Where performance and quality meet

The volatility in markets this year, at a time of rising fear and panic over the COVID-19 outbreak, has led many investors to take an immediate focus on capital preservation and short-term performance. However, all the long-term, structural and systemic reasons why we remain committed to investing on a more socially responsible footing have not gone away.

This month, we take a look at how ESG (environment, social and governance) investments have performed through the recent market volatility. Using MSCI ESG analysis we show that ESG/SRI (socially responsible investing) equity indexes have outperformed their non-ESG/SRI counterparts through the recent Q1 2020 market correction and over the past five years. We also look at how sustainable equity funds have recently measured up. Finally, we highlight the nexus between ESG and quality investing in the equity space, and draw attention to the A, AA and AAA ESG ratings across our equity lists.

First, an update on some adjustments to our asset allocations

Before we take a closer look at how SRI investments have performed through the recent market volatility, there are a number of adjustments we have made to our strategic and tactical asset allocations this month.

Tactically, we remain overweight equities relative to fixed income. But given the rally in equity markets in May, we have now trimmed this position. We have reduced emerging market equities to neutral (as concern about the pandemic’s spread in this region grows and renewed US-China trade war risks have risen) and moved modestly overweight international corporate credit. Here, credit spreads have responded much less positively than equities to the ongoing gradual improvement in the economic outlook.

Our strategic asset allocation weights have also been adjusted following our annual review of medium-term return expectations across asset classes.

Firstly, we have again increased international relative to domestic equity, reflected in an increase to emerging markets.

Secondly, within alternative assets we have increased the weight of both real assets and private equity (at the expense of hedge funds).

Finally, for our single asset portfolios, we have added real assets for yield and private equity for equities.

COVID-19 may have accelerated SRI thematics

The trend toward investing using ESG criteria—which we believe to be integral to maximising our clients’ long-term financial performance—is only likely to have been accelerated amid this year’s climate events, the pandemic crisis and the attention on how corporates have managed their activities and employees through this recent period of economic upheaval.

Sustainability themes, another key pillar under our SRI framework, are

only likely to engender more focus, specifically sanitation and healthcare, reducing

our carbon foot-print and how we can protect the most vulnerable in our societies for the benefit of all stakeholders, employees and investors alike.

Recent developments, moreover, have reinforced the importance of SRI. The virus has highlighted the interconnectedness of our global and domestic economies, environment and society. As a community, we should now spend more time reflecting (and questioning) the entrenched global model birthed in linear production and supply chains which focuses society on short-term consumption. As Simon O’Connor from the Responsible Investment Association Australasia (RIAA) notes, scenarios such as the 2020 pandemic “are core business for responsible, ethical and impact investors, who spend much of their days analysing and assessing causes of disruptions to valuations that sit off the balance sheet: the ESG and ethical issues are fundamental to a holistic understanding of what moves markets”.

How have ESG investments performed through Q1 2020?

Over recent years, we have highlighted several times that ESG investing (and increasingly investing that is focused on sustainability and impact) does not have to come at the expense of returns. Arguably, capital was attracted initially to investments in the SRI space with market-based returns, thereby driving the increased expansion of such opportunities in today’s market. Demand will keep creating and developing its own supply.

In addition, there is the inseparable alignment between the age-old investment factor of quality and ESG as a tool to maximising long-term financial performance. Quality and ESG are in many aspects two sides of the same coin.

We discuss this in more detail further on.

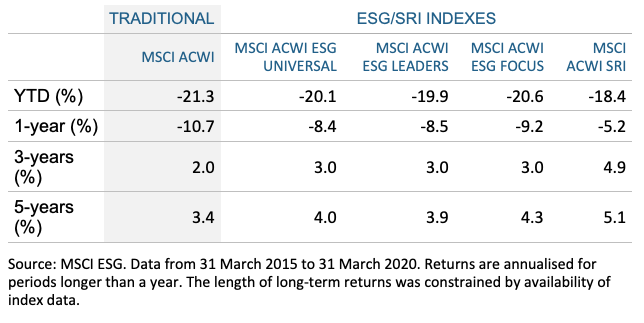

Equities—ESG/SRI outperformed traditional equity indices

There is now increasing evidence of the resilience of SRI investments through the most recent COVID-19 crisis and market volatility. The MSCI cohort of ESG/SRI equity indexes outperformed their non-SRI/ESG counterparts by an average of 1.6% in Q1 this year during the height of market turmoil (see the table below). We see an even more stark result for the BetaShares Australian Sustainability Leaders ETF (FAIR), which beat the S&P/ASX 200 index by over 7% through the first quarter of this year.

Turning to fund managers and looking to the US where there is a good cohort to compare, our analysis suggests sustainable US equity funds outperformed their Morningstar category peers on average calendar year-to-date, led by US large-cap funds. Some of our most exciting ESG and sustainable managers have also outperformed through this recent period of volatility. Our SRI large-cap global equity managers outperformed peers and benchmarks on average over the year to April 2020, delivering -1.3% versus -5.7% for the index. Our key SRI domestic small and mid-cap equity funds also significantly outperformed.

Performance of traditional equity index versus ESG/SRI indexes

Of course, the tendency for SRI funds to be

overweight many of the areas that have benefited from the recent pandemic (and

underweight those that have been harmed by it) will have supported their

short-term outperformance. This includes thematic underweights to oil and

banking and thematic overweights in healthcare, digitalisation and technology.

Nonetheless, the same MSCI cohort of ESG/SRI equity indexes has also

outperformed its counterparts over three and five years to the end of Q1 this

year (though outperformance was narrower at 1.2% and 0.9% respectively according to MSCI in the above table).

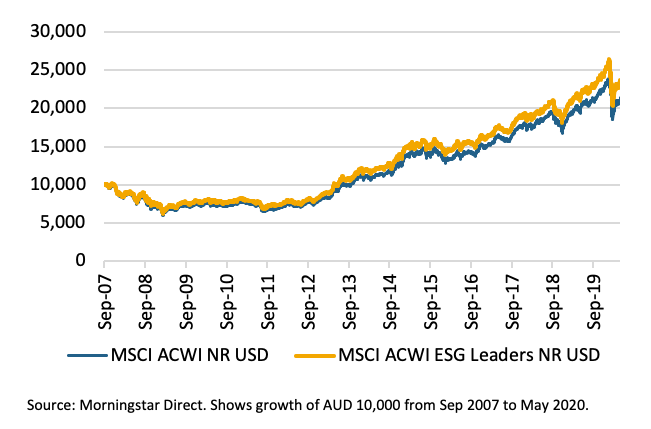

To show this longer-term outperformance, the first chart below compares traditional global equity investing with ESG investing, analysing the MSCI All Country World index and the MSCI All Country World ESG Leaders index. The ESG Leaders index also excludes companies with material involvement in industries such as alcohol, gambling, tobacco, nuclear power and weapons, giving it an additional ethical overlay.

As the chart shows, from September 2007 to late May 2020, the ESG Leaders index outperformed its parent index, delivering an annualised return of 7.0% versus 6.2% for the parent index. Importantly, it also did this with a little less volatility (35.5% versus 36.8% respectively), protecting on the downside during periods when equity markets were weak.

MSCI All Country World ESG Leaders index versus its parent

Fixed income—return differentials have been smaller

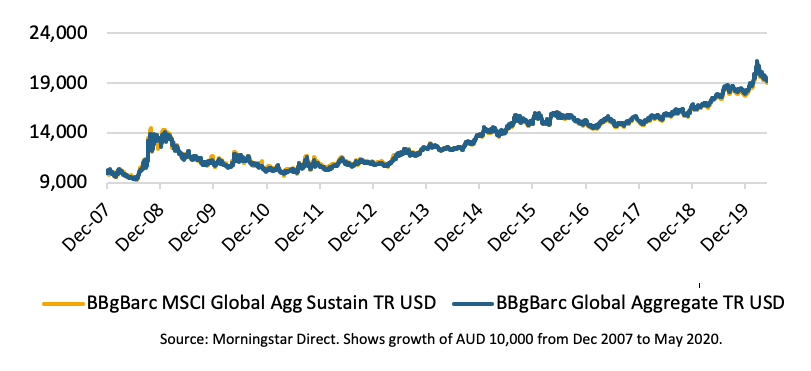

For fixed income broadly, which is a lower yielding asset class, the return differentials tend to be much smaller. However, our analysis shows that long- term returns do not have to be sacrificed, and risk (and volatility) can be mitigated by focusing on sustainable bonds. According to Goldman Sachs US credit research, when looking at green bonds, they found “no evidence that green bonds underperform their non-green peers” in the secondary market.

As shown in the chart below, the Bloomberg Barclays Global Aggregate index and the Bloomberg Barclays MSCI Global Aggregate Sustainable index, from December 2007 to May 2020, delivered similar returns (the Sustainable index delivered 5.42% while the Global Aggregate index delivered 5.48%). Volatility was also similar, though the Sustainable index outperformed during ‘risk-off’ periods, such as in 2008, 2011 and 2020.

