What’s going on in Listed Property?

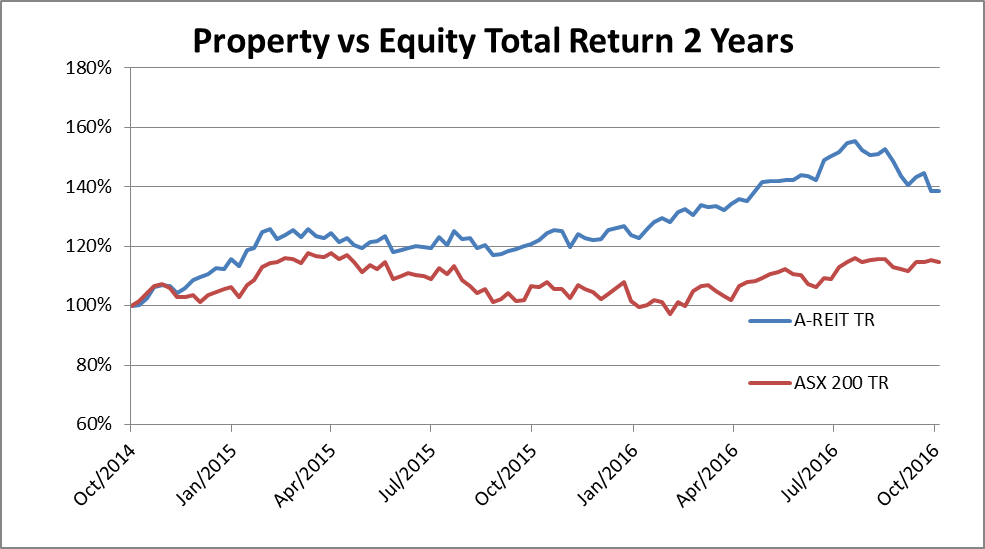

Over the last two years listed property has been the top performing sectors on the ASX 200 outperforming the broader equity market. While Australian other sectors in the equity market have faced concerns about a rising and then falling AUD, falling commodity prices, Eurozone issues and bank capital raisings, listed property has seemingly sailed under the radar up until mid-July 2016 and has since fallen 12% over the past quarter. In this note, we will look at what has caused this fall, what is going on in listed property together with our positioning in the Aurora Property Buy-Write Income Trust (AUP) in the various property sectors.

What’s driving performance?

