What’s next for retail REITs?

If you’ve been to your local shopping centre lately, well, I’m surprised. Deemed essential services, they remain open but have the feeling of a ghost town. Footfall, as visits are known in the trade, has been in freefall. Supermarkets are buzzing but discretionary retailers are closing their doors, despite no legal obligation to do so.

Footfall in freefall

When revenue is next to nothing and no date has been set for a return to normal trading, whatever that looks like, slashing costs is now the only option. Staff were the first to go, with Flight Centre announcing the closure of half its global stores with the loss of 6,000 jobs worldwide (1).

Other retailers, including Premier Investments, owners of Jay Jays, Smiggle and Just Jeans, has taken the “nuclear option” in the words of the Australian Financial Review, planning to stop paying rent altogether (2).

While tenants make the case for rent holidays and reductions, John Gandel, who owns half of Chadstone, Australia’s largest shopping centre, is reminding them that rent is “a legal obligation” (3). It’s a measure of how much has changed in a few short months that this point needs to be made in the first place.

Footfall isn’t the only thing to have collapsed. Through March, Westfield owner Scentre’s share price fell 54.8%, while Vicinity Centres the owner of the other half of Chadstone fell 52.1%. The REIT sector, a traditional safe haven, now looks anything but. The S&P/ASX300 AREIT index declined 35.2%, far more than the ASX300 equities index which fell 20.8% in the most severe market sell off since 1987. While markets will remain volatile for some time, it’s worth noting Scentre is up 27.5% and Vicinity 27.3% to 16th of April as investors begin to recognise the stocks are themselves on sale and that worst case scenarios look less likely as we progress through the COVID-19 crisis!

The concerns expressed in such falls is more than tenants reneging on their obligations over the next few months. It also includes the fear of dilutive capital raisings, a feature of the global financial crisis (GFC), and the uncertainty over what effects an extended lockdown might have on the role shopping centres play in a modern, consumption-led society.

Maybe it will accelerate the growth of online retail? Maybe in future people will be reluctant to pack into flagship centres like Westfield Sydney City and Chadstone on a Sunday? And maybe those rent reductions now being negotiated will become permanent rather than temporary?

These are all concerns one could not have imagined three months ago. At a time when uncertainty is already high, retail has become a byword for it. The current share prices of Australian REITs, most of which are trading at significant discounts to net tangible asset values, tell us as much.

Looking beyond the immediate chaos

We could panic, like many investors did. Or we could look at the facts and try and see past the chaos. The latter is our preferred option.

In response to the uncertainty, bond yields rose significantly in March (but have since stabilised around pre-lock down levels) which didn’t help the already under pressure AREIT sector. Add to this concerns around the prospect of dilutive capital raisings. AREITs appeared to have little going for them hence the indiscriminant selling that ensued.

Capital raisings can’t be ruled out (we have seen two already, however both were at <10% discount to NTA and were viewed as opportunistic balance sheet fortification) but there are a few salient facts that suggest these fears are overdone, more a function of historical experience than current reality.

