What’s the endgame of all this money printing?

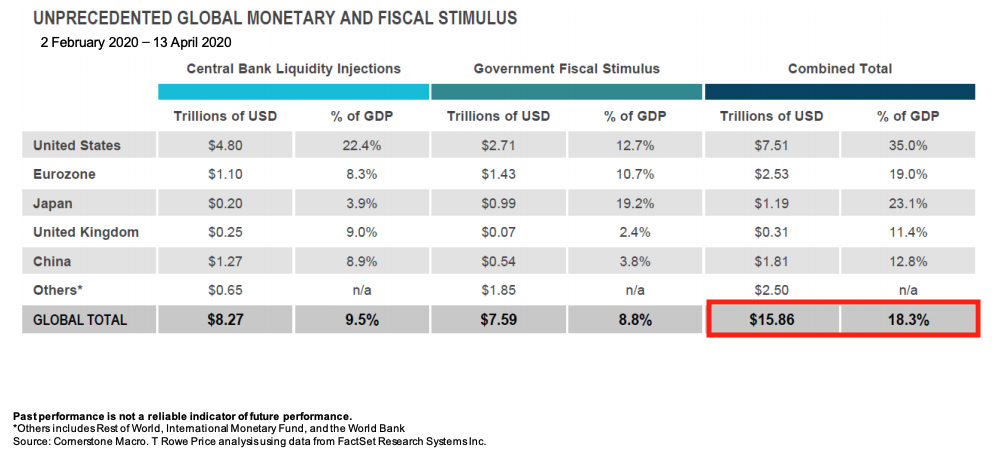

I’d like you to take a quick guess. How many dollars’ worth of fiscal and monetary stimulus do you believe has been pumped into the global economy since the start of February 2020?

The answer is contained in the table below but try and have a go before looking. US$5 trillion? Too low. US$7 trillion. Not even halfway!

SOURCE: T.ROWE PRICE

A mind-warping nearly US$16 trillion or 18.3% of GDP. For perspective, even in the GFC the US and UK stimulus packages were below 10% while in World War II that figure was ~25%.

While readers would be aware that stimulus measures in response to COVID-19 have been unprecedented, to say the least, what none of us can fathom are the long-term consequences of running the printing presses non-stop.

Scott Berg, Portfolio Manager at T. Rowe Price, remarked at a recent webinar that this is the “million-dollar question” and whether it’s 10 or 20 years down the track, there will be a price to pay.

“ My personal view is the history of the world has shown that there is a price to be paid for these things, and that there is no free lunch in economics. There is no magic money tree that means you can just spend as much money, print as much money as you want, and it not to have an impact.”

To frame his thoughts on the possibilities, Berg cast his mind back to the beginning of his career in 2003 when Japan was in the thick of dealing with economic stagnation; its 10-year bond yielded 1.5% (whilst Australia and the US were at 6.5% and 5%, respectively) and the central bank had recently adopted quantitative easing. The ruling party had even considered directing the Bank of Japan to buy equities, which it eventually did in 2010. Fast forward till today, and who would have thought the developed world would be catching up to Japan?

Berg notes that the consequences of QE have so far been inflationary only for equity, bond and property prices, but not for wages and consumer goods. Alas, he’s of the view that governments will not relent until they bring inflation back into the real economy to deal with the debt that’s building up in the financial system.

“To deal with all debt that’s been built up here you’ll either have to have higher taxes, monetisation of that debt, debt forgiveness or inflation. My guess is they will try and keep rates low and hope that inflation comes back into the system because in history that's been the least painful way to deal with it.”

Stocks have bottomed

Notwithstanding the risk of an uncontrolled second wave of COVID-19 or a mutation into a deadlier version that kills young people as easily as old, Berg believes that equities bottomed in March.

Despite a torrent of depressing news and data due over the coming period, he says that the S&P 500 typically troughs 3-6 months before consumer sentiment and manufacturing indices hit their worst.

“We do not believe that this is a crisis of long-term cashflow generation and we do believe a new equity cycle will be born of today’s economic environment.”

During the call, he discussed three investment themes.

