Value opportunity emerging in listed infrastructure

The combination of infrastructures attractive fundamentals, long-term structural growth opportunity, the COVID-19 response and beaten-down stock prices following the March equity correction represents a "unique" buying opportunity for listed infrastructure, according to Sarah Shaw, Founder of 4D infrastructure.

The relative attractiveness of listed infrastructure is highlighted by the widening rift between listed and unlisted valuations in the infrastructure sector, she says.

There has long been discussion in the market about the relative volatility of listed infrastructure assets compared to their unlisted peers. Interestingly, Shaw notes that over short-time frames the correlation between listed and unlisted valuations is often very low when comparing like-for-like assets.

However, over longer periods the correlation has proven to be higher as a function of listed equities being priced daily versus unlisted valuations which are adjusted less frequently, as well as some subjectivity allowed by managers/valuers of unlisted assets.

Image: Sarah Shaw, CIO and Global Portfolio Manager, 4D Infrastructure

4D invests in infrastructure globally and splits the market into two categories:

- Essential services - such as gas, power and water services, which are relatively immune to the macro environment

- User-pays assets - such as airports, toll roads, railways and ports, which capture GDP growth via volume

COVID-19 has caused equity markets to fall by an average of around 20%, with listed infrastructure indices down a similar amount, but hard-hit user-pays stocks such as Sydney Airport (ASX:SYD) and Auckland International Airport (ASX:AIA) have lost one-third of their value.

Yet Shaw points to major super fund UniSuper’s recent move to cut the value of its unlisted assets (which include Brisbane and Adelaide airports) by 6% while this figure was 7.5% for AustralianSuper.

So, which is the better indicator?

“We believe the real fundamental valuation impact on these assets of the COVID-19 pandemic is more closely aligned with the unlisted valuation shift.”

“Completely oversold”

Essential services offer relative earnings resilience in weak economic environments so should be an obvious defensive choice yet have been sold off in line with markets.

By contrast, while there is clearly a significant near-term earnings impact for user-pays assets due to the pandemic, Shaw says the fundamentals suggest the listed market has completely oversold these assets on what 4D considers to be a short-term shock.

Take Sydney Airport as an example. The grounding of flights has an immediate impact on revenues and, given airports are a high fixed-cost business, the impact to the bottom line is even greater. But she argues that a one-year earnings hit for a 70-year duration asset like Sydney Airport does not imply a ~35% reduction in intrinsic value.

While the skies may be clear and roads empty today, make no mistake: COVID-19 will not disrupt our wanderlust to see new cities and places; structural thematics supporting travel will “re-assert” themselves when the economy eventually normalises, Shaw says.

Illustrating the long runway for growth ahead, she cites the CEO of a Chinese travel company who last year presented to the World Economic Forum that around 9% of Chinese citizens (120 million people) have passports, and that number could double by the end of 2020. As incomes boom in China and emerging markets, so will their mobility and this COVID-19 is likely to be a blip in the bigger picture.

“We believe the long-term structural opportunity for airports remains intact and very strong – traffic will recover and with it, earnings and we believe this widening value disconnect between listed and unlisted valuations represents a significant opportunity for listed infrastructure investors.”

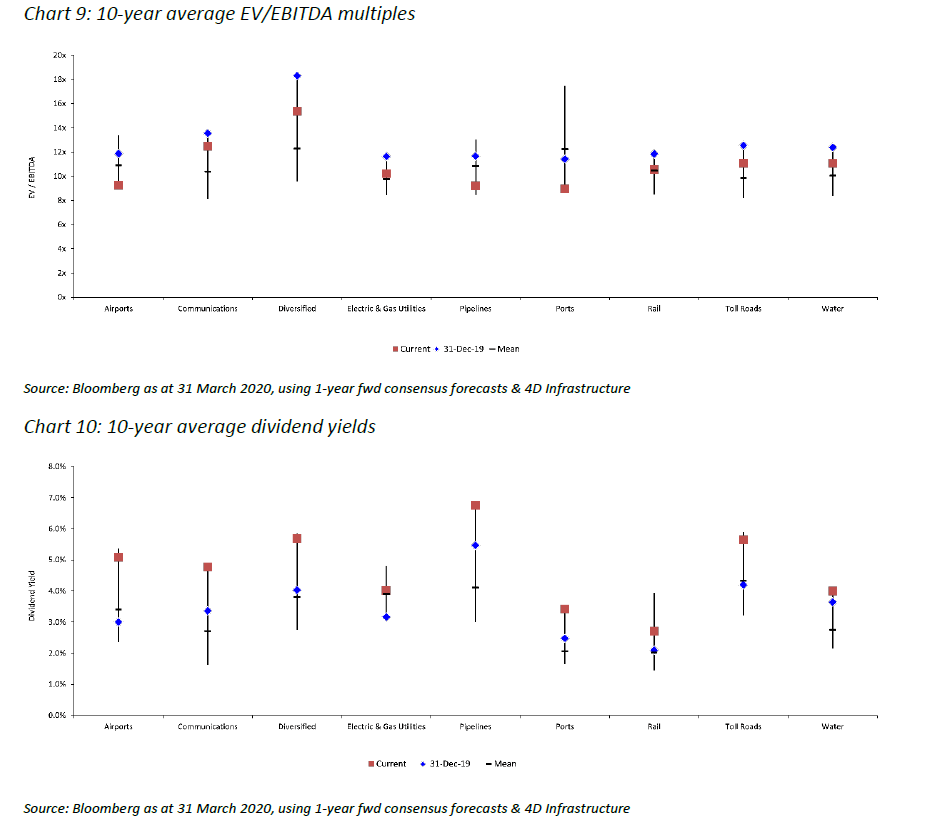

Attractive value across the sector

Shaw also highlighted the attractiveness of the infrastructure universe now by looking at 10-year EV/EBITDA multiples and average dividend yields (the blue dots show where these metrics were as at 31 December 2019 relative to now in the red dots).

“We believe this is a time to refrain from panic, and employ what Berkshire Hathaway’s Charlie Munger describes as ‘sit on your ass investing’, while taking advantage of any extraordinary opportunities the market might offer.”

While there are genuine concerns around companies' ability to ride out the storm, Shaw says solid, well-managed infrastructure businesses are not feeling a cash crunch at present, with reserves in place and balance sheets in strong starting positions (in many cases much stronger than prior to the GFC). Companies are communicating robust liquidity positions, including even the hard-hit airport sector, which should sustain them through COVID-19 into 2021 and beyond.

"Prudently, some companies are cutting dividends in order to further improve available cash, as well as appease social expectations from domestic governments. However, these are not what we would call forced cuts but rather a sensible reaction to a very uncertain environment."

The infrastructure universe opportunity set overall will also be underpinned by long-term population growth dynamics, low-interest rates (for the foreseeable future) and governments directing money toward infrastructure spending as part of fiscal stimulus packages aimed at combating the economic shock caused by COVID-19.

For more extensive views on the asset class from Sarah and 4D, access their recent paper 'Global matters: global listed infrastructure - 'buy' time looming?'

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

1 topic

2 stocks mentioned

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Based in Canada, Vishal has over 15 years' experience in financial journalism and has a particular interest in property, exchange-traded funds (ETFs), investing strategy and financial history.

Expertise

Comments

Comments

Sign In or Join Free to comment