Will the US outpeform international markets over the next decade?

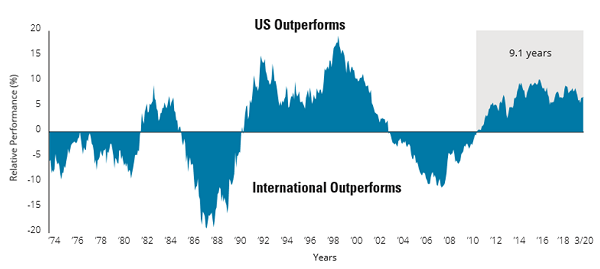

The Perpetual Global share fund was established in January 2011. I took the view that global markets offered much more exciting and rewarding opportunities than the Australian market and with the Australian dollar at parity, it was time to shift exposures to the US and abroad. Those investors that have been with the fund from the beginning have been handsomely rewarded. Now I believe that it is time to shift out of the US into other global markets. The fortunate thing about being a global investor is that you don’t need to invest in an expensive market, you can just move to better opportunities elsewhere. Over time there are periods when the US market outperforms, and other periods when international markets outside of the US outperform. We have been through a 9-year period where US markets and the US dollar has outperformed.

Chart 1 - US Market vs. other international markets

Source: Morningstar data

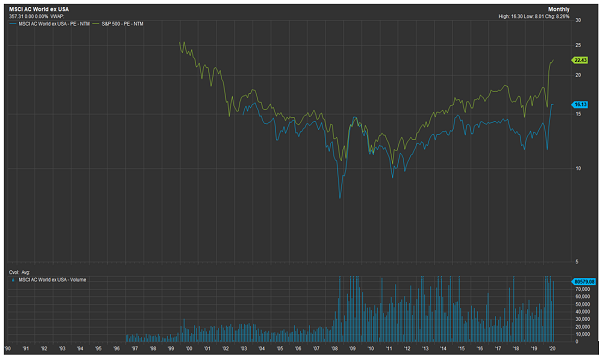

A lot of this is due to multiples expanding in the US. In the chart below you can see that from 2002 to 2012, the price paid for a dollar of earnings was similar in international markets compared to the US. However, this year there has been a huge spike up in the difference between the two. While the S&P 500 index is currently trading on a PE of 20x 2021 guesstimates, the MSCI world index ex US is trading on a much more palatable 15x earnings.

Chart 2 - MSCI World Index vs. S&P500 Index

Source: FactSet

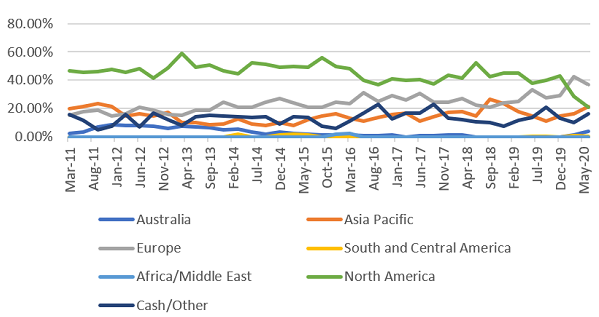

Given the current global recession, expanding US valuations, the unpredictability of earnings streams due to a rampant COVID-19 pandemic, which the US has been unable to control, I have decided to significantly reduce the US exposure in the portfolio. The impending US election is also a risk to earnings of US companies, if Joe Biden is successful, as he has been vocal about unwinding some of Trump’s corporate tax cuts and increasing the corporate tax rate back up to 28%. As can be seen in the chart below, our exposure to US domiciled companies has recently reduced to closer to 20%.

Chart 3 - Rolling Regional Exposure

Source: Perpetual Investments

GREAT BUSINESSES AT GREAT PRICES IN INTERNATIONAL MARKETS AT THE MOMENT

Over the past six months, we have taken the opportunity to accumulate a number of attractive businesses in Europe and Asia. The majority of the businesses we have acquired in Europe are multinational companies, while in Asia we have had more of a tilt towards national champions.

In Europe we added to Vivendi, the owner of Universal Music Group (UMG). UMG is global leader in recorded music, music publishing and audio-visual content in more than 60 countries. The business is growing at double digit rates, driven by the growth of music streaming helped by the growth of digital distribution platforms such as Spotify. Under the leadership of Yannick Bollore, Vivendi has expanded over the years and most recently has sold a small stake in UMG to Tencent. We expect the true value of UMG to be realised by the market over the next few years and are patient and happy holders of the business.

