Where we see opportunities in 2021

A furniture retailer, mining services company, listed property trust and health insurer are among companies that have either rallied, lagged or presented enticing buying opportunities in a COVID-marred 2020.

The market rally amid positive news on COVID-19 vaccine rollouts prompts us to reflect on our portfolio, which currently comprises three reasonably distinct groups of companies:

- Strong performers: Stocks that have rallied strongly from their lows and contributed most to the fund’s recovery;

- Laggards: Those whose stock prices are still well down on where they were pre-crisis and often have not rallied significantly from their lows, despite a material improvement in operating conditions; and

- New opportunities: New additions to the portfolio, where we have capitalised on the sell-off to invest in high quality businesses that we have always liked and have found opportunities to invest in at attractive prices.

In the following wire, I discuss the outlook for each of these three portfolio buckets.

Strong performers

Several investments have rallied strongly from their lows and contributed most to the recovery in the fund, yet our enthusiasm for these stocks remains. Many of these companies were the businesses that Auscap was buying most aggressively in late March and early April. While their share prices are up considerably since then, in most cases their earnings are up even more.

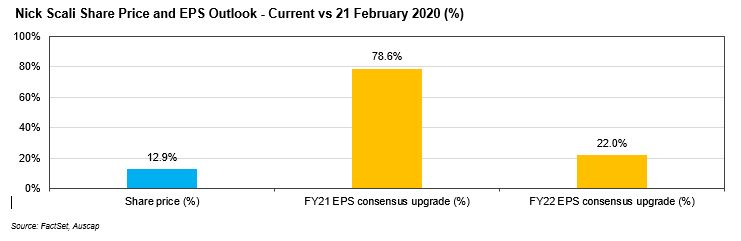

One example is Nick Scali, a business with one of the ASX’s highest return-on-equity ratios. The company is currently experiencing an extraordinarily strong trading environment, aided by fiscal stimulus and a reallocation of consumer spending towards the home. While these tailwinds are likely to subside, we are confident that Nick Scali’s outlook is positive. This confidence is driven by

- growth in online sales

- a significant store rollout plan

- category expansion

- an improved housing backdrop

- higher consumer confidence and potential acquisition opportunities.

Despite this strong trading environment and positive outlook, Nick Scali’s share price is currently only 13% higher than pre-COVID levels. After accounting for Nick Scali’s property ownership and current year cash generation, we estimate the company is currently trading on a price to earnings multiple of less than 10-times forecast earnings in FY22.

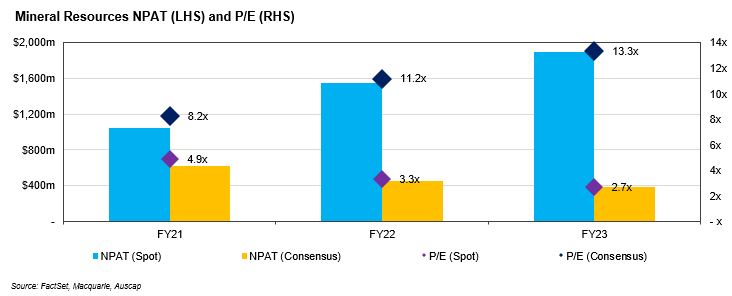

Another strong performer is Mineral Resources (ASX: MIN), which is up more than 80% since February. Since we discussed the stock’s appeal in our September 2019 newsletter, Mineral Resources has continued to expand aggressively. At the company’s November Annual General Meeting, CEO Chris Ellison outlined plans for significant iron ore production growth: “We believe without any doubt that over the next two-and-a-half to three years, we're going to double the entire MinRes business.”

“That's doubling in revenue, doubling probably in the number of people we employ, the tonnes we shift, and more importantly, doubling the bottom line,” said Ellison.

In addition to its exciting organic growth opportunities, Mineral Resources is leveraged to the currently buoyant iron ore price. We estimate that at the spot iron ore price, Mineral Resources is trading on a price to earnings multiple of less than 5-times.

We have a number of investments in this position, where the share price strength has been more than matched by improved financial performance. So, we remain excited about the valuation and growth outlook of our “strong performers” basket of companies.

Laggards

The second group of companies are those whose stock prices are still well down on pre-crisis levels, and which haven’t seen significant rallies over the last six months. This is despite their operating environment being considerably more positive than in March, with many experiencing a strong rebound in business activity.

