US Rate hikes coming, bond moves won't be what you'd expect

Going into expected US Fed rate hikes, most investors would assume that long-dated bonds will likely sell off considerably. Contrary to what popular media commentary would suggest, long-dated bonds are unlikely to move very much at all. In fact, history suggests that long-dated bonds often rally once the Central Bank actually hikes rates. Like the stock market, prices of bond securities move in expectation of future outcomes. History suggests that total return damage to bond portfolios (along with yield sensitive growth assets) largely occurs before the rate rising cycle.

US Rate hikes are coming, but bond moves won't be what you'd expect

US Federal Reserve members (Fed) have been increasingly hawkish in supporting a near-term interest rate rise in the US. Fed commentary has moved up significantly, and JCB now expects the Fed to hike US rates in March and again in June (assuming Marine Le Pen doesn't win the French election and create additional market anxiety).

Going into these expected US Fed rate hikes, most investors would assume that long dated bonds will likely sell off considerably (or, at least, that is what the press and bond bears would lead some to think). Contrary to what popular media commentary would suggest, long-dated bonds are unlikely to move very much at all. In fact, history suggests that long-dated bonds often rally once the Central Bank actually hikes rates.

As a bond (and thus interest rate) specialist manager, JCB thinks it is worth noting to investors that what you 'may' expect is highly unlikely over the medium term.

Like the stock market, prices of bond securities move in expectation of future outcomes. History suggests that total return damage to bond portfolios (along with yield sensitive growth assets) largely occurs before the rate rising cycle. The expectation of rate hikes (late in the economic cycle) is bad for long-dated bonds, REITs, etc. at the point where expectations (vs. realisation) hits and not the other way around.

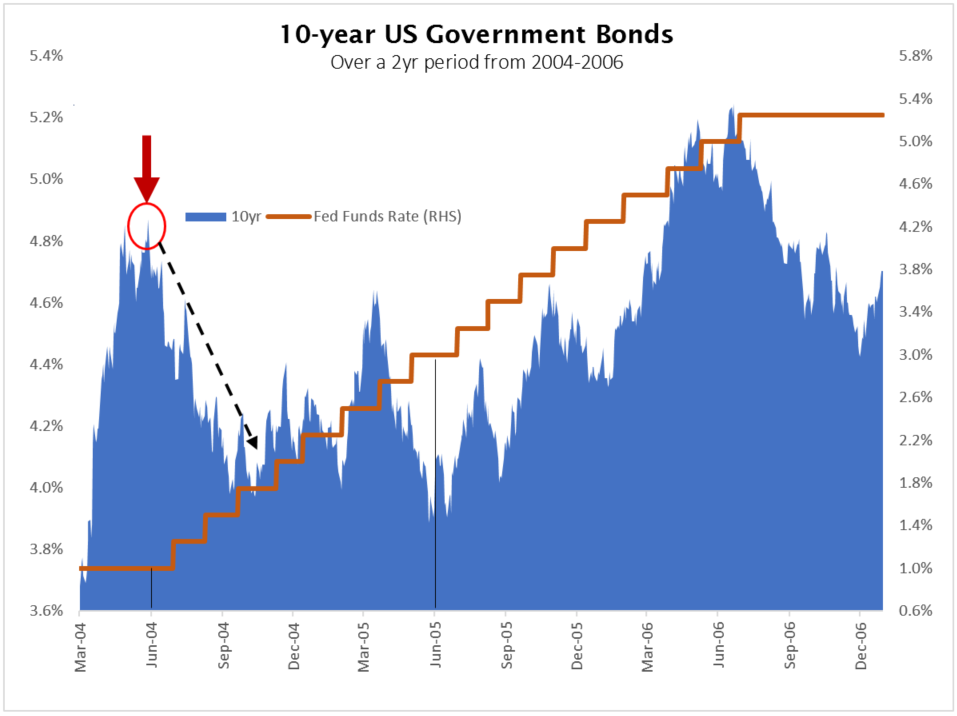

The last complete Fed hiking cycle was between 2004 and 2006. Over that two-year period, the US Federal Reserve raised rates by +4.25% (i.e. 1.00% to 5.25%). However, contrary to what an average investor would expect, the yield changes on ten-year US Treasuries was +0.37% (i.e. 4.87% to 5.24%).

What is most illustrative of our thesis is that US 10-year Treasury yields peaked before the first rate hike on 2004 and went on to rally through 2004 for a capital return of 8%. This was in spite of the Fed hiking short-dated rates.

This is important for a number of reasons:

1) Total return damage to bond portfolio's and yield sensitive growth assets tends to occur before the first hike, as seen above.

2) Expectation (vs. actual) rate hikes (late in the economic cycle) is bad for long-dated bonds, REITs, etc. We experienced much of that in Q4 last year after Trump's election.

3) Realisation (actual) rate hikes are often neutral to positive for the long end, as seen in in the chart below, where ten-year bonds rallied 99 bps outright early in the hiking cycle from 4.87% to 3.88% in mid-2005.

Image source: Jamieson Coote Bonds

4) As a Central Bank crosses neutral rates (where rate hikes restrict the economy), asset impact is usually transferred to growth assets (i.e., equities, etc.long dated).

Jamieson Coote Bonds believes that further capital long-dated bonds are unlikely to be anywhere near the magnitude experienced in Q4 last year after Trump's election as expectations are now largely priced in.

In fact, JCB believes that most highly sophisticated bond investors are considering the asset class as a tactical asset allocation in the short term given the significant improvement in valuations. Sophisticated investors with diversified portfolios will hold a cornerstone allocation to high-quality bond securities of various maturities. Warren Buffett's recent Berkshire Hathaway update highlighted a large holding of ''cash and equivalents such as Government Bonds.''

Interest rates are the virus that effects all asset classes. Jamieson Coote Bonds believe that we are quite late cycle for growth assets to behave in a way that suggests avoiding having a cornerstone allocation to a high-grade portfolio of defensive bonds that protect portfolios during times of market turmoil (or any severe growth/equity market sell off).

Sources: JCB Analysis

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

3 topics

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

Expertise

Angus established Jamieson Coote Bonds with Charlie Jamieson in 2014. He started his career with JPMorgan in London, before working at ANZ and Westpac, where he transacted the first ever Australian Bond trades for several large Asian Central Banks.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management