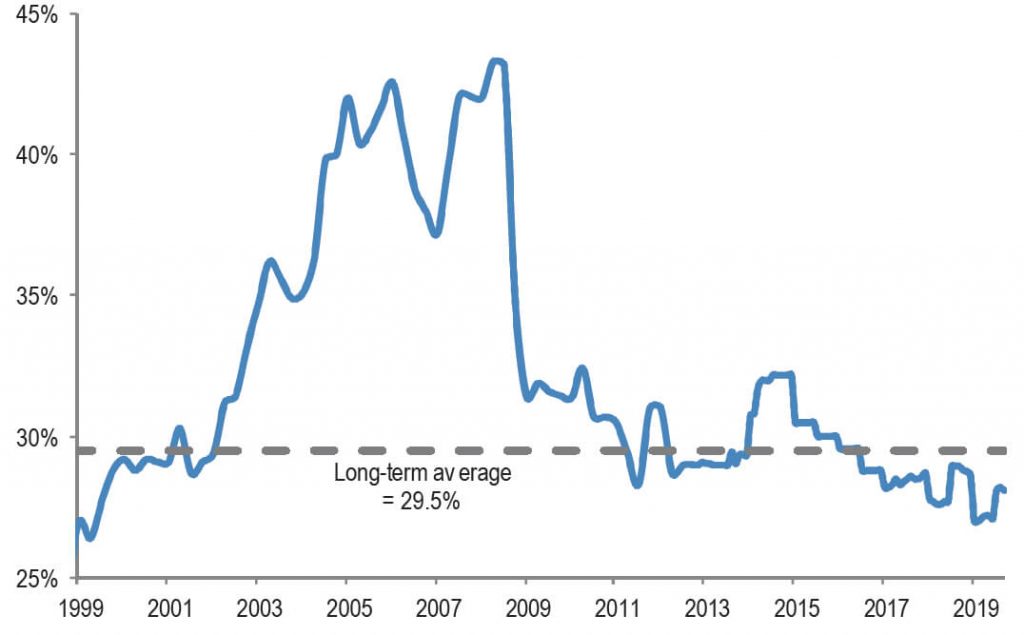

Debt is lower, more diversified and longer in tenure

AREIT gearing is now much lower than it was at the time of the GFC. In 2008, debt levels were around twice as high with funding sourced mainly from domestic banks using short duration loans. This was not prudent, as events subsequently proved.

JP Morgan research shows how REIT sector gearing has declined since the GFC (see Chart 1), to the point where it is now lower than the average of the last two decades.

REIT Sector weighted average gearing

Source: JP Morgan 21 March 2020

It is to the sector’s credit that it has spent the past decade getting its house in order with lower levels of debt but also more diversified funding sources and improved debt expiry profiles, both of which support the proposition that the prospect of future capital raisings are more distant than investors currently expect.

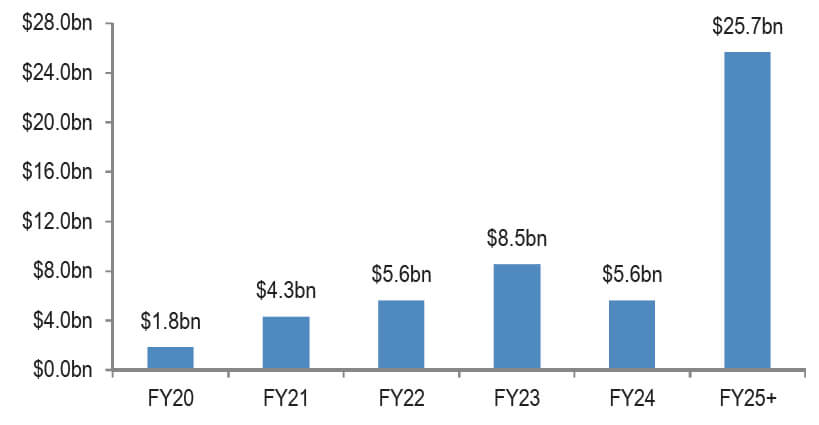

Let’s first examine the debt expiry profile, again using JP Morgan data. The jargon belies an important distinction; if you owe the bank $100m and it needs to be repaid in June, that’s a bigger problem than if it needs to be repaid in 2022, when shopping centres will, in all likelihood, be full of shoppers.

As Chart 2 shows, less than $2bn in AREIT sector debt is due to be repaid this financial year. And of the total $51.5bn of estimated debt, half isn’t due to be repaid for five years or more. Add to this the fact that several AREITs have raised additional debt over recent weeks to ensure they can cover FY20 and in some cases FY21 repayment obligations.

REIT debt expiry profile

Source: JP Morgan 21 March 2020

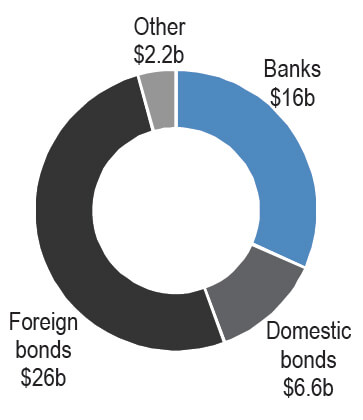

In terms of funding sources (see Chart 3), AREITs have also diversified their debt mix since the GFC. Of the $50bn+ sector debt, about half now comes from foreign bonds, while domestic bonds account for another 12%. The reliance on domestic banks as a source of debt has been greatly reduced, which means the sector can’t be easily squeezed by one funding source or another.

REIT debt mix

Source: JP Morgan 21 March 2020

AREIT sector debt is lower, more diversified in terms of sources and is longer in tenure, the average debt term being almost six years, meaning it isn’t due to be repaid for many years. These factors mean that REITs are far better placed than they were in the GFC and that the chances of highly dilutive capital raisings are low. In the words of JP Morgan, “We believe the liquidity picture is far superior than recent pricing suggests” (4).

Shoppers will return and the rent will be paid

Of course, with retail outlets closed and shoppers staying away, sector earnings this year are highly unpredictable. But there’s every reason to suggest they will normalise at some point in the next year or two. The reasons for this have less to do with facts and figures than with historical norms and the predictability of human behaviour.

The first thing history tells us is that pandemics end. Things may seem apocalyptic right now but like SARS, MERS, Ebola and a host of other diseases, Covid-19 will pass. And when it does there’s every chance people will go shopping.

Whilst it’s true that being forced to shop online in isolation may accelerate the growth of online retailing, history also shows that markets have been around for millennia, not just as a place where people exchange goods but also where they socialise, eat, argue and simply hang out. Pandemics came and went but markets, bazaars and high streets outlived every one of them.

Shopping centres, featuring restaurants, gyms, cinemas and childcare centres amongst other things, are their modern equivalent. They serve a functional community purpose, of course, but also facilitate the exercise of one of humanity’s deepest traits, to gather together and do stuff, even if it’s to try on jewellery or eat fried chicken.

Given our unique and current circumstances, cooped up in houses and apartments not seeing friends and relatives, it’s tempting to be seduced by the idea that our current daily habits will endure once the lockdown is lifted. AREIT investors would do well to appreciate the historical body of evidence that they probably won’t.

Shopping has long been a communal experience. It’s highly likely that it will remain that way. Some chains might not survive this period but others will rise to replace them, as has been the tradition. If you’re invested in quality well managed shopping malls, you have much less to worry about than you think. Be patient and let time do its work. The shoppers will return, the rent will be paid and eventually, AREIT share prices will again come to reflect the yield they’re likely to deliver over the long term.

Access a steady stream of reliable income

To find out more about the income options that APN Property Group provides, please click the 'CONTACT' button below.

1. Sky News 26 March 2020

2. AFR 26 March 2020

3. SMH 27 March 2020

4. JP Morgan 21 March 2020

2. AFR 26 March 2020

3. SMH 27 March 2020

4. JP Morgan 21 March 2020

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Pete joined Dexus Real Estate Securities in 2006 and is responsible for the management of the suite of real estate securities funds. With more than 19 years of experience in financial markets, Pete brings a unique knowledge set, completing Masters-level academic research papers on both commercial real estate cycles and global property securities.

Featuring

Pete Morrissey,

Dexus

Pete joined Dexus Real Estate Securities in 2006 and is responsible for the management of the suite of real estate securities funds. With more than 19 years of experience in financial markets, Pete brings a unique knowledge set, completing Masters-level academic research papers on both commercial real estate cycles and global property securities.

........

This article has been prepared by APN Funds Management Limited (ACN 080 674 479, AFSL No. 237500) for general information purposes only and without taking your objectives, financial situation or needs into account.

1 topic

2 stocks mentioned

Pete joined Dexus Real Estate Securities in 2006 and is responsible for the management of the suite of real estate securities funds. With more than 19 years of experience in financial markets, Pete brings a unique knowledge set, completing...

Expertise

Comments

Comments

Sign In or Join Free to comment