Sustainable and traditional bonds have delivered similar returns

Quality and ESG—two sides of the same coin

Financially high-quality companies have consistently outperformed their low-quality counterparts in both developed and emerging markets. Compared to their peers, they are more profitable, have more conservative balance sheets and generate greater cash flow over the longer term.

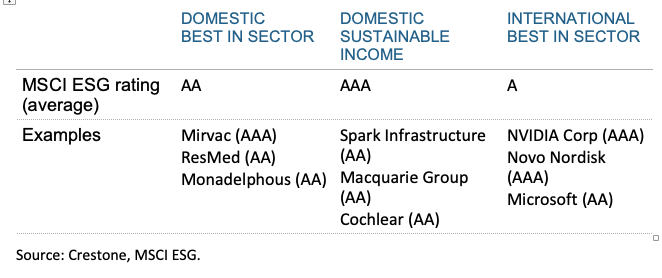

Our core equity lists (international, domestic and sustainable income) focus on identifying high-quality companies that, over time, have an emphasis on long-term stability and consistency of metrics. Our lists undergo a rigorous screening process that ranks stocks within sectors according to a number of financial ‘buckets’, including profitability, top-line growth, capital intensity and balance sheet strength.

While our core equity lists have not explicitly incorporated ESG into the stock selection framework, they still aggregate to A, AA and AAA MSCI ESG rating scores, respectively. Why is this so? In essence, quality (as defined by our ranking criteria) and ESG are two sides of the same coin.

How the Crestone equity lists score from an ESG perspective

Integrating ESG into the stock selection process is more intertwined with financial forecasting than many investors realise. For example, a company that uses cheap child labour not only faces reputational damage but, in forecasting future earnings, one must make an assessment on the likelihood of this cheap source of (human) capital continuing and, therefore, the prospect for margins going forward. In many respects, this means that ESG investing—and here there is a strong focus on the social—is not only about activism (and of course ethics) but also about the choices that companies make and how it will impact the future health of that company.

In other words, sustainability of financial returns can only be achieved by companies having an eye to various ESG criteria, including corporate governance. Having a proper Board structure that is independent, with strong shareholder protections and where executive remuneration is aligned to performance not only scores strongly on an ESG basis but, for most investors, is considered a necessary condition for strong financial oversight.

By default, companies that have proven themselves adaptable to change and focused on delivering superior financial performance are also, implicitly and explicitly, accounting for the risk and return associated with issues such as environmental change, employee and supply chain welfare and diversity of thought. That is, in order for a company to be financially successful, it must, at some level, be cognisant of the importance of ESG issues and, therefore, prudently manage investor capital to account for potential risks associated with these issues in order to deliver a desirable financial outcome.

What does the future hold?

Looking ahead, many of the themes we have mentioned, such as healthcare, digitalisation and technology (key long-term investment themes we flagged at the start of this year), as well as energy efficiency, are likely to be some of the growth sectors over coming decades. Technology, of course, will continue to be a growth sector. It is central to a sustainable economy for a number of reasons, including the delivery of large-scale energy efficiency tools to enable the management of both COVID-19 and potential future health crises (through telehealth, tracing, health monitoring to name just a few).

Compiled with contributions from Rachel Etherington (Investment Adviser) and Todd Hoare (Head of Equities).

Align your investment with your values

The desire to invest responsibly has never been stronger. At Crestone, we work with a wide range of investors who are looking to align their investments with their values. Click the 'CONTACT' button below to get in touch with us.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

........

General advice notice: Unless otherwise indicated, any financial product advice in this email is general advice and does not take into account your objectives, financial situation or needs. You should consider the appropriateness of the advice in light of these matters, and read the Product Disclosure Statement for each financial product to which the advice relates, before taking any action. © Crestone Wealth Management Limited ABN 50 005 311 937 AFS Licence No. 231127. This email (including attachments) is for the named person’s use only and may contain information which is confidential, proprietary or subject to legal or other professional privilege. If you have received this email in error, confidentiality and privilege are not waived and you must not use, disclose, distribute, print or copy any of the information in it. Please immediately delete this email (including attachments) and all copies from your system and notify the sender. We may intercept and monitor all email communications through our networks, where legally permitted

1 topic

1 stock mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

Ross vs the AI hype: her shocking prediction revisited

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets