Share prices and reality: 2 high quality oversold businesses

With the advent of the 24-hour news cycle, live pricing feeds and an endless stream of news and stock market analysis, a widely held view is markets become more efficient as more information becomes freely available. Here we argue this is not always the case, and look at two growth companies that are now offering compelling value as the result of a gross market inefficiency.

Where professional investors were once able to exploit an information advantage by virtue of simply having better access to markets and/or the timely dissemination of company news announcements, market data and stock analysis is now freely available to almost every individual, neatly reported on a minute by minute basis, indexed by stock code and delivered direct to one’s smartphone.

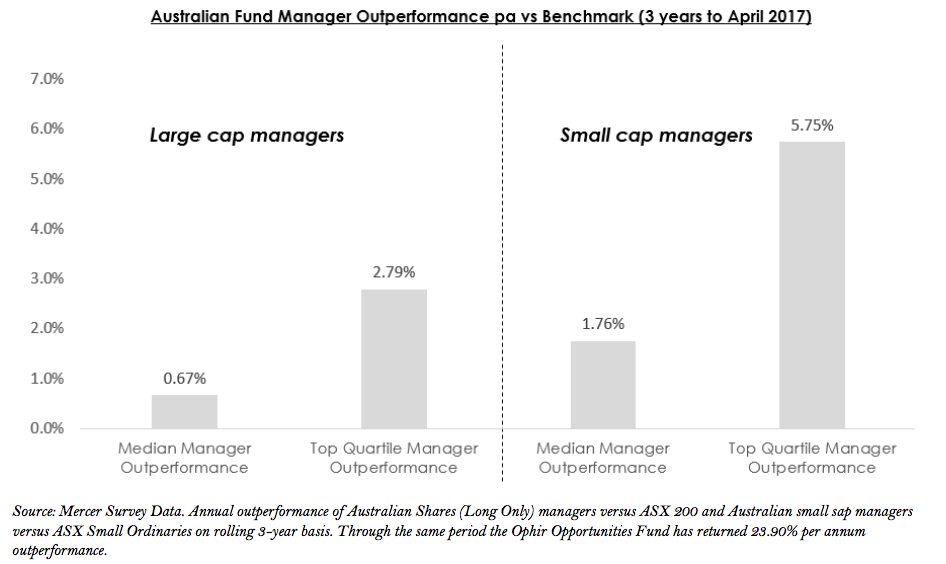

Is this tidal wave of information and data creating less opportunities for professional investment managers? Market theorists would suggest that with greater information comes greater efficiency and therefore less opportunities for alpha. Certainly the competitive advantage held by professional managers in the larger cap end of the market appears to have been eroded away somewhat in recent years. This no doubt has subsequently opened the door for the now monolithic rise in passive low-cost ETF products.

Small cap managers have been insulated somewhat from the phenomena, primarily as a function of the far wider opportunity set and lower media and sell-side analyst coverage. While the number of small cap managers has increased in recent years, there still remains ample opportunity for professional managers to uncover attractive businesses within the space through their own proprietary in-house research. That being said, the level of publicly available information and analysis on the smaller cap space has noticeably increased, although the quality of that information typically is less consistent.

What is interesting is that this seemingly endless flow of information and analysis may actually be creating new inefficiencies for investment managers to exploit by virtue of generating the equivalent of investor group think. Enormous amounts of capital today are moved around the world on a daily basis in response to the latest macro data point or news item release, only to then be rotated to another corner of the market following some other widely anticipated event. The growth in ETF index-tracking products has only served to allow this capital to not only move quicker, but also to gravitate toward larger companies that make up the biggest proponent of an underlying index.

To borrow from Ben Graham’s observation “share prices in the short term are voting mechanisms and in the long term weighing mechanisms”, capital markets today may actually be creating more opportunities for bottom-up, benchmark-unaware investors that are able to sift through the noise of the market and deploy capital into specific underlying businesses rather than some overarching index.

Whilst highly simplistic in nature, investors can often forget that behind every index or stock code there exists actual companies operating within the real world. While markets may on a second- by-second basis dictate what the equity of this company is worth, often there are opportunities where news events and the rotation of capital can price this equity at levels not accurately reflective of the company’s underlying operating performance. These are fantastic opportunities for managers that have spent time meeting with the companies and understanding the key earnings drivers to deploy capital at a time when the broader market is pricing the equity cheaply.

