What history can tell us about a potential value rally

After the extraordinary rally in growth stocks over the last few months, the question we frequently hear from investors is whether the market will enter a value rally – perhaps not right now, but over the near to medium term.

The more predictable the earnings growth, the more likely a value rally

We do not have strong views about the potential external triggers of such a value rally, be it government intervention, central bank policy, inflation or political change. However, we believe that earnings – or more precisely, cash flows – are ultimately the drivers of a value rally, in particular the predictability of earnings growth. The more predictable the earnings growth for the market as a whole, the more likely we experience a value rally.

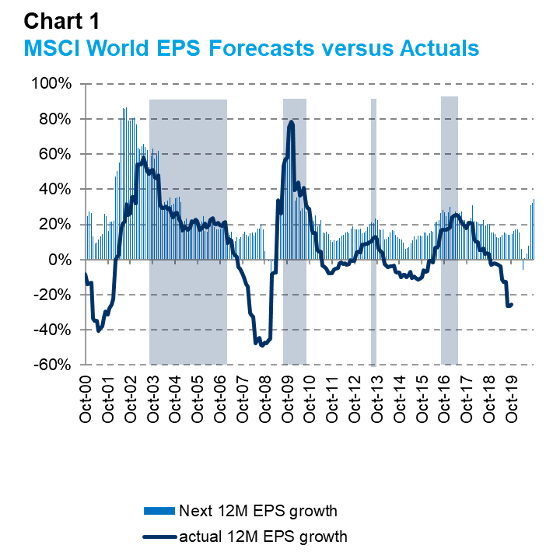

Chart 1 illustrates this point. The bars show consensus expectations in terms of 12 months forward EPS growth. The dark blue line shows actual EPS growth. Where the bars and the dark blue line are closely aligned, the consensus was broadly right, and where they diverge, earnings have been unpredictable and disappointed expectations. The shaded vertical areas show periods of value rallies, i.e. periods where the MSCI World Value Index outperformed the MSCI World Growth Index. As you can see, value rallies have historically occurred when earnings forecasts were reliable.

Source: MSIM and FactSet, October 2020

This should not be much of a surprise. A value stock is one that is cheap relative to its near-term intrinsic value. The intrinsic value of a company is a function of its future free cash flows, of which earnings are an important component and hence its ability to pay dividends or reinvest in the business. During periods of predictable earnings, value stocks can be attractive as they often trade at a discount to intrinsic value due to uncertainty caused by e.g. cyclicality, management or perceived structural issues. In such instances, the gap between price and intrinsic value can be determined fairly easily. When earnings keep disappointing, determining the intrinsic value can become difficult for investors and the discount for uncertainty deepens.

If we look at the value rally from 2003 to July 2007, the stable “Goldilocks” environment made earnings growth predictable and value stocks outperformed. Similarly, during the 2009/10 recovery period, earnings forecasts for cyclical value stocks were reliable and so investors bought into them.

A value rally is first and foremost an earnings phenomenon, not a valuation phenomenon

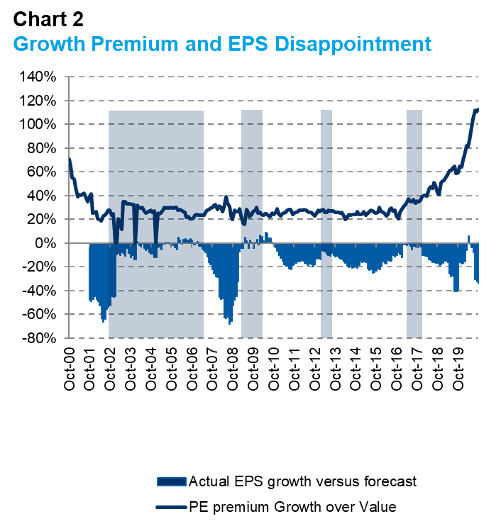

Since 2010 we have gone through nearly 10 years of near-consistent earnings disappointments, driven not only by negative rates but also technological disruption and political upheaval - first in the Eurozone and then in the U.S./China relationship. Apart from the very brief periods of 2012/13 and 2016 when temporary relief measures created earnings growth that matched up to forecasts, earnings have disappointed and value stocks underperformed.