Buying financials and commodities

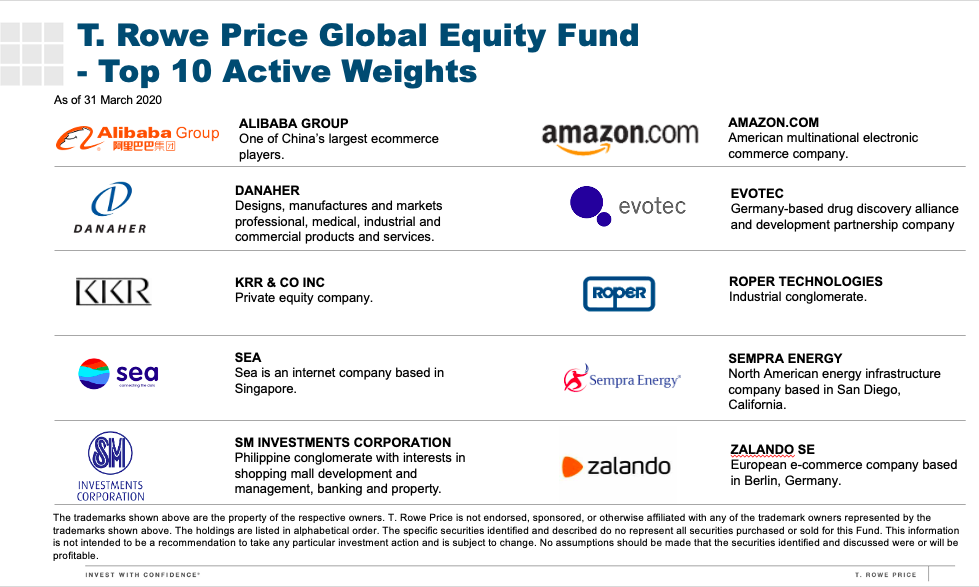

To position itself to benefit from a potentially inflationary environment, Berg has taken some money off the table from high-flying stocks like Amazon and Tesla and into the underperforming financials and commodities sectors within the growth-oriented T. Rowe Price Global Equity Fund, which has over $3 billion in assets.

“Financials have been the biggest single addition to the portfolio. They have sold off incredibly hard. If rates stay here or the world stays here, and we just follow a normal path coming out of a recession... they offer that very cheap optionality where if you were to get a change and get a bit more inflation, these stocks would be absolute gangbusters."

Avoiding energy

One area that Berg is avoiding is energy. While the mantra “lower for longer” is connected to rates, it can now also be applied to oil prices, which have been disrupted by both a supply shock and demand implosion and there is far too much uncertainty on whether demand will recover to pre-COVID levels.

Technology to shine

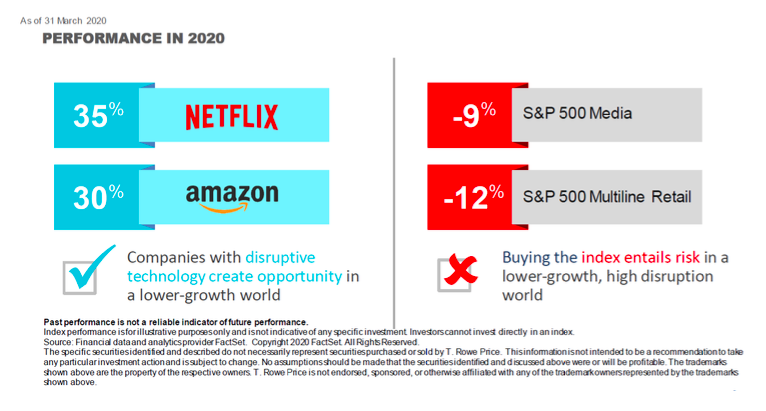

The portfolio remains well-diversified with significant exposure to growth companies. Berg notes that many investors who continue to balk at valuations of tech shares could be missing out on significant gains in the years ahead, as COVID-19 has further entrenched themes such as e-commerce and streaming services into our daily lives, setting up tech companies for a brighter future with even stronger earnings profiles in a lower growth world.

"Going into this crisis, a lot of people would've said that Netflix and Amazon were expensive stocks, right? But we've made the point, their business, their underlying profit and cash flow growth, and the scale at which revenues are growing is so different to everything else, that it's more deserved."

He says that in some cases tech shares are now offering better value than consumer staples stocks, which have experienced a temporary boost in demand due to stockpiling.

“Market valuations are particularly attractive in the context of interest rates and bonds. Google, for example, is trading on 20x earnings when you take out the cash they have, whereas Walmart which is not growing nearly as fast is trading on 30x. Many growth companies like Amazon and Shopify are trading at record highs as the pandemic accelerates a number of secular trends out there.”

Never miss an update

Want to see previous insights from Scott or get notified when he publishes wires in future? Follow him here.

Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Featuring

Scott Berg,

T. Rowe Price

Scott Berg is the portfolio manager for the T. Rowe Price Global Growth Equity Strategy.

........

This article is for informational purposes only and should not be considered financial advice. The article may contain the views or opinions of third party contributors to Livewire Markets. These contributors have not considered your objectives, financial situation, or needs. The information in this article should not be relied upon as a substitute for personal financial advice. Livewire Markets recommends that you seek independent advice before you apply for any financial product or service. Livewire Markets is exempt from requiring an AFSL under ASIC Regulatory Guide 36, section 66.

3 topics

2 contributors mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment