What possibly keeps the FED awake at night.

.jpg)

James Smith

Providence Independent Investment Advisory

For the members who preside over the US Federal Reserve (the FED - the central bank for the United States), one might ask what keeps them awake at night. While the easy answer is ‘quite a lot’, for the purpose of this article, let’s look at the primary driver of the FED’s dual mandate: to "promote effectively the goals of maximum employment, stable prices, and moderate long-term interest rates".

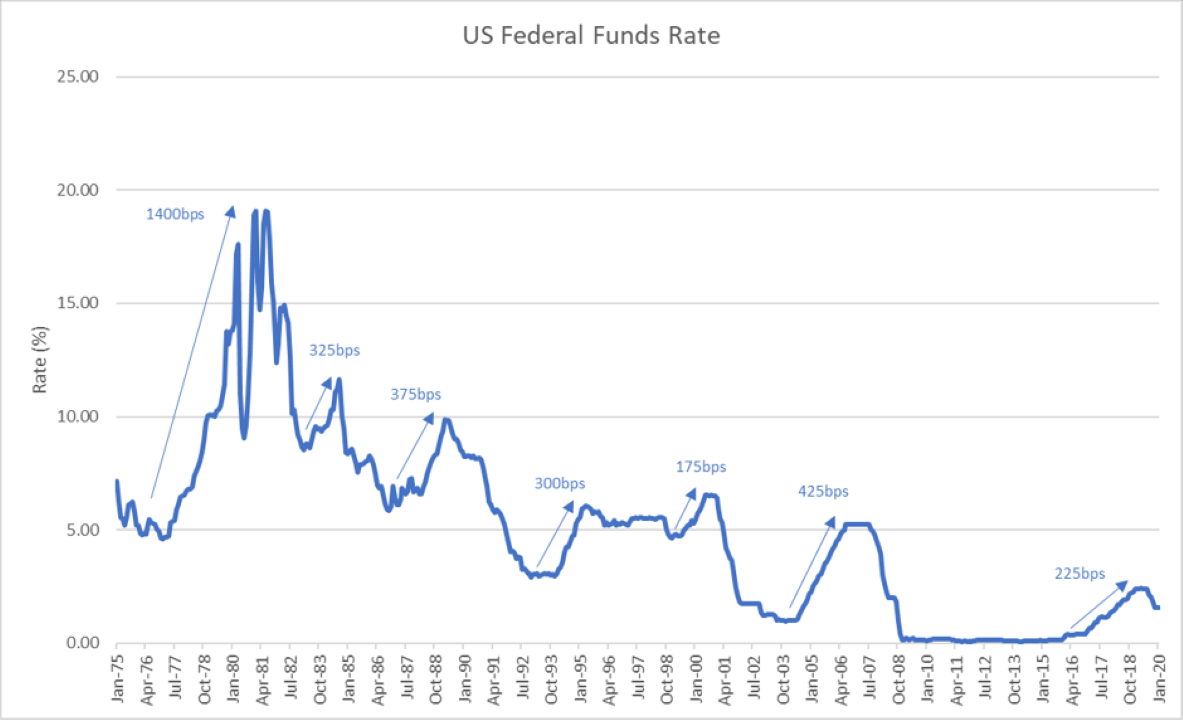

The influence that the direction of the FED’s interest rate policy path has on financial markets, its bearing on global investment markets, currencies and other economies is significant. Therefore, it is interesting to look at the history of US interest rates over more recent cycles.

If the Fed’s starting point for cutting official interest rates is declining, they have less in the tank to play with. Early in 2019, a number of market observers believed the FED had finished raising rates for this cycle, arguably buoyed by the FEDs own remarks in December 2018 that they “promised” to stop raising rates. As 2019 progressed and data remained unresponsive (mostly in the form of a lack of inflation) and global growth slowed, the FED cut rates three times, starting in August. The cycle ‘peak’ for now, reset lower once again at 2.5%.

If this is the new revised down “peak” (1.5% as 2.5% didn’t last long), the US FED official interest rate is once more set lower than previous rate tightening cycles. Substantially lower. The question as to whether the FED is ‘done’ with raising rates this cycle is an interesting one given there remains robust momentum in the US economy (albeit an economy that is late cycle). If the FED has completed rate hikes for this cycle, their monetary firepower (in the form of rate cut scope) is 375bps below the last rate hike cycle peak (2006) and 500bps below the peak prior to that (Jan 2000) (Figure 1).

In any cycle, there are two primary forms of stimulatory levers that can be pulled to help an ailing economy: Interest rate reductions and fiscal stimulus in the form of increased government spending. Often these go hand in hand to get an economy active after a significant slowdown or recession. More recently, history has shown that the FED also has another lever - Quantitative Easing. While unprecedented in its actions, the combination of dramatic interest rate cuts, and Quantitative Easing pulled the US economy out of recession and helped steer the world away from the Global Financial Crisis (GFC) triggering a massive asset reflation event over the last decade.

The FED suggests (through a dot-point guidance for official interest rates) that their ‘neutral’ or long-run average rate is now 2.5% or 100bps above the current level. That is still 275bps below the previous cycle peak.

As debt continues to rise for both public and private enterprise, the burden compresses the ability for official interest rates to rise to levels seen in previous rate hike cycles. In the absence of a massive burst of inflation (still up for debate), it appears that official interest rates in the US will again peak at a lower rate compared to previous cycles.

This, therefore, leaves the US FED with less monetary firepower in the next economic downturn to stimulate the economy. The US government, already heavily indebted, would no doubt ‘double down’ with more debt to help stimulate a flightless FED. An ailing economy may be less responsive to a smaller quantum of interest rate cuts given the above scenarios when the time comes.

And the cycle lives on… with more debt and lower rates and arguably lower returns.

Figure 1. Rates & Bonds: History of Fed Policy and Hiking Cycle

Source: Bloomberg

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

With 25 years of investment market experience, James holds the position of Senior Investment Adviser for Providence Independent Investment Advisory, founded in 2000 and is responsible for Melbourne clients of the firm.

.jpg)

James Smith

Head of Melbourne, Senior Investment Adviser

Providence Independent Investment Advisory

With 25 years of investment market experience, James holds the position of Senior Investment Adviser for Providence Independent Investment Advisory, founded in 2000 and is responsible for Melbourne clients of the firm.

Expertise

James Smith

Head of Melbourne, Senior Investment Adviser

Providence Independent Investment Advisory

With 25 years of investment market experience, James holds the position of Senior Investment Adviser for Providence Independent Investment Advisory, founded in 2000 and is responsible for Melbourne clients of the firm.

Expertise

Comments

Comments

Sign In or Join Free to comment