What is our favorite commodity after the latest gold crunch?

We've been talking about MM’s reflation outlook a lot recently i.e. we anticipate inflation will finally rear its head courtesy of the unprecedented degree of financial stimulus by both global central banks and governments. The entrenched downtrend in the CRB Index illustrated below shows this is clearly a call for a change in trend – the CRB Index is made up of all commodities from precious metals to the energy complex and foodstuffs like soybeans, sugar and corn. Gold might exert the most influence, but it hasn’t been able to offset the numerous bear markets still unfolding in the other markets.

Obviously we are far more interested in the individual commodities when evaluating stocks / sectors but it’s reassuring that a 30-50% rally would hardly dent the decade old downtrend – perhaps I’m wearing rose coloured glasses and the downtrend should be scarring me!

MM remains bullish the “reflation trade”.

Bloomberg CRB Index Chart

1 Precious Metals.

The influence of bond yields on financial markets has been extremely evident over the last few days with gold plunging over $US200/oz, or more than 10% in less than 4-days – we certainly live in interesting times! By 9pm last night the precious metal complex had reversed early losses in a huge way with silver bouncing 10% in just a few hours! However we should ask the question what did the bulls expect, gold had risen for 9 consecutive weeks, its longest winning streak since May, 2006, just this financial year alone the precious metal had risen over 15%.

The irrational exuberance in the precious metal complex has shown the way ahead for us but things needed reining in and they clearly have been, the excited bulls were already inking in the all-time “real” price high set in 1980 of $US2,800/oz. The press was full of gold as were investors portfolio’s, especially the fickle momentum traders hence the perfect recipe for the washout we’ve been calling which has subsequently unfolded. However we believe golds journey is far from over, the latest bullish move was inspired by negative real interest rates only began in late March 2020, just 5-months ago, remember MM believes the gold price could rally for a few years and pullbacks are to be bought.

MM took advantage (hopefully) of this aggressive washout to buy Newcrest Mining (NCM) for our Growth Portfolio and the ETF Securities Silver Bullion ETF (ETPMAG) for our Global Macro ETF Portfolio.

We remain bullish precious metals in the coming months.

Gold $US/oz Chart

Silver $US/oz Chart

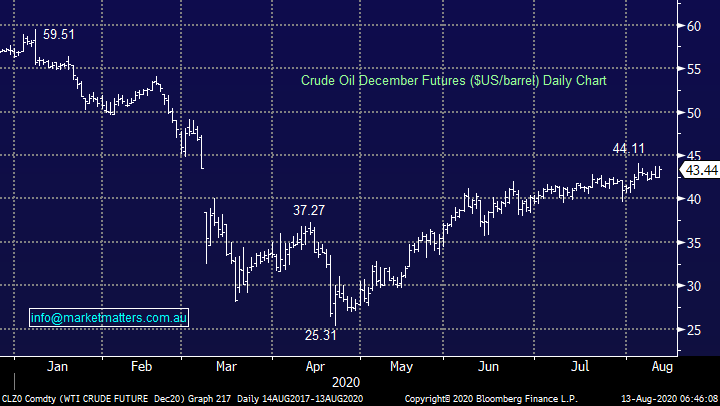

2 Energy Stocks

The oil price continues to trade around multi-month highs yet the stocks are well below their equivalent milestone scaled in June, our conclusion is simple – MM believes that the energy sector is materially undervalued and presents excellent risk / reward from current levels. Inventories are already being drawn down due to increasing demand and reduced production, a healthy combination. Also as mentioned earlier in the week we believe Natural Gas has reached a point of inflection leaving only coal to trigger some optimism in the energy complex.

MM remains bullish the Energy Sector.

Crude Oil December Futures ($US/barrel) Chart

Our preferred exposure is Beach Petroleum (BPT) due to its deep valuation on offer and strong balance sheet i.e. it can fund growth and maintain operations with crude oil at current levels. We also own Woodside (WPL) in our Growth Portfolio, it’s the most conservative option but enjoys the best balance sheet. Hence MM is considering increasing our BPT position.

MM remains bullish BPT medium-term.