The German market has always been a rich market filled with quality companies. We currently have about 10% of the portfolio allocated to German companies which are all multinational companies. Healthcare companies like Merck KGaA, a leader in life sciences and pharmaceuticals, and Fresenius Medical care, a leader in dialysis in the US and Europe, have found a happy place in our portfolio. We have also bought into RWE, a large power generator and wind farm operator, during the March sell off. We also added to our Siemens position as the group continues to move forward in simplifying the business and highlight the strength of their healthcare and digital automation businesses.

In Asia, we added to our technology positions in national champions. We have held Alibaba for quite a number of years now, initially through our position in Yahoo, when the company was not listed. We then bought directly into the company during its IPO in 2014 and have recently added to the position. Alibaba will continue to benefit from the rapid growth in ecommerce in China, which this pandemic is accelerating. We also believe that its leadership in the cloud and payments, through its stake in Alipay, are not being fairly valued by the market. We have also added to our position in Baidu, which is the leading search engine in China, but also has a number of other hidden assets. They are the largest shareholder in Iqiyi, one of China’s leading internet video streaming services, and Trip.com, China’s leading online travel portal. They are also a leader in artificial intelligence and have a well-developed autonomous driving car platform, Apollo. I’m amazed at how much the market is paying for Tesla, while attributing negative value to Apollo.

Japan is also a market filled with quality multinational companies. We have taken the opportunity to add to our Japanese positions recently. Despite the media’s love affair with highlighting the travails of a small position in Masa Son’s collection of assets, the company has performed well for us since Elliott has taken a position and urged Masa to take some profits on some of their larger positions and buy back stock to narrow the discount between the value of their assets and the price ascribed by the stock market. Their stakes in Alibaba, ARM and Softbank telecommunications corp underpin the value of the conglomerate and these businesses continue to perform very well.

We have recently bought into Optorun, which is a leading manufacturer of vacuum coating machines and products for smartphone manufacturers such as Apple. We believe the company will benefit from the growing demand for filter, lens, display and mini-LED coating applications.

We have also bought back a position in Asahi, which continues to grow into a brewing and drinks powerhouse globally. The pandemic has led to falling stock prices for these businesses as the shut down of bars and on trade premises will lead to a decline in earnings this year. However, we believe this is a unique opportunity to buy a portfolio of quality brands at a large discount to fair value. Asahi has recently settled on the acquisition of Australia’s Carlton United Breweries, which was the crown jewel in Australia’s Foster’s group (pardon the pun). We expect Asahi to extract significant cost synergies as it integrates this business with their soft drinks assets (schwepps and other brands) in Australasia. The Japanese market has been blindsided by the pandemic, but we believe that the value of the group will be realised over the next few years as the world slowly returns to a new normal and the group extracts these synergies.

WHAT IS DRIVING US MARKETS HIGHER?

1. Monetary and Fiscal stimulus

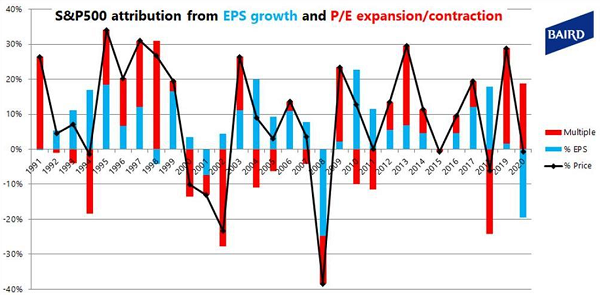

The government stimulus measures in the US have been astounding. As Jamie Dimon put it at a conference, “the fed didn’t bring a bazooka, they brought the whole army”. The federal reserve has expanded its balance sheet by 3 trillion dollars, buying listed and unlisted bonds. This has injected a significant amount of liquidity into financial markets. It has also created this unusual scenario where we have seen the S&P 500 multiple expand during a period of significant earnings downgrades. As can be seen in the chart below, the last two times the markets fell due to recessions (2001 and 2008), the multiple of the market actually went down, not up.

Chart 4

Source: Baird Research

The other area of stimulus has come from governments increasing their fiscal expenditure to support the unemployed. Job keeper and seeker payments are prevalent around the world which has led to a surge in government debt.

In the US, lawmakers have passed three emergency aid packages totalling nearly $3 trillion. The 2 trillion initial stimulus spend, adding $600 per week to unemployment benefits is set to end in July. This will need to be extended to support consumption, otherwise the impacts on the economy will be deeper than what we are currently experiencing. U.S. debt is on track to surpass the size of the nation's economy for the first time since World War II and the US budget deficit for 2020 will top $3.8 trillion, more than double the record set during the 2008 financial crisis. The problem with ballooning government debt is that at some point it will need to get paid back and that’s why Biden wants to increase the corporate tax rate to 28%.

2. Retail euphoria

As a global investor, we are always hunting for high quality businesses that are mispriced by the markets. Equity markets go up and down based on money flowing into and out of them over periods of time. Sometimes there is no rational pricing of assets occurring as central banks either pump liquidity into assets or investors keep buying the same companies because they keep going up. Eventually logic prevails and capital is allocated rationally again but it can take many years. I was just reading that Elon Musk is now the 7th richest person in the world, with his 18% stake in Tesla comprising the bulk of his $70 billion dollar fortune. Tesla is now being valued at $286 billion dollars, which implies a price to earnings ratio of 360x. Its global peers, like BMW, Volkswagen, GM, Toyota, trade on multiples of 6-10x. Many of these globally leading auto manufacturers are arguably just as advanced as Tesla is on the ability to produce electric vehicles or autonomous driving cars. However, the market knows that these businesses are highly capital intensive. Tesla on the other hand is a good example of how a number of US companies with a great marketing pitch are soaring to incredible valuations as euphoria takes over. Even its founder is laughing on twitter about “stonks” and how he thinks the Tesla stock price is too high. Those tweets were a few months ago when the stock price was around $800. That hasn’t stopped the retail train from continuing to pile in with its price doubling again as it seems to be going up 10% a day. On Monday 13th of July, almost 40,000 Robinhood accounts added shares of Tesla during a single four-hour span. The stock was up 14% at one point in that day and then closed down 3%. Looks like it will be a wild ride!

While many of the US’s greatest investors are sitting back on a pile of cash analysing weaker economic data (Warren Buffett, Stanley Druckenmiller, Jeremy Grantham), the US market continues to grind higher. We haven’t seen valuations this high since the peak of euphoria in 2000 and it took over a decade for the market to move higher from those levels.

Citadel Securities, the market-maker which handles more than a fifth of US equity trading and 40% of equity retail trades, says retail traders now account for 20-25% of stock market trading, up from its historical 10% range. The US market is not alone in seeing these bouts of retail market euphoria. In the late 1980s, the Taiwan stock exchange index had a powerful rally driven by retail investors. At the time there were more stock brokerage firms than stocks in the index and everyone from janitors to dancehall hostesses were trading stocks. It only took the index thirty years to get back to the same levels again. I’m not saying the US stock market is at those types of levels, but it's time to remember the old adage that when your taxi driver (or in these days uber driver) is giving you stock tips, it's time to question the market’s exuberance. I really enjoyed Jeremy Grantham’s recent quote, “the chutzpah involved in having a bubble at a time of massive economic and financial uncertainty is substantial”.

The interesting thing about this market is that there is a large bifurcation between the valuations of traditional companies and the ones that are expected to take over the world. So, we are still finding some very interesting opportunities in the US market today. We have been buying back some old favourites like Fox Corporation and CME Group, which have been caught up in the recent sell off. We have also added to our healthcare positions, adding CVS Health, which is a leader in pharmacy services and healthcare benefits.

While markets can move quickly in both directions in the short run, we like to take a longer-term view to investing with a focus on continuing to generate attractive absolute returns for our clients, while minimising the levels of risk. COVID-19 is a pandemic which is unpredictable and the duration of its impact on society and the economy is unknown. It has driven governments and central banks to take unprecedented steps of lowering interest rates and handing out money. Fiscal stimulus has been necessary to support those in need but I question the benefits of the distortions that central banks have created. I'm happy with the quality of the businesses we own and the upside in the portfolio, whilst looking to mitigate the impact of weakening global economies by being most exposed to resilient industries like technology, consumer staples, healthcare and stock exchanges.

I hope you all stay safe and healthy over this new financial year.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments.

Profeta Investments is a global asset management firm focused on delivering high absolute returns. We focus on investing in quality businesses through different phases of their maturity. We manage a high conviction portfolio taking a long term view. We focus on growing companies with strong balance sheets where management teams are aligned with shareholders. For more information visit www.profetainvest.com

1 topic

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments. Profeta Investments is a global asset management firm...

Expertise

Garry is an experienced global investor, managing global equities portfolios at Profeta Investments and Perpetual Investments for over twenty years. He is the founder of Profeta Investments. Profeta Investments is a global asset management firm...

Expertise

Comments

Comments

Sign In or Join Free to comment