An example is GDI Property Group (ASX: GDI), a real estate owner and fund manager with significant exposure to the Perth office market. Due to the impact of COVID-19 on office occupancy, GDI provided modest rent relief ($1.5m for FY20) to select tenants and its NTA decreased by 1.5% to $1.30 at 30 June 2020. This valuation attributes little value to its funds management activities, and significant development opportunities. But GDI is currently trading 26% below pre-COVID levels and at a double-digit discount to its net tangible assets, despite multiple data points suggesting the West Australian economy is performing strongly.

We think that over time, the market will realise that GDI’s operating environment has improved, and the discount is not warranted. Despite signs of renewed investor interest in some of the laggards during November, we continue to view valuations as attractive across this group of businesses.

New 0pportunities

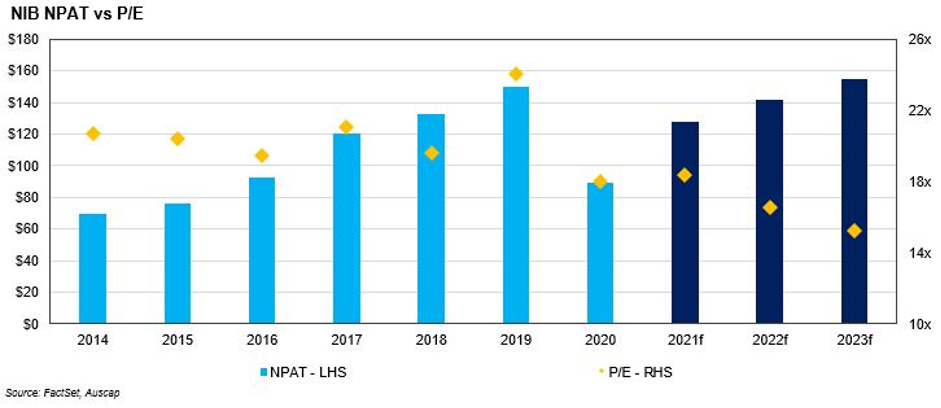

The third group of companies are new portfolio additions, where we’ve capitalised on the sell-off to invest in great businesses that we have always liked at prices we find attractive. One example is NIB Holdings (ASX: NIB), whose primary business of selling health insurance across Australia and New Zealand has proven largely resilient to COVID-19. But in response to APRA guidance, NIB took a material COVID-19 provision for these businesses due to the potential for a large catch up in claims in coming months.

Time will tell to what extent this provision is required. NIB also has two smaller divisions that were heavily impacted by COVID-19. One is an international inbound health insurance business covering international students and workers. The other is NIB Travel Insurance. Profit for these two divisions dropped from $42 million in FY19 to a combined $3 million in FY20. NIB is currently trading on an FY22 P/E multiple of approximately 16.5-times, which compares favourably to its historical average multiple and does not account for an eventual recovery in NIB’s COVID-exposed businesses. We anticipate that its earnings should improve as the impact of the pandemic on global activity recedes.

We will continue to monitor the economic data and developments in relation to the Fund’s portfolio closely, but we are encouraged by the forward indicators. The Fund’s current exposures we believe compare favourably to the broader market. They are high quality businesses with forecast earnings growth in excess of the market, trading with attractive valuation metrics.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short portfolio using Proprietary funds. Prior to 2007 he worked at Macquarie Bank within the Investment Banking Group. Tim is a CFA charterholder, a CMT charterholder, a Senior Associate of FINSIA, a Graduate of the Australian Institute of Company Directors (GAICD) and has a Bachelor of Laws (Hons) from the University of Sydney and a Bachelor of Commerce from the University of Sydney.

........

Tim Carleton is a Principal and Portfolio Manager at Auscap Asset Management (Auscap), a boutique equities long/short investment manager. This article contains information that is general in nature and does not constitute investment or any other form of advice. This article does not take into account the objectives, financial situation or needs of any particular person nor does it constitute a recommendation to be relied upon when making an investment or any other decision. You need to consider your financial needs before making any decision based on the information in this article and a person should obtain and consider the relevant disclosure document before deciding whether to invest in an Auscap fund. No part of this article is to be reproduced or disclosed without the prior written consent of Auscap. In relation to any MSCI data in this article, the MSCI data is comprised of a custom index calculated by MSCI for, and as requested by, Auscap. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Comments

Comments

Sign In or Join Free to comment