A recent example front of mind for small cap managers will have been the sell-off experienced in a number of the higher-quality growth businesses through the second half of 2016. As markets embraced the prospect of global reflation, an unprecedented amount of capital rotated away from small cap growth businesses in favour of cyclical, banking and resources companies on the view a return to global growth was imminent.

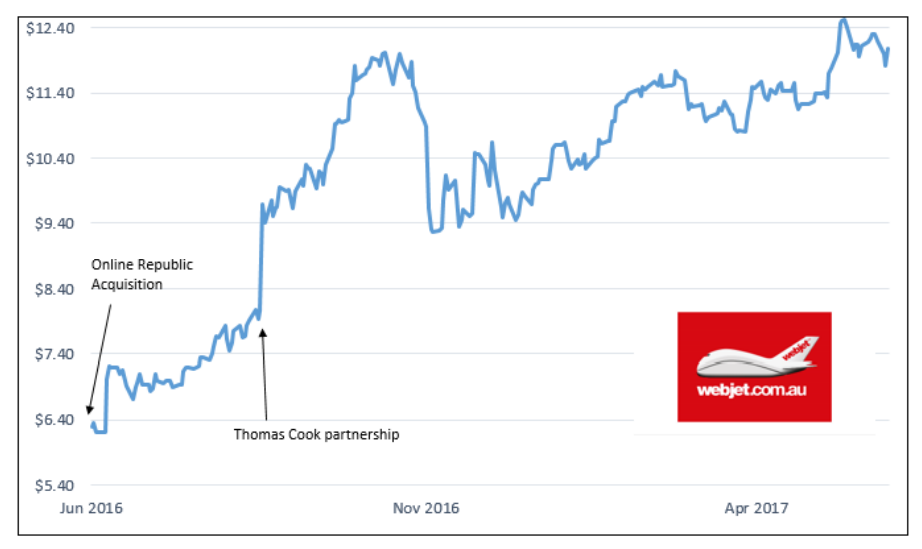

As a consequence, a good number of excellent companies in the space saw the price of their equity decline at a time when the businesses themselves were continuing to deliver from an operational standpoint. A number of these businesses have subsequently served to recover well from the sell-off, and for those investors that took advantage of the opportunity at the time, the rewards have been compelling. Two recent examples that come to mind in our own portfolios were travel business Webjet (WEB) and data centre provider NextDC (NXT).

Webjet (WEB)

The continued growth of Webjet’s core flight bookings business has been a surprise for many, given the booking fee model has come under pressure in other areas of the global travel industry in recent years. The growth in international flight bookings and the ability to provide additional services (car hire, travel insurance, accommodation packages) saw the core business comfortably exceed market growth rates and allowed the company to grow and diversify into new wholesale B2B travel opportunities

The company accelerated these plans in June 2016 with the $79m acquisition of global e-commerce group Online Republic, a market leader in online motorhome rentals, car hire and cruise packages. This was followed shortly after by an announced strategic partnership with global tour operator Thomas Cook in August 2016, a deal expected to be significantly earnings accretive in future years and meaningfully accelerating the wholesale hotel booking business into growth markets in Europe. As a result, the market subsequently re-rated the business on expectations of continued future growth in the core Australian business and significant growth optionality globally.

Despite the initial enthusiasm, the company share price instead came under pressure through the beginnings of the growth sell-off in October. While industry feedback indicated continuing strong growth in international travel numbers and management remained upbeat on the progress of recent acquisitions, the share price of the business instead retreated some -22% from its October highs. Comfortable that the underlying business continued to be operating well, we initiated a positon in the company in November and have been pleased with the continuing progress.

Under the guidance of CEO John Guscic, the business has subsequently exited the underperforming Zuji business (netting $56m for further growth opportunities) and upgraded their earnings guidance at the recent February result. Importantly, growth has continued to accelerate through the year as the company enjoys tailwinds from decreased pressure on airline ticket pricing and the continued structural move toward online travel. From the lows in November, the share price has since recovered +34%.

NextDC (NXT)

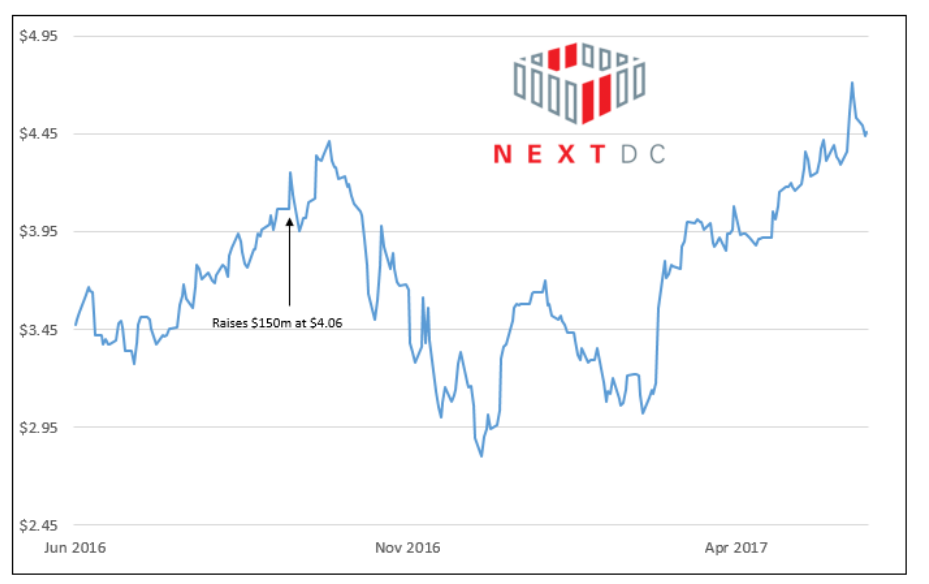

Data centre provider NextDC was essentially hit with two sides of the rotation trade stick. A highgrowth / high multiple business in its own right, the company raised $150m in fresh capital in September 2016 to fund the construction of a new Sydney data centre to meet growing demand for cloud services.

The business has seen exceptional growth for its data centre services in recent years as businesses make the structural transition toward hosting their IT networks in the cloud. This requires businesses to purchase space (so-called “racks”) in physical data centre locations, to which they pay the data centre provider an ongoing monthly subscription. This trend toward co-location of data has been the driving force in NXT’s growth, the business reporting FY16 earnings before interest, tax, depreciation and amortisation (EBITDA) more than 3x the number produced in FY15.

At the time of the raising, the company had issued guidance for FY17 EBITDA in the range of $46- 50m, which in itself almost doubled the earnings delivered in FY16. The equity issuance was unsurprisingly swamped in demand, with the share price momentarily responding well to the new growth initiatives.

As has been the case with a number of growth businesses that raised fresh equity through 2016, NXT was hit particularly hard as the rotation period took hold. Capital raisings had provided liquidity events for more ‘non-natural’ holders of small cap growth stocks to acquire a large parcel of shares and these companies were subsequently the first to be sold through the rotation back to large caps. Despite the market clamouring to write a cheque for fresh equity at $4.06 in September, the share price instead slumped to $2.80 only two months later.

It would be difficult to think the underlying structural move towards cloud adoption had significantly changed in such a short time. As a business that owns large, physical infrastructure-type assets one could argue that the move in global bond yields may have had some impact on the way analysts discounted future cash flows, though it seemed a stretch. An unlisted competitor making some noise around aggressively taking on the business from a pricing point of view may have contributed to some shorter term concerns, however the quantum of the sell-off still seemed largely overdone.

Like Webjet, operationally the business continued to perform well despite the listed equity of the business suggesting otherwise. Unsurprisingly, growth in data centre uptake has continued, with the company maintaining their EBITDA guidance for FY17 and further growth expected out of new data centres currently on track for completion in the next 6 months. Our own anecdotal feedback from discussions with competitors and listed IT service businesses would indicate the demand profile for data centre storage continues to strengthen and it has been pleasing to see the market again recognise the growth runway ahead.

--

This is an extract from Ophir's monthly letter to investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

2 stocks mentioned

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Andrew has over 15 years’ experience in portfolio management of listed companies, stockbroking and economic analysis. Prior to co-founding Ophir, Andrew worked from 2007 to 2011 as a portfolio manager at Paradice Investment Management.

Expertise

Comments

Comments

Sign In or Join Free to comment