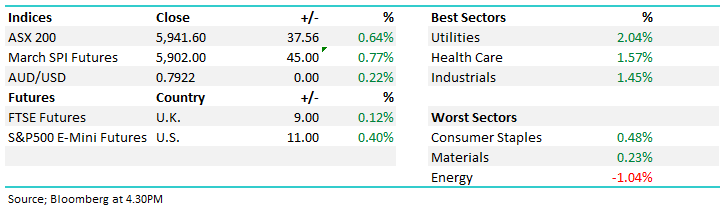

What Mattered Today; Woodside gets whacked...

Reporting dominated the market today with some reasonably big ranges for those companies out with results. Overall the market was weak on open, largely a result of selling amongst the resource plays while the banks bucked their recent trend and provided good support – the mkt rallying well from the 10.30am low this morning, closing near its highs – up 37pts or +0.64% to close at 5941. The typical defensive style sectors did best, Utilities & Healthcare while the energy stocks were hit after Woodside came back online post their massive $2.5bn capital raise – the stock declined by 6.81% to close at $28.63 – a poor result – more on that later.

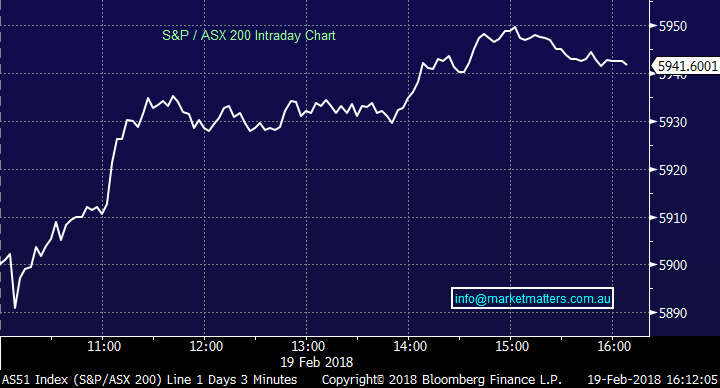

ASX 200 Intra-Day Chart

ASX 200 Daily Chart

CATCHING OUR EYE

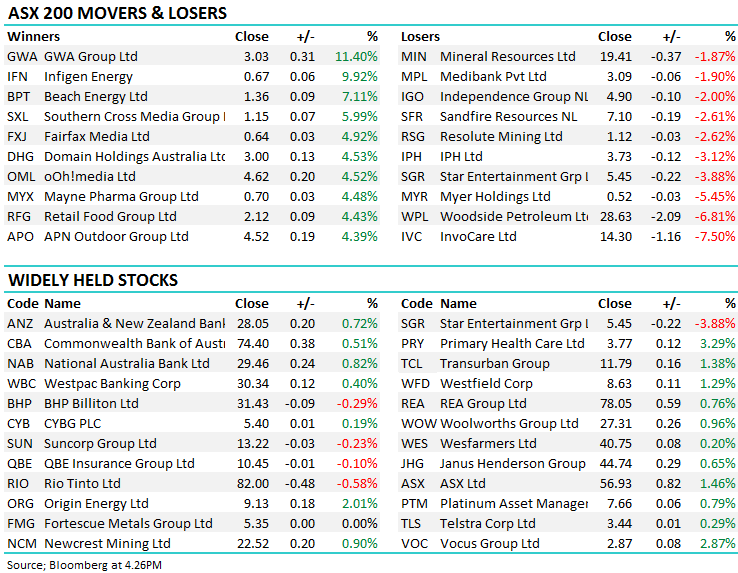

1.Woodisde Petroleum (WPL) $28.63 /-6.85%; 90% of institutional shareholders took up their entitlement under the current offer at $27 a share on a 1 for 9 basis, leaving a shortfall which was auctioned off - with a settlement price of $29.60, a premium of A$2.60 to the offer price of A$27.00 per share, and a discount of 1.7% to the theoretical dividend adjusted ex-rights price ("TERP") of A$30.11 per share. I would have thought the shares would do better today however there was obvious selling to fund new stock being issued at $27.00.

As a retail shareholder, a few key aspects to consider; The renounceable rights have commenced trading today under code WPLR. A holder can elect to take them up, sell them on market before the 28th Feb, or if no action taken, they go into a book and the proceeds flow back to holders. The settlement of the Retail Entitlement Offer is the 15 March 2018.

