Why use a multi-manager framework in fixed income portfolios? Risk management is the key

The utilisation of multi-manager frameworks is often criticised as detracting from returns. However, focusing on return maximisation ignores the inherent uncertainty in financial markets and how utilisation of multi-manager portfolios can, if implemented appropriately, assist in providing a more robust framework for managing such inherent uncertainty.

What is the Investor’s Objective?

The assumption that the objective of all investors is to maximise returns is potentially misleading as this only captures part of an investor’s objectives. A focus on return maximisation as the key objective misses consideration that the path the returns from an investment strategy take to attain the ultimate objective is also of importance. In other words, investors who want to maximise returns (or excess returns when measured against a predefined benchmark), must also manage, though not necessarily minimise, the risk associated with attaining this intended outcome. Why is this secondary objective important? In order for investors to see an investment strategy through to the end, they must possess sufficient confidence that the strategy will deliver the desired outcome. A high level of volatility, both absolute and relative to peers, can undermine confidence that an outcome will be achieved and thereby induce excessive portfolio rebalancing. Ultimately, investors want to maximise the potential excess returns while managing, or even minimising, the potential for disappointment or failure to achieve their return target by a material margin.

The Limitations of Quantitative Analysis?

Having set the investors objectives, it is now necessary to establish a suitable framework for considering investment decisions based on what investors actually know at the time they are deciding on a particular investment strategy. It is in the establishment of a suitable framework that the statistical analysis of historical return characteristics can be misleading as it implicitly assumes investors know what happened over a certain time period. The ambiguity arises as any statistics utilised are actually calculated over a particular time frame and therefore only hold for that particular time frame. Only if investors can assume that the characteristics of the historical time frame will hold in the future can use of the statistics be relevant. However, with an uncertain future investors cannot know that this will be the case. Until the end of the timeframe under examination, investors would not have even known that these statistical characteristics actually existed; i.e. they could only be calculated when the time period under examination had passed. For this reason statistical analysis of past data can give a false impression of the amount of information that investors possess when implementing an investment strategy and must therefore be utilised with care.

What Can an Investor Therefore Know?

Once the uncertainty associated with statistical information is factored in, it becomes clearer that when making investment decisions regarding an uncertain future investors have surprisingly few factors which can be assumed to hold. This arises as the derivation of a set of investment assumptions needs to be independent of the particular type of market environment and therefore should not require a general outlook for markets in order to hold. In other words, the assumptions set out must be highly likely to hold no matter what the market conditions. Generally, there are five basic tenets which is reasonable for investors to accept irrespective of market conditions.

1) The universe comprises a certain number of active fixed income managers at any point in time.

2) Active management has the potential, on average, to generate excess returns over the long term; i.e. there is the expectation that out of the universe of active managers that the average active manager, or a subset of active managers, will generate a material level of excess returns. While the validity of this assumption will vary from market to market, with respect to issuance weighted fixed income benchmarks, especially those in relatively small and concentrated markets, there are solid grounds for the view that they are inefficient from a risk/reward perspective. This provides scope for active management within fixed income portfolios to generate more efficient outcomes; i.e. the average manager to generate excess returns over the longer term.

3) Even though an active manager may generate excess returns over the longer term, it does not mean that they will generate excess returns over every sub period.

4) The level of excess returns generated by each active manager will be less than perfectly correlated over the longer term; i.e. there are diversification benefits.

Investors need to make a decision on the investment strategy followed with only an understanding, but no effective quantification, of the previously mentioned tenets to guide in structuring a portfolio.

What is the impact from combining managers?

With this knowledge, investors now set out to establish a strategy for hiring active fixed income managers. Let’s start by taking the two extreme outcomes.

1) The first situation is where investors simply choose to invest in a single manager. Investors may conduct background analysis to increase the odds of picking a winner but still face a material level of uncertainty associated with not only the ultimate level of excess return generated but also the path taken to get to the ultimate investment outcome.

2) Investors can go to the other extreme where they simply rebalance to ensure that they have invested an equal dollar amount in each of the managers within the universe. By doing this, they are guaranteed earning the average excess return from the universe of active managers. However, this structure in practice is often not feasible, considering (a) requires a significant level of asset base, (b) can be quite expensive to implement and (c) ignores the potential that the universe can change over time thereby inducing material transaction and transition costs.

