research has strong implications for investors. While most companies today view themselves as controlling or participating in a value chain, digital transformation is pushing enterprises “right and up”.

Digital disruption is causing threats to traditional business models, but is also part of the solution. The journey of digital transformation provides the opportunity for companies to improve their end customer knowledge with improved data collection and analysis; and, to assemble a web of relationships to provide wide-reaching solutions with interfaces that integrate services between partners and applications that tie these together for customers.

This framework is instructive to evaluate the differences in businesses and understand how they can succeed in a digital world. In seeking to identify the long-term winning businesses, we would add two additional dimensions:

- the degree to which the service offering is mission-critical in the eyes of the enterprise customer

- the degree to which there are viable competing offerings and the associated ease with which enterprise customers can switch. Learning from Montaka’s interviews of technology executives in a wide range of enterprises, there are a number of core technology building blocks to any large organisation which are truly mission critical.

While by no means exhaustive, a summarised list would include:

- Data infrastructure and networking – the core compute, storage and digital communications upon which all enterprise applications sit;

- IT service, operations and asset management applications – the applications used by IT departments to manage the IT systems and assets of the enterprise;

- Enterprise resource planning (ERP) applications – the back-office applications that house all company finance, HR and operational data

- Customer relationship management (CRM) – the applications used by the sales and marketing teams to manage customer relationships, drive marketing campaigns and deliver customer service.

- Productivity applications – the applications used by employees on a day to day basis to do their basic roles (email, messaging, videos, documents, spreadsheets, etc). The concept of a building block being mission-critical within the enterprise carries with it important implications for the quality of its related cash flows.

Think of the expense incurred by a large multinational enterprise for, say, its ERP system. As a percentage of the revenues of the enterprise, the expense is immaterial. And yet, without the ERP system, the enterprise could not perform any of its accounting, finance, ordering or invoicing functions. Through this lens, this expense will likely be unaffected no matter the economic conditions in which the enterprise finds itself. It is effectively a senior claim on company revenues. Other more junior claims, such as marketing spend or labour expenses, will be cut first in times of economic distress. Furthermore, when there is a significant mismatch between the value added by a mission critical building block; and the amount it costs, there is logically an opportunity to expand pricing in various forms. This could include new add-ons, as well as straight increases in like-for-like pricing.

Take ServiceNow, for example, which dominates the IT Service and Operations Management space for large enterprises globally. It is the mission critical platform upon which the IT department manages all of the infrastructure, applications and IT processes across the enterprise. Its largest clients pay more than US$20 million per annum in subscription fees – but these fees are in the context of an annual IT budget of more than US$8 billion. Its value-add is arguably orders of magnitude higher than its cost to the enterprise.

...with limited competition

High switching costs and limited competition are key ingredients for winning over the long-term in this attractive space. High switching costs are typically driven by a number of factors, including:

- critical data or machine learnings that are trapped on the incumbent system and cannot easily be transferred to the new system;

- potentially large costs and risks associated with transferring to a new system

- user habit and familiarity with incumbent systems.

While high switching costs ensure the long-run security of business for vendors, it is this recurring business in the context of limited competition that helps ensure the expansion of the value that be extracted over time.

The more competitive a space, the greater the degree of price competition that will likely build over time. We note, for example, that Salesforce is the clear market leader by a long margin in CRM. ServiceNow is the clear market leader by a long margin in IT service and operations management. In ERP, the space is dominated by SAP and Oracle.

It is particularly powerful for these mission-critical enterprise building blocks to be delivered under a software-as-a-serivce, or SaaS subscription model. This model is here to stay. There is enormous value to an enterprise CIO in being able to add services immediately and simply with little more than a credit card. These services can scale up and down based on the CIO’s requirements and, by definition, the software is always the current, up-to-date version in the marketplace from the vendor.

From the vendor’s perspective, the SaaS model creates a cash flow stream that is highly predictable, recurring and – for a vendor of mission-critical enterprise software with high switching costs and limited competition – highly resilient and durable under substantially all economic conditions. This speaks to the very high quality of these cash flows and raises genuine questions for the appropriate discount rate investors should apply when valuing these cash flows.

The appropriate discount rate to be applied to any investment has two parts:

- a base rate based on the concept of a risk-free rate

- a spread, based on the variability of those cash flows in a range of economic conditions.

As we see it, there are strong arguments to suggest that, in the current environment, there is downward pressure on both of these components for businesses including ServiceNow, Salesforce, SAP and Microsoft. And for context, the valuation impact of reduced discount rates on these rapidly growing businesses is very significant: every two percent reduction in appropriate discount rate, for example, adds in the order of +50-70% in value.

Finally, there is one very important attribute that increases the probability that the winners of today continue to win in the future: their access to data. Privileged access to data creates an enormous opportunity for incumbents to leverage and to expand their advantages.

Artificial intelligence, analytics and security are all forms of valuable add-ons to enterprise customers – and all require extremely large quantities of wide-ranging data in their development. It is this data that is the scarce resource in this equation – the sort of data that today is available to those which are dominating the enterprise landscape, such as Amazon, Microsoft, Alphabet, Alibaba, Salesforce, ServiceNow and SAP, to name just a few.

This access to large pools of valuable enterprise data carries with it option value, or opportunities to create new revenue streams. We believe these options will increase in value substantially over time and are often overlooked by investors today.

We believe the digital transformation of the enterprise is a prospective, structural trend that is now accelerating as a result of COVID-19. Within this trend are a number of attractive markets with high barriers to entry and limited competition. Identifying and investing in the long-term winners of these attractive markets is an opportunity worth considering.

Compound your wealth over the long-term

Montaka Global Investments provides investors the opportunity to compound wealth over the long term through disciplined global investment strategies and a sophisticated approach to risk management. Click ‘FOLLOW’ below for more of our insights.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Andrew is responsible for managing all investments at Montaka, including the ASX-quoted Montaka Global Long Only Equities Fund (ticker: MOGL) and Montaka Global Extension Fund (ticker: MKAX).

Expertise

Comments

Comments

Sign In or Join Free to comment