Wage Worry

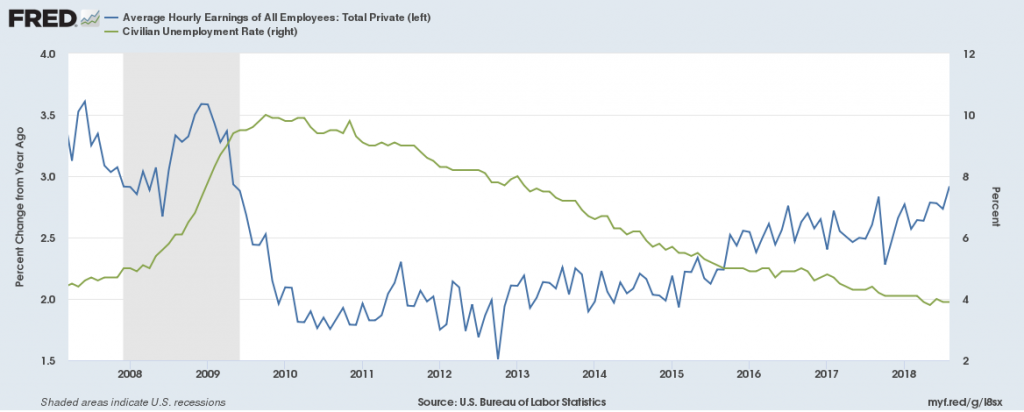

Global equities were on the defensive last week reflecting rising trade tensions and a higher than expected US wage outcome. Contrary to hopes, no US-Canada trade deal was announced and instead Trump ratcheted up the trade angst by threatening more tariffs on China and hinting his next focus could be Japan. Meanwhile, US payrolls on Friday revealed that annual growth in average hourly earnings hit 2.9%, contrary to a market expectation that it would remain steady at 2.7%. As seen in the chart below, annual growth in average earnings has displayed a volatile sawtooth pattern around a broadly steady trend in recent years, but it’s now again testing the top end of this range and a breakout (similar to that last evident in late 2015) could now be at hand.

As it happens, the market seemed to take the wage surprise reasonably well – with the S&P 500 only down 0.2% on Friday – possibly on the view that this could just be yet another rogue result which will be unwound in coming months. Given this backdrop, next months US payrolls report takes on even more critical importance. If annual wage growth breaks through 3% next month, the market could suffer some sticker shock, even though some further moderate gain in wages (as would be the case in Australia!) is in fact a healthy development. Indeed, it would still probably require wage growth to hit 3.5-4% before the Fed would see it as a sufficiently serious inflation problem warranting a more aggressive tightening schedule. As I’ve long argued, when and if that day eventually comes – and I still don’t think its around the corner – it would be game over for one of America’s greatest bull markets.

Closer to home, the S&P/ASX 200 suffered even more – despite a weaker $A and an upbeat Q2 GDP report – which would ordinarily both be market supportive. As outlined in my Market Trends report last week, one challenge for our market is that more of the rebound in recent months has been driven by valuations rather than earnings. At 16.1 times forward earnings, our market ended August at an above-average 8.2% premium to the global benchmark valuation. As regards Australian Q2 GDP, moreover, although the 0.9% quarterly gain was impressive, there are legitimate doubts as to whether such solid growth can be sustained given the diminishing pipeline of housing activity, low household saving, and a currently more subdued business investment outlook for this financial year.

Week Ahead

Trade tensions and the US CPI should be two of the major global focuses this week. While a possible US-Canada trade announcement could offer some solace to nervous investors, sadly the more serious tensions with China don’t appear likely to abate anytime soon. Given last week’s wage surprise, moreover, the market will likely be quite sensitive to any upside surprise in America’s consumer price index on Thursday.

In Australia, there will be interest in the extent to which recent global trade tensions and local political instability caused a further dip in the (still high) NAB survey measure of business sentiment when it’s released tomorrow. After a surprise decline last month, employment should bounce back solidly in Thursday’s labour market report. Having declined a little of late to 5.3%, there will also be interest in whether the unemployment rate manages to edge any closer to 5% – seen as a necessary first condition before we might expect a decent lift in wage growth and household income.

Have a Great Week!

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Author, columnist, investment strategist and macro-economist. Previous roles at Federal Treasury, OECD, Macquarie Bank and AFR. I develop economic insights and portfolio construction strategies for BetaShares' retail and adviser clients.

Comments

Comments

Sign In or Join Free to comment