Beach Petroleum (BPT) Chart

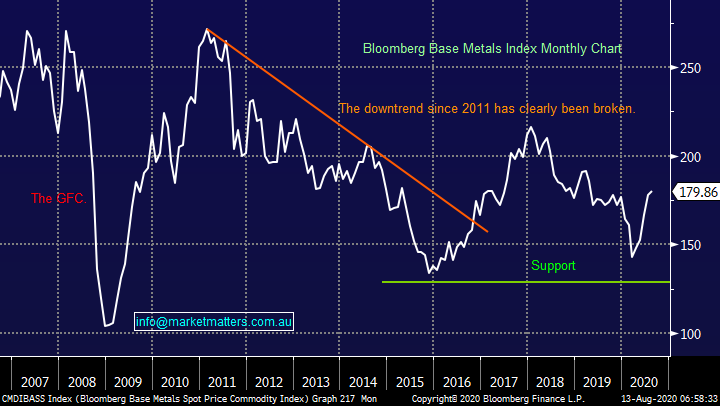

3 Industrial / Base Metals.

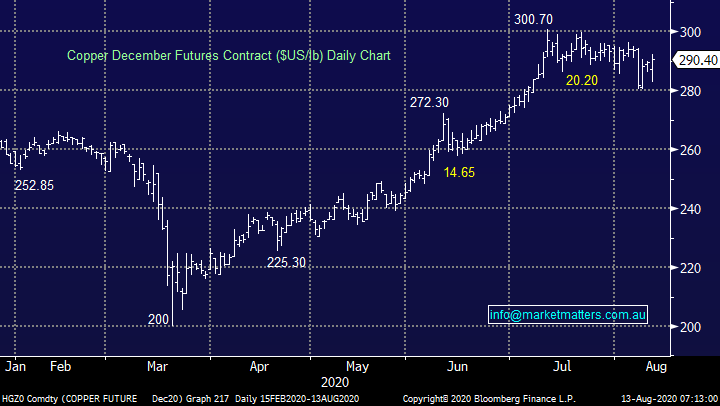

The 50% rally by copper has helped the base metals recover a significant portion of their last few years decline but we believe there’s a lot more left on the upside especially when / if the likes of nickel and aluminium join the party. Dr copper managed to rally over 5% in July but it did fall over 4% last Friday, some further consolidation wouldn’t surprise over the coming weeks.

While we see no reason to exit our copper play via OZ Minerals (OZL) the question we ask is should we be more evenly spread across the metals complex – we also hold Western Areas (nickel) and Alumina (aluminium) plus of course goliath diversified miners BHP Group (BHP) and RIO Tinto (RIO). The simple answer is not at this stage, any further tweaking looks & feels unnecessary, our position reflects our view, it’s time to sit back and see if we are correct.

MM remains bullish industrial metals.

Bloomberg Base Metals Index Chart

Coppers been consolidating for around a month now with Fridays ~4% drop not really registering on the chart, we are actually bullish short-term liking copper for a break above $US300/lb in the coming weeks.

MM sees an additional 5% upside in copper short-term.

Copper ($US/lb) Chart

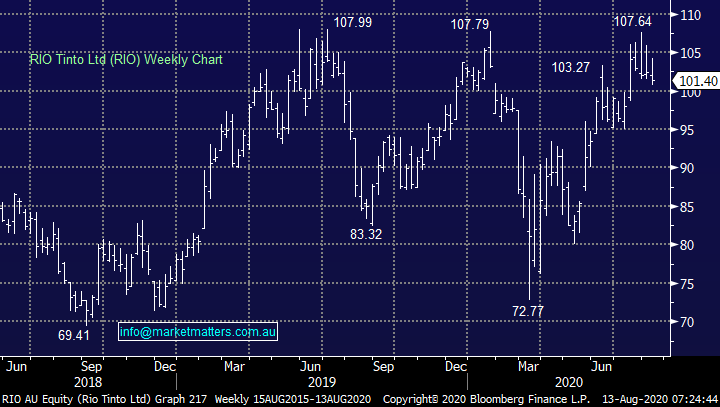

4 Iron Ore.

Bulk commodity Iron Ore has been a standout in 2020 rallying over 60% from its April low. Not surprising the related stocks have enjoyed a great year with pure play Fortescue (FMG) the standout up 130% since March while the more diversified RIO Tinto (RIO) has gained just under 50% and BHP Group (BHP) almost 70%. At this stage we feel these are the stocks which have potentially got ahead of themselves on the optimism front and while we remain bullish they are vulnerable to underperformance at least short-term.

Iron Ore(CNY/MT) Chart

RIO Tinto (RIO) Chart

Conclusion

MM likes our portfolio mix across the commodities front but we are considering trimming (not closing) either our BHP or RIO position and increasing our BPT holding, a slight move up the risk curve with regard to commodities.

Register for a free trial to Market Matters

At Market Matters, we write a straight-talking, concise, twice daily note about our experiences, the stocks we like, the stocks we don’t, the themes that you should be across and the risks as we see them.

To sign up for a free trial to Market Matters, leave your email and phone number through the 'CONTACT' button below

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and Partners heading up a team that manages direct domestic and international equity & fixed-income portfolios for wholesale investors.

........

Any advice provided is of a general nature only.

2 stocks mentioned

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

James is the Lead Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & portfolios open for investment. He is also a Senior Portfolio Manager at Shaw and...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

The most consistent ASX dividend stocks

Livewire Markets

Equities

Buy Hold Sell: 5 ASX names built for income

Livewire Markets