Woodside Daily Chart

2.Seek (SEK) $20.50 /1.94%; Reported a 1H result that was in line with expectations however they increased guidance which the market liked. All metrics were strong for SEK with revenue growth of +26%, EBITDA growth +20% - NPAT at 103m which was inline. In terms of guidance, they reaffirmed revenue growth of 20-25% but importantly, they expect EBITDA growth of 14-15% which is an upgrade from 12%. All up a good result, the only slight issue was around higher than expected cost growth.

Seek Daily Chart

3. InvoCare $14.30 / -7.5%; the funeral provider was hit hard today after reporting decent full year numbers (in line with expectations) however they downgraded guidance to “low single digit 2018 operating EBITDA,” mostly subdued due to some sites being refurbished during the year - obviously a disappointing growth outlook as the market was looking for a ~8% through 2018.

IVC has done a good job of increasing margins but it seems to have come at the expense of market share which fell over 2017. As grim as it sounds, IVC is in a market we like, as the population ages there will be natural growth in the business model. The push for IVC to pre-sell funerals also holds risk as inflation between sale and delivery (of the body) will impact margins. However, now over 20% below it’s all time high set in November last year, IVC is beginning to look interesting here.

Invocare Daily Chart

4.Brambles (BXB) $9.74 / 1.14%; The market took the result poorly in the first instance, however the company did a good job of talking things up on the conference call – and the stock rallied from the lows. Revenue was $2.75bn with the market expecting $2.8bn, in constant currency terms, growth was c5% which was inline - importantly, the Nth American CHEP business returned to volume growth (around +2%) and the emerging mkts division was good . Anyway, we’re not a big fan of BXB at current levels – not a lot to get excited about but a reasonable result non-the-less.

Brambles Daily Chart

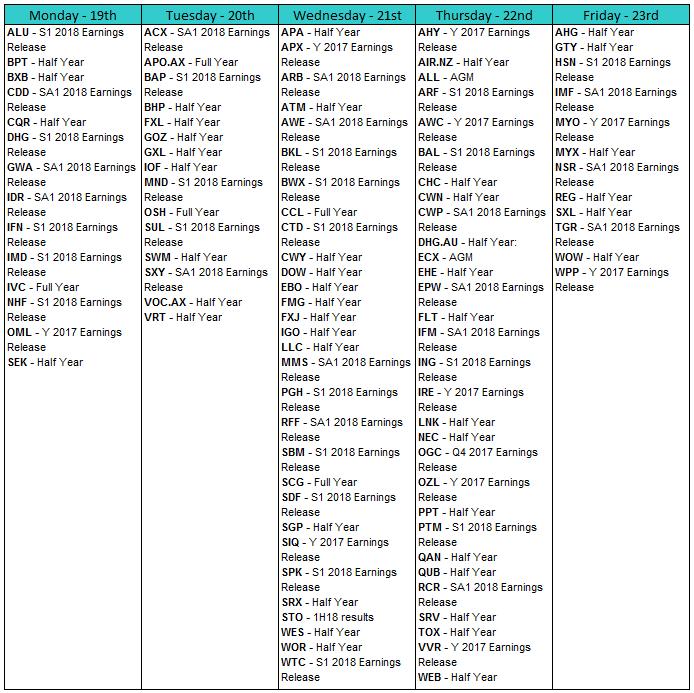

REPORTING THIS WEEK

A big week in terms of reporting – stocks in our portfolio include; FMG, BHP, AWC, OZL, PPT, WEB all out with results. I’m also pretty keen to see IGO, LLC, PPT, and Woolies.

Last week, we had a slight skew of beats to misses in terms of earnings, 8 to 6 in the larger cap space, while more of them beat v missed in terms of the dividend. Aggregate growth expectations for FY18 have fallen from 8.4% to 6.8%, largely driven by CBA which missed given AUSTRAC provisioning. All up, reporting is doing OK with a few decent results out today to kick off this parade…

Have a great night

James & the Market Matters Team

The above is an extract from the Market Matters Afternoon Report. To gain access to all reports for the next 14 days, including our picks into the market drop, CLICK HERE

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors.

James is also Portfolio Manager & primary author at Market Matters, a digital advice & investment platform with over 2500 members that offers real market intel & six portfolios open for investment.

4 stocks mentioned

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

James is Director & Lead Portfolio Manager at Market Partners - a collective of highly experienced investment professionals, operating independently, managing discretionary portfolios for wholesale investors. James is also Portfolio Manager &...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets

Funds

The 5 best-performing super funds of the year

Livewire Markets