What Mattered Today; Trump loses economic guru – stocks drop 1%

Yesterday afternoon we wrote…What Trump Slump? Markets regain their mojo – however the red across the tape today clearly shows that said mojo has come and gone pretty quickly. All was looking reasonable for a good day today, futures were slightly higher, a major broker has upgraded CBA and a weaker $US had prompted some buying in the material stocks overnight, however the resignation of Gary Cohn, Trumps Economic Adviser sent US Futures sharply lower and we followed suit. That suggests the market's knee-jerk interpretation of Gary Cohn's resignation is that neither he, nor anyone else, was able to convince Trump that unfocused tariffs on steel and aluminium imports are a bad idea. The follow-up headline saying the U.S. is considering broad curbs on Chinese imports and takeovers will add to concerns the apparent easing of trade tensions on Tuesday was a mirage.

From an investment standpoint, there is now the obvious struggle in determining whether or not Trump is more interested in U.S. stocks escaping their recent volatility and returning to record highs, or levelling what Trump has long considered an uneven playing field for global trade. Cohn's resignation suggests the president's priorities may have shifted decisively from the former to the latter.

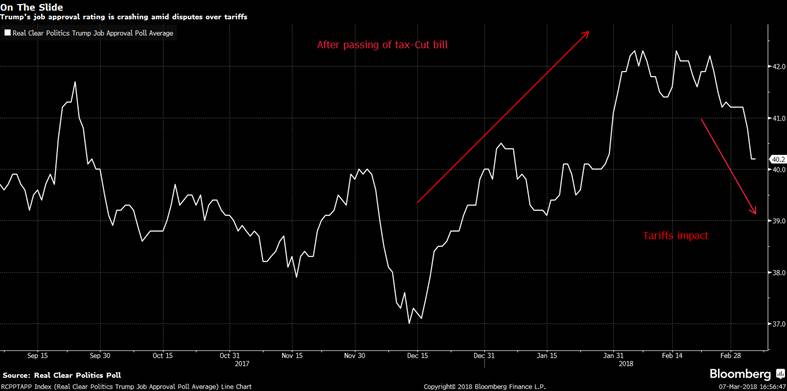

Interesting to see Trumps approval ratings are now on the slide – he’d hate that I would have thought!!!

That interpretation of Cohn’s resignation will get tested tonight in the states with US Futures trading down -1.25% at time of writing pricing a negative start at least, while Asian markets were also weaker today, but not by as much. Our market was sold off early, bounced up around midday then tracked lower into the close. It seemed no one wanted to go home long today!

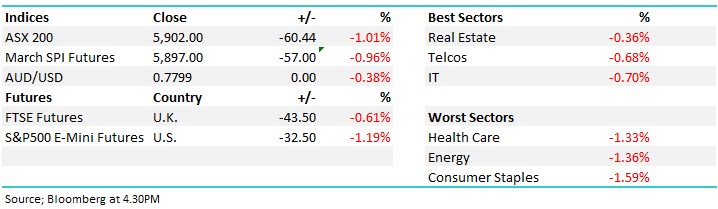

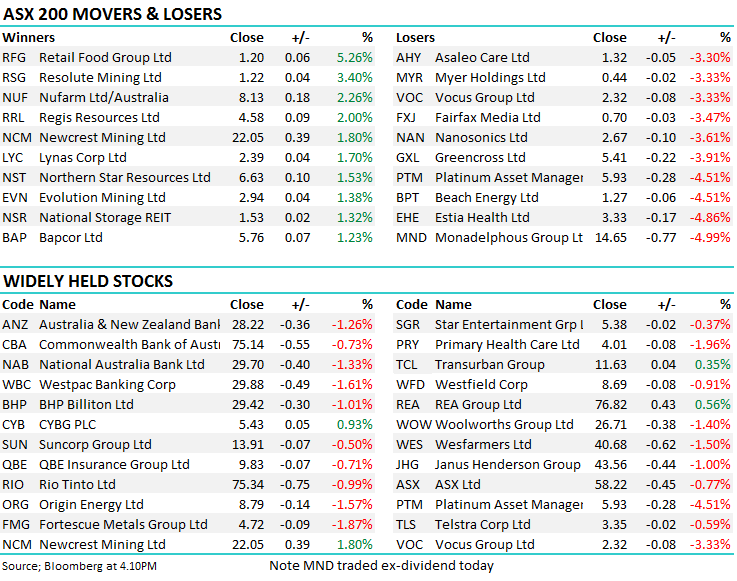

Overall, the S&P/ASX 200 Index finished -60 points lower giving back most of yesterday’s gains – this index now at 5902 points - a drop of -1.01% - red right across the sector landscape today!