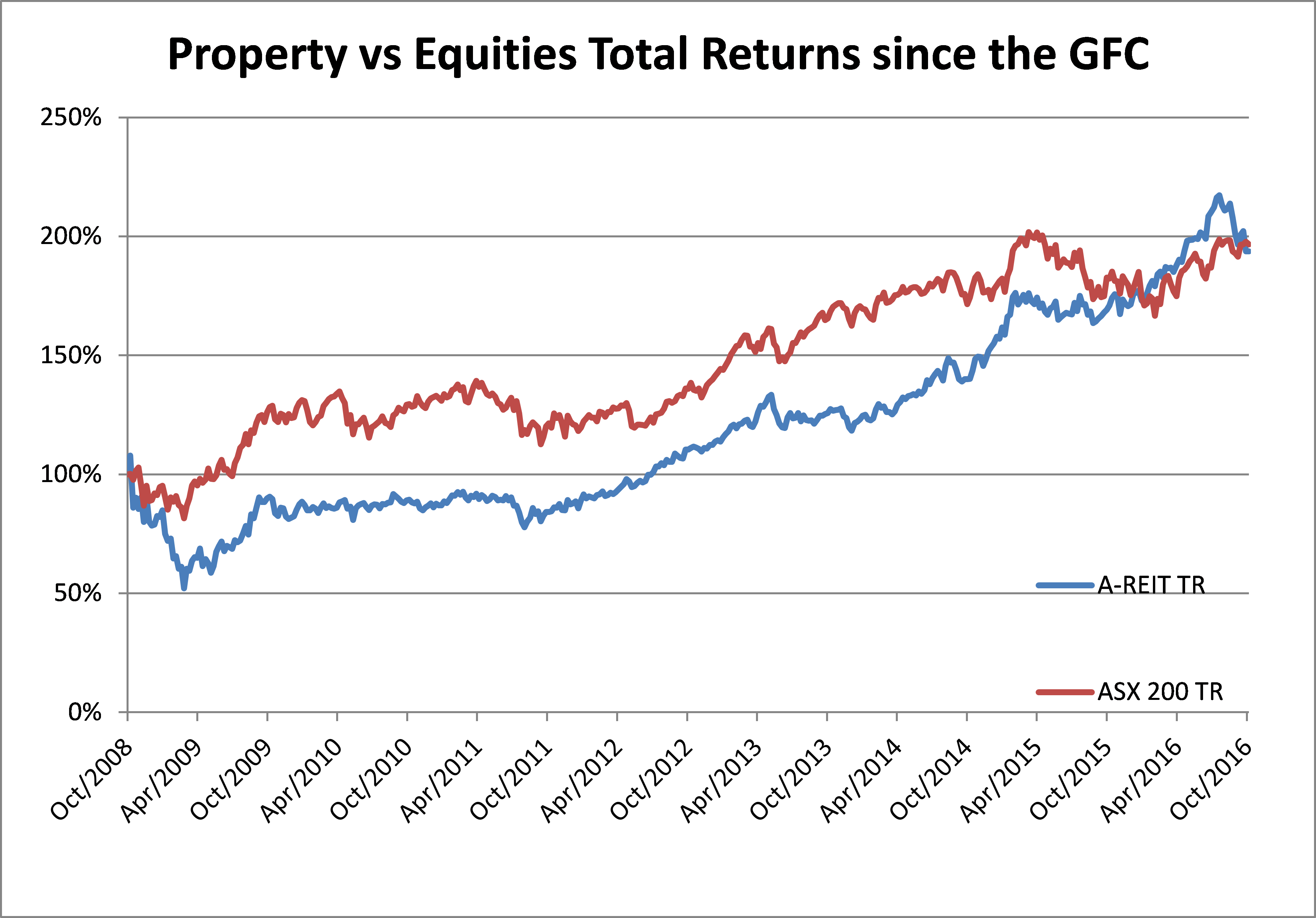

The charts below illustrate the performance of LPTs vs. equities since the GFC and over the past two years. After falling heavily in 2008 and 2009 and then tracking the broader market until 2013. Listed property has outperformed equities over the past three years and has recouped the underperformance coming out of the GFC. The key catalysts that pushed the sector higher were under-valuation, trust-reducing interest costs by refinancing high-cost GFC-era debt, extensive buy-backs below net tangible assets (NTA) and relatively high yields for Australian Trusts. Additionally, the effects of quantitative easing had push down interest rates and stimulated the interest in Australian commercial property from global investors. We see that these key catalysts have been now played out.

Over the past quarter, the sell-off in the Listed Property sector has had little to do with underlying property fundamentals, but rather the result of wider macroeconomic factors such as rising bond yields in anticipation of global rate hikes in the future. Other defensive sectors such as infrastructure and utilities and that are viewed bond proxies were similarly sold off.

Recent Activity in the Listed Property Sector

In 2015 mergers and acquisitions activity in the global listed property market was almost US$160 billion, which is very close to the previous peak in 2007 and this has been mirrored albeit on a smaller scale in the the Australian listed property market. In 2016, corporate activity in this market continued to be strong (allowing property investment bankers to upgrade their Porsches and Ferraris to a Tesla), though at a lesser pace than 2014 (Westfield restructure and the Dexus bid for Commonwealth Property Office) and 2015 ($12 billion Novion merger with Federation Centres to create Vicinity). Over the last year, we have seen Dexus bid for Investa Office Trust and a bidding war for GPT Metro Office Trust that was ultimately won by South African-backed Growthpoint Properties.

On the IPO front this week we saw Charter Hall pull the IPO for Australia’s largest ever property sector float the $1.1 billion Charter Hall Long WALE REIT. We looked closely at this IPO for the AUP fund but declined as the pricing was too high relative to comparable listed trusts.

Around the Grounds

Retail (61% of LPT Index)

Discretionary retail continues to adapt to the challenges of digital competition to bricks and mortar, with retail landlords changing their tenant mix to include more personal services and food outlets, areas that face minimal impact from the internet. Retail landlords have been quite fortunate in that the demise of chains such as Borders Bookstores and Dick Smith has been offset by the entrance of foreign retailers into the Australian market (H&M and Zara). Occupancy across the retail sector remains strong at 99%, and the trusts have reported improving retail sales aided by a decline in petrol prices, greater inbound tourism courtesy of a falling AUD and the impact of falling mortgage rates on disposable income.

Non-Discretionary Retail has recently begun to underperform discretionary retail, as spending growth on staples (food and liquor) has stagnated due to falling inflation and declining grocery prices as the battle for market share between Woolworths, Coles and Aldi has intensified.

Office (17% of LPT Index)

The strength of the office market, particularly in Sydney, has surprised the market, with demand tightening as vacancy declines from 11% to 5%. Two years ago, the consensus view was that 2016 and 2017 rents would be under pressure in the Sydney office market as Lend Lease’s commercial towers at Barangaroo released 320,000 m² of prime office space onto the market. What was missed was the impact that this development had on new construction and the quantity of space taken out by the resumption of land for the Sydney Metro line and the residential conversion of existing office towers. Indeed Aurora’s offices in 1 Alfred Street Circular Quay, which was sold to China's Dalian Wanda Group, is going to be knocked down in December to be developed into high-end apartments. While the Trust has benefited from being overweight office trusts, we have been surprised at the strength of the market, owning large positions in Investa Office and GPT Metro Trust due to our view that they were both acquisition targets rather than a bullish call on the Sydney office market.

According to the Property Council of Australia (PCA), overall office vacancy in Australia stands at 10.5%, with strength in Sydney (5%) and Melbourne (7%) being balanced against Brisbane (17%), Perth (22%) and Adelaide (14%).

Residential (4% of LPT Index)

The strength in the residential market in Sydney and Melbourne has been mirrored by the performance by the major residential developers Mirvac and Stockland in 2016. The sector has been buoyed by two rate cuts in 2016 and has ignored measures designed to curb foreign purchasers of residential real estate. Looking forward, we have minimal exposure to this sector due to concerns about the developing oversupply of apartments in 2017 and 2018 and rising settlement risks.

Industrial (18% of LPT Index)

While the industrial sector has enjoyed cap rate compression that has led to higher asset prices, this space could be tougher in the future as increased supply hits the market (+500,000 m2 in Brisbane and Melbourne, +700,000 m2 in Sydney under development). The industrial trusts, as well as certain office trusts, have been boosting their earnings by generating development profits from re-zoning industrial property to residential. As the residential market moderate, these development profits will be tough to sustain.

Aurora’s View

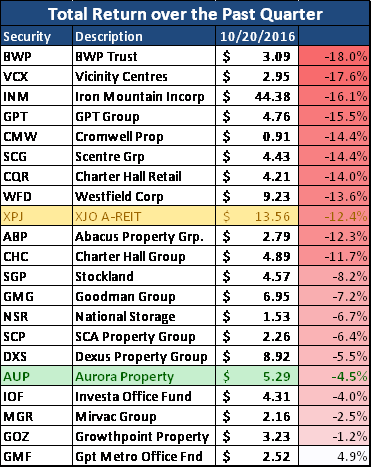

The 12% fall in the sector over the past quarter has restored some valuation sanity to the property sector, but from the below table one can see that the falls have been broad based. The Trust has performed as expected during this correction due to our portfolio strategy of populating the portfolio with higher quality domestic rent collectors combined with a derivative overlay strategy to enhance income should outperform in this market. We see that the majority of returns over the next 12 months will come from distributions and income from writing call options over existing holdings. The sector currently trades at a +25% premium to net tangible assets (excluding Westfield Corporation), 16x forward PE and 5.0% yield.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap & Praemium. Atlas' Australian Equity Income Fund (ASX:AFM01) provides quarterly income with low volatility. Click follow to be the first to get my next wire.

3 topics

6 stocks mentioned

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Atlas is a boutique investment manager focused on income-related strategies in Australian Equities. The Atlas Concentrated Australian Equity Portfolio is a managed discretionary account (MDA) available on Hub24, Netwealth, Macquarie Wrap &...

Expertise

Comments

Comments

Sign In or Join Free to comment