When does too much of a good thing break bad?

In this article I am going to discuss the composition of the S&P/NZX 50 index, which is considered New Zealand’s principle gauge of how the New Zealand share market is performing, and is the main proxy for a passive, diversified exposure to the New Zealand equity market.

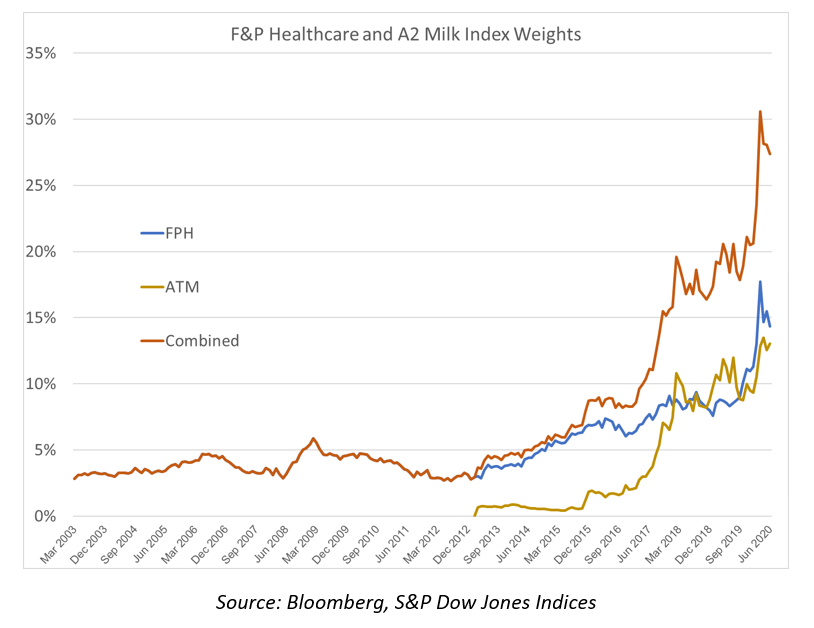

In its current format, the S&P/NZX 50 index weightings go back to 2003. At that time, Fisher & Paykel Healthcare was a relatively recent spinoff from Fisher & Paykel Appliances and had a solid initial index weight of 2.8%. Spinoffs often make for interesting investment opportunities and Fisher & Paykel Healthcare proved so. Back in 2003, A2 Milk was a recent start up and not yet a member of the index. As you can see in the chart below, it joined the index in 2013.

In 2003 the combined weight of the two companies in the S&P/NZX 50 stood at 2.8%. Jump forward 17 years to 2020 and their combined weight recently topped 30%. The chart below shows how their index weights have changed over the period.

Over the past four years there has been a significant increase in the index weights of A2 Milk and F&P Healthcare, which has seen their combined weight treble from 10% to 30%. The last surge has been as a result of their very strong performance during the recent market weakness related to Covid-19.

So, can an index become too concentrated to serve its purpose as a proxy for a diversified exposure to equities? The best example of an index that became too concentrated, that I know of, was the Helsinki Stock Exchange in 2000. At that time, Nokia had a 70% index weight, which effectively rendered that share market index useless. An active manager was going to be largely judged on one investment decision and a passive investor pretty much got exposure to one company. Neither purpose of a properly functioning index was being served.

Interestingly, the early 2000’s was also a time that New Zealand was grappling with an index concentration issue of its own. New Zealand Telecom peaked at a little over a 30% index weight. As it turned out that was a real headwind for the New Zealand market as it became apparent that the AAPT acquisition in Australia was a dog and, even worse, tighter regulations in New Zealand were about to shred earnings.

There can be little doubt that a 30% concentration in two companies is a level that is starting to reduce diversity. Many commentators in the US are currently amazed that the top 5 companies in the S&P 500 index make up 21% of that index. Microsoft, Apple, Amazon, Facebook, and Google account for 21% of the index. It is a level of concentration that they are not familiar with and some commentators are concerned about a lack of diversity there. By way of comparison, our top 5 companies including A2 Milk and F&P Healthcare are close to touching 50%.

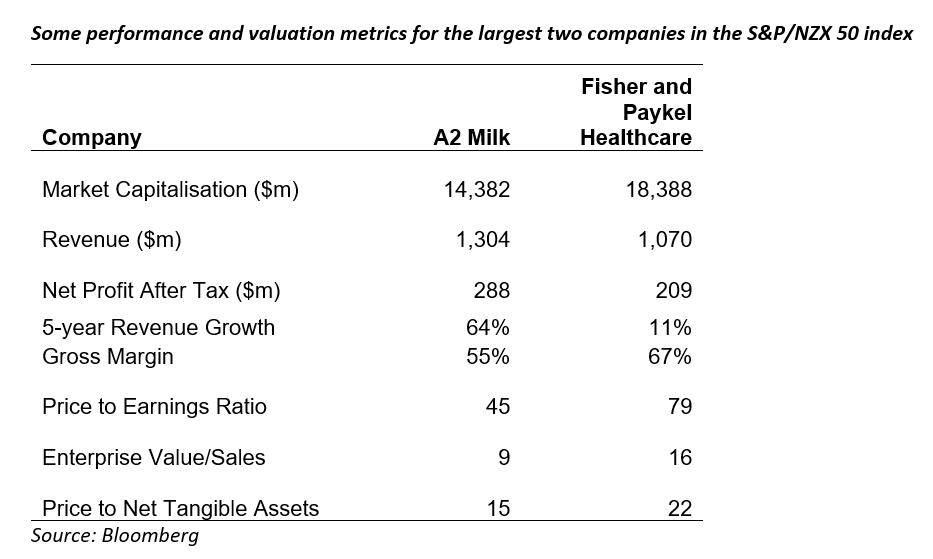

In our opinion, A2 Milk and F&P Healthcare are good companies. But they are currently priced with optimistic growth expectations. Both companies are cash generative and highly profitable, with growth options and have no current clouds over their business models. But their share prices reflect that and trade on the expensive side. A good company can still be a bad investment if you pay too much for it. And future price movements of these two companies will weigh heavily on S&P/NZX 50 index returns.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

........

Castle Point has taken all reasonable care in the preparation of these articles, however accepts no responsibility for any errors or omissions contained within. Past performance is not necessarily an indication of future performance. Opinions expressed in these articles are our view as at the date of issue and may change

5 topics

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Stephen has over 25 yrs investment experience & co-founded Castle Point, a NZ boutique fund manager, in 2013. Prior to that he worked at funds management companies in Auckland, London & Edinburgh. Castle Point WINNER FundSource Boutique Manager 2019

Expertise

Comments

Comments

Sign In or Join Free to comment