United Kingdom: Forgiving market

The United Kingdom has become a particularly fertile hunting ground for the Forager International Shares Fund in a Brexit-tainted world. Six of the Fund’s 10 largest positions are listed in London. Two of those have businesses that are entirely domestic facing, two are more global in nature and the remainder listed in London but with all their operations elsewhere.

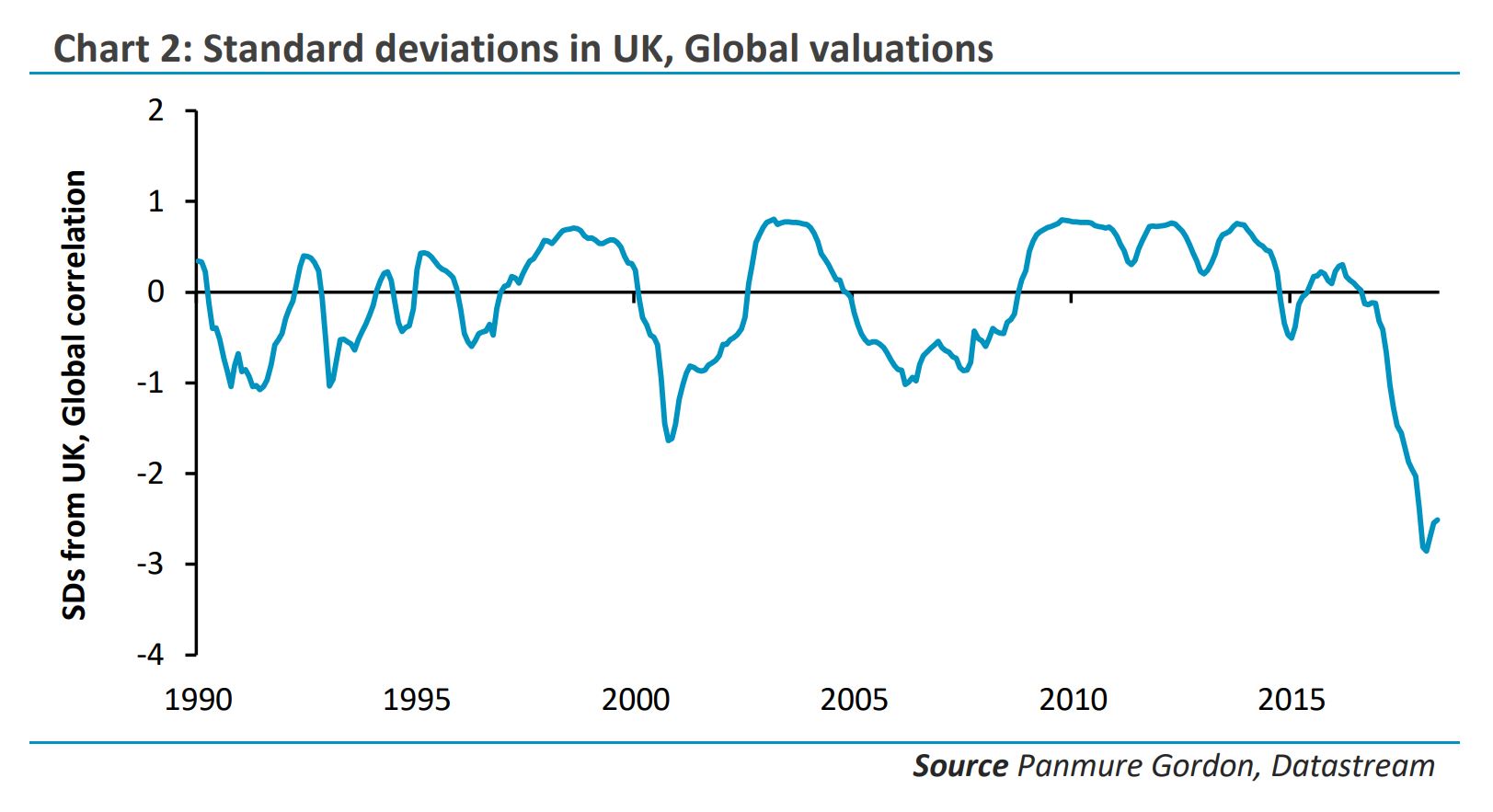

Broker Panmure Gordon recently published the below chart. On a blended average of three valuation metrics—Price to Earnings, Price to Book Value and Enterprise Value to Earnings Before Interest, Tax, Depreciation and Amortisation—the UK market is unusually cheap compared with global averages. Three standard deviations cheap in their telling.

Gentlemen should never blog about standard deviations, but I’ll make an exception today. Panmure's numbers suggest that 99.85% of the time the UK market is less cheap (in comparison with the rest of the world) than it is today. While such specificity deserves scepticism, we agree with the sentiment.

Markets like this set the scene for pleasant surprises.

Not disappointing = outperforming

We’ve all seen situations where price has gotten ahead of value. At such times, a company might report 25% earnings growth but if the market expected 27%, the stock will sell off sharply. Think of it as an unforgiving market.

The UK has already been through all that, and significant disappointment is already ‘baked in’. So the situation becomes almost the opposite. Let’s call it a forgiving market.

Babcock International Group (LSE:BAB) is a Fund top 5 position, we’ll explain its investment merits in the June 2018 quarterly letter. Babcock reported full year results three weeks ago - 3% revenue and earnings growth. They lined up with modest broker expectations as well as our own. The stock is up 13% since.

Another top 5 position is Auto Trader Group (LSE:AUTO)—see the March 2018 quarterly for a detailed discussion of the investment thesis. Its full year results, released last week, also largely met expectations. Actually several brokers referred to the result as 'mildly disappointing', then upgraded. The stock is up 19% in a week.

Blancco Technology Group (LSE:BLTG) is an illiquid stock we'll discuss at our coming roadshows and in a future quarterly report. The market set it a pretty short and simple list of demands in recent months—appoint a good new CEO to replace the one fired nine months ago and release some half-yearly results on time. It delivered. The stock is up 34% since mid-March.

When expectations are low, not disappointing is itself reason for celebration. Not delivering fresh bad news is enough impetus for the market to lift its boot off the head of a good company with a languishing stock price.

I’m not sure whether I’m 80%, 97.5% or 99.85% confident of good results from our UK positions. But recent market action confirms it’s been the right place to be focusing attention.

Further insights

If you are interested in receiving the Forager monthly and quarterly reports, please register here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Gareth Brown is a Portfolio Manager at Forager Funds Management, with a focus on researching European stocks for the Forager International Shares Fund.

.jpg)

.jpg)

Gareth Brown is a Portfolio Manager at Forager Funds Management, with a focus on researching European stocks for the Forager International Shares Fund.

Expertise

Gareth Brown is a Portfolio Manager at Forager Funds Management, with a focus on researching European stocks for the Forager International Shares Fund.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management