What matters very little is the relative valuation of value stocks versus growth stocks. The premium in Price Earnings terms between growth stocks and value stocks was fairly stable before and going into the four main value rallies of the last 20 years. In other words, a value rally is first and foremost an earnings phenomenon, not a valuation phenomenon.

Source: MSIM and FactSet, October 2020

The picture emerging in 2020

During the current COVID crisis we have seen by far the largest underperformance of value versus growth of the last 20 years, even though near-term earnings disappointment is no worse than in 2018, for example. This has left us with the biggest relative valuation gap between value and growth since 2000.

Without earnings growth becoming more predictable, there will be no value rally

The gap suggests that the market believes that there is more earnings disappointment ahead, i.e. the consensus 35% earnings improvement for the next 12 months will simply not materialise. We do not know whether the market is right, but we are fairly confident that without earnings growth becoming more predictable, there will not be a value rally. And as we have seen in the last 10 years, predictability of earnings is not just a function of economic growth, but also a question of how well companies handle disruption, embrace new technology and – increasingly – how well they deliver on ESG matters. In other words, quite a lot of things need to go right for a value rally to happen.

Quality in a value rally

This brings us to the next question: how does a quality portfolio behave in a value rally? A quality stock as we define it has first and foremost predictable earnings growth at sustainably high returns. In a period when very few companies have predictable earnings, quality stocks tend to outperform. This is mostly on the back of stronger earnings, but also in part due to a higher scarcity premium. In a value rally, this scarcity premium goes down. However, predictable earnings growth should not be affected. Therefore, the absolute risk to a quality portfolio lies in valuation, not in earnings. If we look at historical trends and the relative performance of our global strategies, we see that in periods of value rallies (2003-2007, 2009/10, 2012/13 and 2016), generally performance lagged in relative terms but was strong in absolute terms. More recently, we have again seen our global portfolios’ earnings profile showing predictability and resilience even in this unprecedented environment.

Our global portfolios’ earnings profiles have shown predictability and resilience, even in this unprecedented environment

Our main concern now is valuation. In the pandemic, companies with predictable earnings profiles have become even scarcer and their valuation premium has gone up. That is particularly true for high growth technology companies and the so-called “COVID-winners”.

We believe that there are two ways to lose money: either the earnings go away or the multiple goes away. This makes us wary of high growth/high valuation companies. As a result, the portfolio changes we have undertaken in the last few years have mostly been driven by concerns about valuation rather than earnings growth. We have steadily shifted out of stocks with excessively high valuation into stocks with more realistic valuations. As a consequence of both stronger earnings and our approach to valuation, our global portfolios have actually de-rated versus the market. In contrast, most growth portfolios have re-rated during the pandemic.

Going forward, we have no visibility on valuations, neither absolute nor relative. Whether the portfolio outperforms in the near and medium-term will partly depend on whether or not the market shifts into a world of higher overall earnings predictability. But relative performance is not our objective. We aim to buy stocks with earnings which compound predictably and sustainably high returns on operating capital, at acceptable prices. Our goal is to generate absolute, rather than relative returns over the long term.

Invest in quality

Morgan Stanley Investment Management are a global franchise delivering innovative investment solutions across public and private markets worldwide. Click the 'FOLLOW' button below for more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bruno is a portfolio manager for Morgan Stanley Investment Management’s London-based International Equity team. Prior to that, Bruno worked for Sanford Bernstein, where he was a Senior Analyst covering the financial sector for eight years.

Bruno is a portfolio manager for Morgan Stanley Investment Management’s London-based International Equity team. Prior to that, Bruno worked for Sanford Bernstein, where he was a Senior Analyst covering the financial sector for eight years.

Expertise

Bruno is a portfolio manager for Morgan Stanley Investment Management’s London-based International Equity team. Prior to that, Bruno worked for Sanford Bernstein, where he was a Senior Analyst covering the financial sector for eight years.

Expertise

Comments

Comments

Sign In or Join Free to comment