TOL - 17th Nov, 2020

Why we're bullish on lithium

This quarter we wanted to focus on the significant medium-term opportunity around raw materials for Electric Vehicles (EVs), and particularly Lithium, where we have recently pivoted our stance on the commodity and increased the Ausbil Investment Management Global Resources Fund positioning significantly.

We believe the inflection point for EV acceptance is nearing, and there are a number of implications for natural resources markets driven by this theme. The main winners (in terms of commodity volume growth) from an increase in global rechargeable battery demand are likely to be Lithium, Nickel and Cobalt, and potentially Manganese.

At a high level in terms of commodity exposures, pure-play cobalt exposures are hard to find globally, and so we see limited opportunities to invest in this segment in size. Graphite remains challenged, as costs of synthetic Graphite remain low, cannibalising the market for natural Graphite. We are paying attention to this space as opportunities may present, but broadly we believe a recovery in Graphite is likely to take some time because of increased synthetic Graphite capacity in China, and low Synthetic Graphite feedback prices (pet coke prices are low, reducing synthetic Graphite prices).

The Nickel market is currently dominated by Stainless Steel demand. In time, the proportion of Nickel consumed in Batteries will increase, and we are focused on this metal on a longer-term basis, but short-term we believe the best opportunity to leverage the EV thematic is through Lithium exposure.

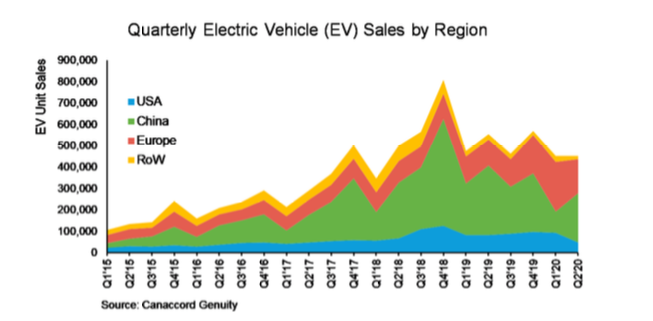

China no longer dominates EV demand

One important theme we have seen play out over the past 18-months has been an increase in EV demand from countries outside of China. China has dominated global EV demand since 2017, supported by domestic subsidies, but as we have seen the EV market mature, other jurisdictions have seen an increase in EV demand. In Europe particularly, local subsidies now have a number of EV models at the same, or lower price point to internal combustion models. Where historically buyers were required to pay a premium upfront for an EV, offset by lower running costs longer-term, subsidies and reduced manufacturing costs, and now upfront prices are similar relative to internal combustion models.

On a long term basis, we believe reduced manufacturing costs for EVs (particularly batteries), and higher compliance costs for internal combustion engine vehicles will see the economic benefits move further towards EVs. This, combined with higher quality vehicles being available to the mass market, will continue to drive EV demand within China and other markets.

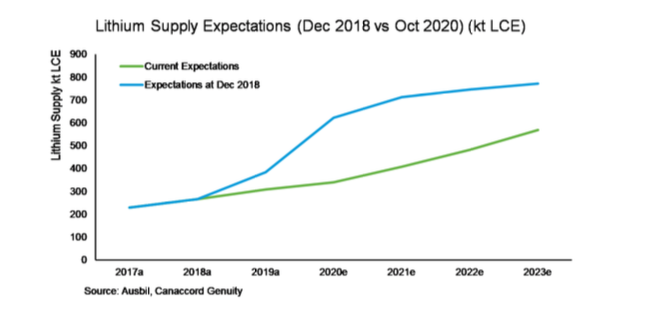

Supply has not eventuated in the Lithium market

Looking back at our own supply forecasts for Lithium from December 2018, production is well below where we expected. In part, this has been driven by supply curtailments as a result of weak pricing, but supply has not eventuated as we expected.

Lithium projects take time to fund, build, and commission. Even given the current excess production capacity in the market, we expect demand growth will absorb this excess capacity relatively quickly. With delays in new project construction, we could see a market reminiscent of 2017, where EV and battery makers scramble for product as the market tightens, driving commodity and equity markets higher.

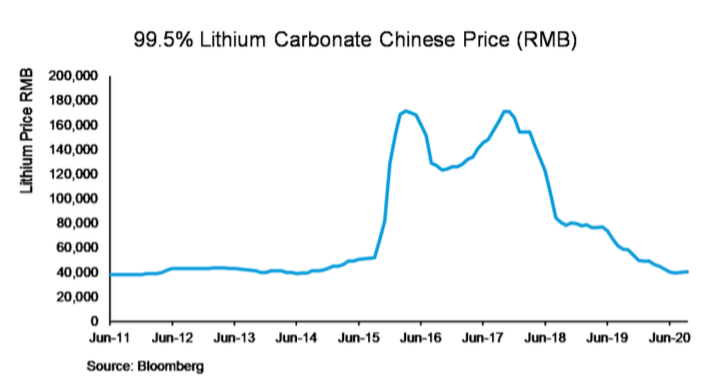

Lithium prices appear to have bottomed

True pricing for Lithium products is difficult to locate in real-time, however Chinese pricing for Lithium Carbonate is shown below. Anecdotally Lithium producers are suggesting pricing has increased slightly in recent weeks and months, and demand from customers has stabilised and is increasing. Ultimately, we believe an increase in the Lithium price will see a re-rate in Lithium equities, however, given the nature of the market we believe equities will likely rally well ahead of reported price increases in the commodity market. As such, we have positioned the Fund long in Lithium, leading into expected price increases in Q4 CY2020 and Q1 CY2021.

How Lithium is produced

Broadly speaking, there are three common resources used to produce Lithium, Brine Deposits, Hard Rock Deposits and Clay.

Brine Deposits. Mainly focussed in South America (Chile/Argentina), Brine Deposits have been a source of Lithium for many years, with brine pumped to the surface, and Lithium extracted via a chemical process. Historically, brine has been concentrated, then a precipitation process used to purify Lithium into Lithium Carbonate, but more recent technologies are advancing for direct extraction of Lithium from brine. Examples of companies producing Lithium from Brine include Orocobre, SQM and Albermale.

Hard Rock Deposits. Hard Rock (typically Spodumene) deposits are common in Australia. The mining and processing route is similar to traditional mining practices (drill, blast and mine) and processing (crush, grind and separate). Spodumene projects produce a concentrate product which then needs to be upgraded to Lithium Carbonate or Lithium Hydroxide through a conversion facility. Projects can be integrated (where a miner also converts at their own processing plant), or a Spodumene concentrate market exists, where producers sell Spodumene concentrate rather than purified Lithium carbonate and Hydroxide. Examples of companies producing Lithium from Hard Rock Deposits include Galaxy Resources and Pilbara Minerals.

Clay. Tesla recently attracted attention to the Lithium space with Elon Musk suggesting Tesla may be able to produce their own Lithium from Tesla owned Clay deposits in the US. We remain a little cautious on Clay deposits, as traditional processing routes require high capex, albeit Musk suggested Tesla may have an alternate processing route. Examples of other companies assessing Lithium from Clay include Ioneer and Lithium Americas, however there are currently no producing clay Lithium deposits of which we are aware.

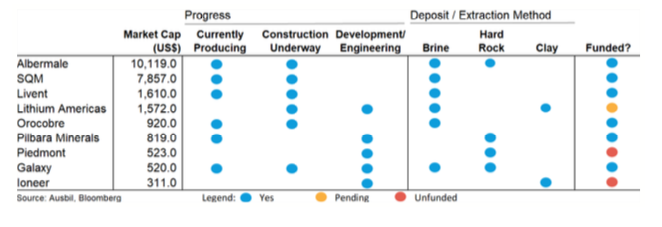

Our preferred plays in Lithium

Although there are a number of Lithium explorers globally, the list below shows our core focus list in the commodity. We believe there is currently a divergence in valuations between existing producers and developers, and the Fund currently holds positions in Galaxy Resources, Orocobre and Pilbara Minerals.

Invest in high quality natural resources companies

The Ausbil Global Resources team looks to capitalise on the volatility within the natural resources sector by employing a long/short approach to global natural resources equity markets with a focus on generating positive returns in both rising and falling commodity markets. Click 'FOLLOW' for more of our insights.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

James is the Portfolio Manager for the Ausbil Global Resources Fund and an Equities Analyst at Ausbil covering natural resources.

........

The information contained in this has been prepared for general use only and does not take into account your personal investment objectives, financial situation or particular needs. Ausbil is the issuer of the Ausbil Australian Active Equity Fund (ARSN 089 996 127), Ausbil Australian Geared Equity Fund (ARSN 124 196 407), Ausbil Australian Emerging Leaders Fund (ARSN 089 995 442), Ausbil MicroCap Fund (ARSN 130 664 872), Ausbil Australian SmallCap Fund (ARSN 630 022 909), Ausbil Balanced Fund (ARSN 089 996 949), Ausbil Active Dividend Income Fund (ARSN 621 670 120), Ausbil Australian Concentrated Fund (ARSN 622 627 696), Ausbil Active Sustainable Equity Fund (ARSN 623 141 784), Ausbil Global SmallCap Fund (ARSN 623 619 625), Candriam Sustainable Global Equity Fund (ARSN 111 733 898), Ausbil 130/30 Focus Fund (ARSN 124 196 621), Ausbil Global Essential Infrastructure Fund – Hedged ARSN 628 816 151), Ausbil Global Essential Infrastructure Fund – Unhedged (ARSN 628 816 151), Ausbil Global Resources Fund (ARSN 623 619 590) and MacKay Shields Multi Sector Bond Fund (ARSN 611 482 243) (collectively known as ‘the Funds’).

The information has given by Ausbil Investment Management Limited (ABN 2676316473) (AFSL 229722) (Ausbil) and has been prepared for informational and discussion purposes only and does not constitute an offer to sell or solicitation of an offer to purchase any security or financial product or service. Any such offer or solicitation shall be made only pursuant to an Australian Product Disclosure Statement or other offer document (collectively Offer Document) relating to an Ausbil financial product or service. A copy of the relevant Offer Document may be obtained by calling Ausbil on +612 9259 0200 or by visiting www.ausbil.com.au.

You should consider the Offer Documents in deciding whether to acquire, or continue to hold, any financial product. This information is for general use only and does not take into account your personal investment objectives, financial situation and particular needs. Ausbil strongly recommends that you consider the appropriateness of the information and obtain independent financial, legal and taxation advice before deciding whether to invest in an Ausbil financial product or service. The information provided by Ausbil has been done so in good faith and has been derived from sources believed to be accurate at the time of completion. While every care has been taken in preparing this information. Ausbil make no representation or warranty as to the accuracy or completeness of the information provided in this presentation, except as required by law, or takes any responsibility for any loss or damage suffered as a result or any omission, inadequacy or inaccuracy. Changes in circumstances after the date of publication may impact on the accuracy of the information. Ausbil accepts no responsibility for investment decisions or any other actions taken by any person on the basis of the information included. Past performance is not a reliable indicator of future performance. Ausbil does not guarantee the performance of any strategy or fund or the securities of any other entity, the repayment of capital or any particular rate of return. The performance of any strategy or fund depends on the performance of its underlying investments which can fall as well as rise and can result in both capital gains and losses.

3 topics

5 stocks mentioned

1 contributor mentioned

James is the Portfolio Manager for the Ausbil Global Resources Fund and an Equities Analyst at Ausbil covering natural resources.

Expertise

James is the Portfolio Manager for the Ausbil Global Resources Fund and an Equities Analyst at Ausbil covering natural resources.

Expertise

Comments

Comments

Sign In or Join Free to comment