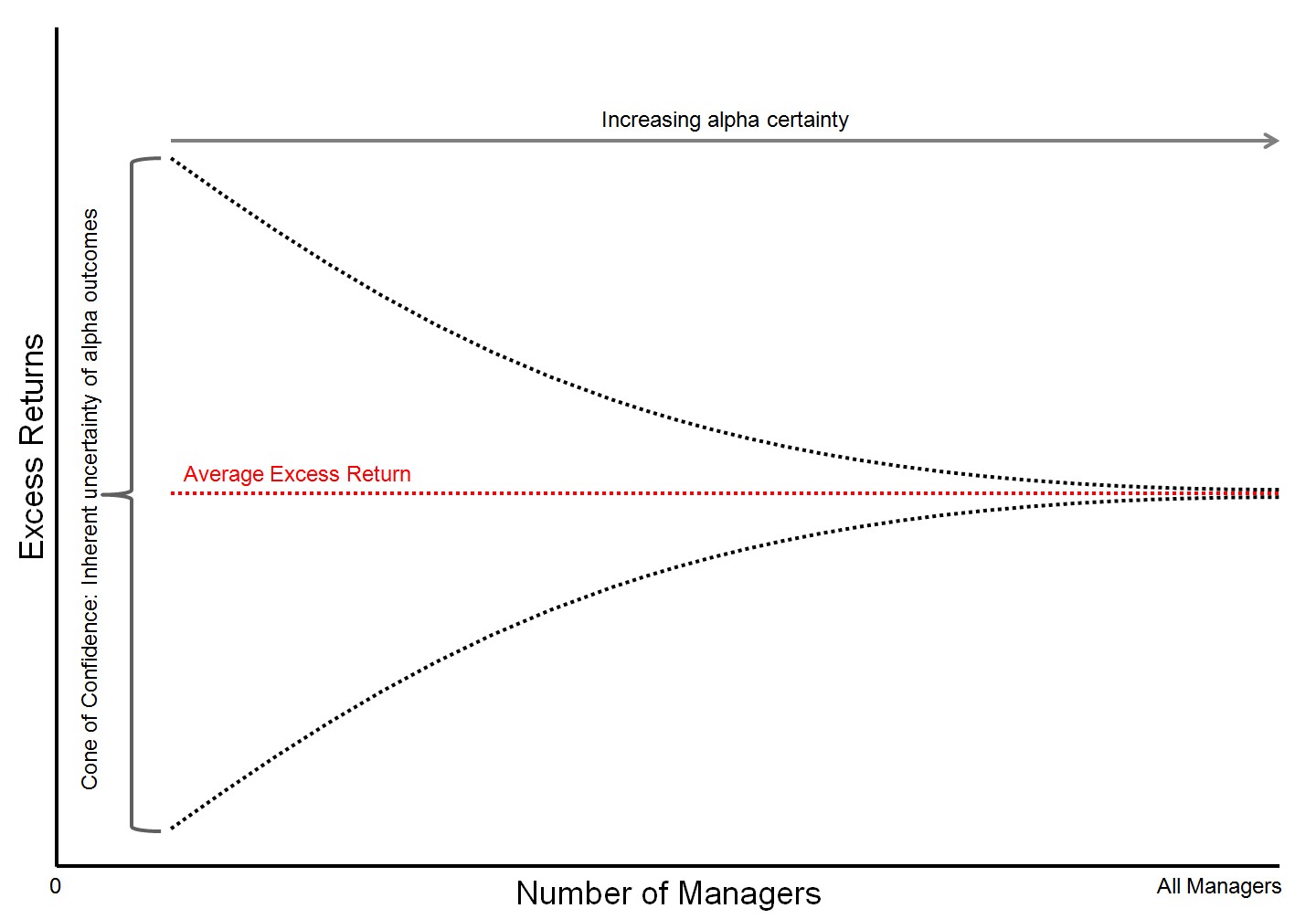

If investors were to plot the range of possible combinations and outcomes between these two extremes it is likely that we will get something like the stylised relationship illustrated in Figure 1.

Figure 1 :

Due to the correlation between managers being less than 1, as more managers are added together the dispersion of excess returns will decline. This continues until the point at which the investor holds equal amounts of all managers, where the dispersion from the average anticipated excess return becomes zero. In the stylised chart the ‘cone of confidence’ shows volatility of excess returns diminishing at a decreasing rate as more managers are added to the portfolio. What this illustrates is that naively adding more managers reduces the dispersion of excess return outcomes; i.e. moves the investor further along the ‘cone of confidence’. However just as important is the implication that the benefits from the reduction in the volatility of excess returns are derived at a decreasing rate as more and more managers are added to the portfolio; i.e. law of diminishing gains. Accordingly investors need to consider the optimal point of manager diversification beyond which the additional cost associated with adding additional managers to a portfolio may more than offset the gains from risk reduction. This stylised representation above highlights one of the key benefits associated with utilising a multi-manager framework in the fixed income space. It reduces the level of uncertainty associated with achieving a desired excess return target while not actually reducing the expected level of excess returns that the investor has access to. This is not to say that with the benefit of hindsight; i.e. knowing what market conditions actually transpired over a particular timeframe, the investor may not have been able to do better by either picking a single manager or not pursuing active management. This is simply based on hindsight whereas the investor needs to make decisions regarding the future in an environment of inherent uncertainty.

There has been much written regarding the pros and cons of multi-manager investing. Much of the analysis has focused on the impact of returns. Yet it is not simply the one dimensional, and often poorly defined, objective of maximising returns which is the focus of multi-manager investing within fixed income portfolios. Multi-manager investing goes further than this to also encompass the dual objective of risk management or managing the dispersion in return outcomes. Multi-manager investing aims to manage the dispersion of excess returns and by doing so maximise the probability that both shorter term and long term returns are maximised. Though this can be achieved by randomly combining managers a more methodical approach which looks at manager skill, style biases, market opportunities and benchmark inefficiencies can maximise the benefits to be derived from multi-manager investing within fixed income markets and thereby maximised the potential that the desired outcomes will be achieved.

Get investment insights from industry leaders

Liked this wire? Hit the follow button below to get notified every time I post a wire. Not a Livewire Member? Sign up for free today to get inside access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

1 topic

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment