Walking the risk vs. return tightrope

In deciding which risks are worth taking today in fixed income portfolios, it’s hard enough working out what to do with known, certain market influences, but even harder trying to factor in the many variables also at play. Conjuring a waterborne analogy, it feels much like an analogous swan navigating inclement weather on the Zambezi; graceful as always above the water, while constantly adjusting a frenzied and exhausting paddle beneath to stay afloat and on course.

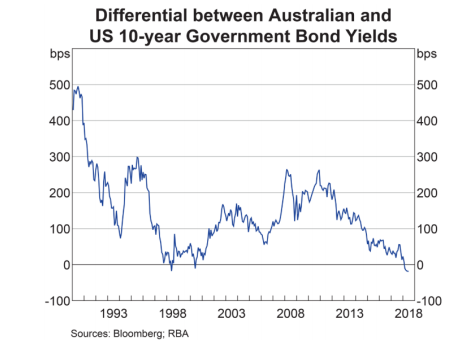

So what do we know with any degree of certainty? For the first time in 18 years US government bond and cash rates are higher than those in Australia (see below). Not just a little, but as much as 20% higher if you look at the 5yr part of the curve, with current* yields at 2.76% (US) vs 2.29% (AU). We know that company fundamentals are reasonably strong, corporates having worked hard to remedy their balance sheet weaknesses in the years since the GFC. Corporate spreads, while tight, still reflect a decent return for the risk you take lending to those of higher quality.

What of government bond curve shapes? In each region, precious little steepness, with a paltry 20bps^ extra reward for moving out as far as the US 30yr bond from the 5yr. Not quite the enticing term premia we’d like. But what does it tell us? Broadly, one of two things, a) that we will (must…?) see some steepening at the long end to return the curve to a more conventional shape, or b) that continued economic recovery remains more tenuous than markets are pricing in, and short end rates may be volatile, thereby adding to the appeal of a more stable – albeit lacklustre – long bond yield. The continued weight of money from defined benefit pension money hoovering up long end supply also remains a headwind to steepening.

And hikes generally? From a more consensual position of several Fed rate hikes still to come, Kapstream flits between ‘one’ and ‘done’ when we consider the remainder of 2018. ‘One’ assumes US unemployment remains at historic lows and trade warring and geopolitical risks don’t worsen (which they arguably already have); ‘done’ is starting to feel progressively more likely, not least of all as the bizarre Trump circus continues to surprise/perplex/astonish/shock (all interchangeable depending on the day of the week and which policy has his attention).

The question is, ‘what to do?’. If we have conviction that rates stay put in the near term, then lengthening portfolio duration beyond current (relatively modest) levels makes some sense. For some time, our view on the RBA holding rates at current levels hasn’t altered, so maintaining duration exposure to AU rates at a little above ½ a year feels comfortable. Not least of all for the slight return tailwind it may potentially provide, but also for its protection against the credit (spread) duration exposure elsewhere in the portfolio. But do we dare add some US rates exposure to the mix? While absolute yields remain low, the very real risk of failing on our objective of delivering consistently positive monthly returns will quickly materialize if we prove to be too bearish and the Fed continues on a more bullish hiking path.

There is also the very real challenge of continued sloooooow widening of spreads as credit markets balance reasonably robust corporate fundamentals against the gradual withdrawal of Quantitative Easing programs and resultant volatility. Across Kapstream’s portfolios spreads have widened 10+ bps on average so far in 2018. With credit spread duration of ~3 years that equates to a rough mathematic detraction of 30bps; a ‘paper cut’ that persists with a slow bleed. However, the one silver lining of this cloud that remains over us is that coupons/interest from the very same portfolio are now some 30bps higher today than six months ago, which means higher future returns from a portfolio with no greater default risk than then. Patience is a virtue.

So, this undoubtedly remains an environment in which those managers able to ‘walk the tightrope’ between protectionist and opportunist earn their fee. Risk management first, return generation second. Keep your head above the surface and your powder dry for calmer waters ahead, but in this unchartered territory it pays to be prepared for what’s around the next bend.

For more insights from Kapstream Capital, visit our website: (VIEW LINK)

* Source: Bloomberg, 22/7/18

^ Source: US Department Of The Treasury, 12/7/18

Unless otherwise specified, any information contained in this publication is current as at the date of this report and is provided by Fidante Partners Limited (ABN 94 002 835 592, AFSL 234668) the issuer of the Kapstream Absolute Return Income Fund (ARSN 124 152 790) (Fund). Kapstream Capital Pty Limited (ABN 19 122 076 117, AFSL 308870) is the investment manager of the Fund. It should be regarded as general information only rather than advice. It has been prepared without taking account of any person’s objectives, financial situation or needs. Because of that, each person should, before acting on any such information, consider its appropriateness, having regard to their objectives, financial situation and needs. Each person should obtain the relevant Product Disclosure Statement (PDS) relating to the Fund and consider that PDS before making any decision about the Fund. A copy of the PDS can be obtained from your financial adviser, our Investor Services team on 13 51 53, or on our website (VIEW LINK). If you acquire or hold the product, we and/or a Fidante Partners related company will receive fees and other benefits which are generally disclosed in the PDS or other disclosure document for the product. Neither Fidante Partners nor a Fidante Partners related company and our respective employees receive any specific remuneration for any advice provided to you. However, financial advisers (including some Fidante Partners related companies) may receive fees or commissions if they provide advice to you or arrange for you to invest in the Fund. Kapstream Capital, some or all Fidante Partners related companies and directors of those companies may benefit from fees, commissions and other benefits received by another group company.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Founded in 2006, Kapstream offers investors an alternative approach to fixed income, combining capital preservation techniques with unconstrained portfolio management skills in the pursuit of stable, absolute returns.

Kapstream

Founded in 2006, Kapstream offers investors an alternative approach to fixed income, combining capital preservation techniques with unconstrained portfolio management skills in the pursuit of stable, absolute returns.

Expertise

Kapstream

Founded in 2006, Kapstream offers investors an alternative approach to fixed income, combining capital preservation techniques with unconstrained portfolio management skills in the pursuit of stable, absolute returns.

Expertise

Comments

Comments

Sign In or Join Free to comment