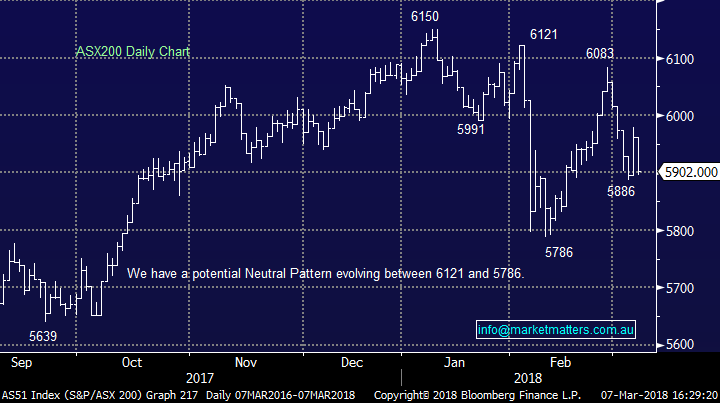

ASX 200 Chart

ASX 200 Chart

CATHCING OUR EYE

1. Aussie GDP; Was out today and missed expectations for Q4 however there was some upward revisions on prior numbers which helped to offset the miss. The main issue was around non-dwelling construction , so the building of stuff that you don’t live in which took 0.5% off the GDP number. All in all, Real GDP rose 0.4pc over the quarter, but stepped down 2.4pc over the year, well below the long-term average of closer to 2.9pc. A rise in consumer spending helped offset a drag of net exports and slowing construction.

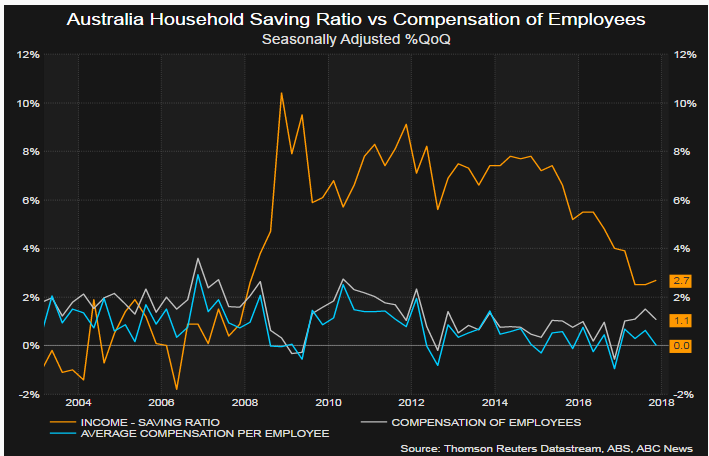

Total wage growth over the quarter rose 1.1pc, reflecting strong jobs growth, while average earnings flat lined.

This is a good chart highlighting household savings (orange line) versus movement in wages

2. Commonwealth Bank (CBA) $75.14 / -0.73%; Was weaker today however outperformed the banks after Bank of America raised it to a buy. He reckons that the ~7% underperformance to peers NAB and ANZ since June last year is too much and concerns around a potential money laundering case are now reflected in the price. They now have the most bullish call on the street with a PT of $87.50. In terms of the wider sector, they share our view saying that the Australian banking sector is closer to oversold than overbought!! That sounds a bit ‘grey’ but that’s about as high conviction in terms of language you’re ever likely to get.

Commonwealth Bank (CBA) Chart

Have a great night

James & the Market Matters Team

The above is an extract from the Market Matters Weekend Report. For a free 14 day trial of our service CLICK HERE

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

1 stock mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment