3 ways to invest in gold

Rob Holder

LGT Crestone

Gold has a long association with finance and investing—from its use as a form of early currency to gold standard-based currencies from the late 1800s. More recently, it has played a role in complementing other portfolio holdings.

Current attitudes to investing in gold are varied—some hold a great deal of the precious metal in their portfolio, but most hold none. Recently, investors have been drawn by strong returns, and questions have been raised as to what an appropriate holding looks like within a diversified portfolio.

What role can gold play in a portfolio?

Gold has traditionally been used as a portfolio hedge, rising in response to higher inflation, to a declining US dollar and to sharp reversals in riskier assets. This negative correlation is attractive from a diversification standpoint, helping to dampen overall portfolio volatility. Gold also has a limited supply and various demand sources—from jewellery production to industrial applications and as an investment. Despite these positive characteristics, gold has its critics, most notably Warren Buffet, who decried gold’s lack of return drivers. Gold does not produce anything and has costs associated with its storage. Gold has also experienced extreme price volatility and prolonged periods of negative returns, making expected future returns difficult to forecast.

What is a reasonable return expectation for gold?

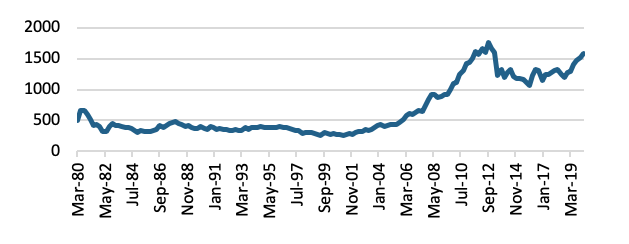

Gold differs from most other investments as it is a real asset which does not have an internal rate of return. So, we are forced to look to history as a guide to potential future returns. This is problematic as the price of gold has been particularly volatile through time, and the overall return varies greatly depending on the time period selected.

Return assumptions vary from zero nominal return (as the internal rate of return is zero) to 9% real return (if you take the price gain since the year 2000). The former seems too conservative, given gold’s inverse relationship with inflation, and the latter too optimistic, given prolonged periods of zero growth in gold’s price history. We believe a reasonable return expectation for gold sits in the region of 0% to 2% real return, which is broadly in line with the long-term return over the 20th century.

The price of gold has been particularly volatile through time

Source: Bloomberg. Data as at April 2020.

What’s the optimum asset allocation?

Given the challenges associated with establishing reliable forecasts for risk, return and correlation, there are also issues in determining an appropriate weight for gold within portfolio strategic asset allocations (SAA). As a result, it is important to temper any findings from mean-variance type analysis. Research by JPMorgan in 2012 found that including gold in portfolios will improve the risk and return outcomes when compared to traditional equity/fixed income dominated portfolios. A portfolio with an allocation to gold could expect a real return of 2% and volatility of 14%. Our own analysis suggests a benefit for including gold—particularly for investors with balanced and growth risk profiles where the diversification benefits are greatest due to larger equity weightings elsewhere in the portfolio.

We prefer to place a recommended weight range

As with all asset classes, the optimum portfolio weight varies considerably depending on forward-looking expectations. However, as noted earlier, this is particularly challenging for gold, so we prefer to place a recommended weight range rather than an outright weight. An allocation to gold sits within the alternatives asset class, and more specifically as a component of the real assets sub-asset class.

Our findings suggest a strategic weight of between 0% to 3% is appropriate for investors with either a balanced or growth risk profile. For most investors, this suggests that gold should be a relatively small ongoing SAA position—or a tactical position implemented when market conditions are supportive of holding gold.

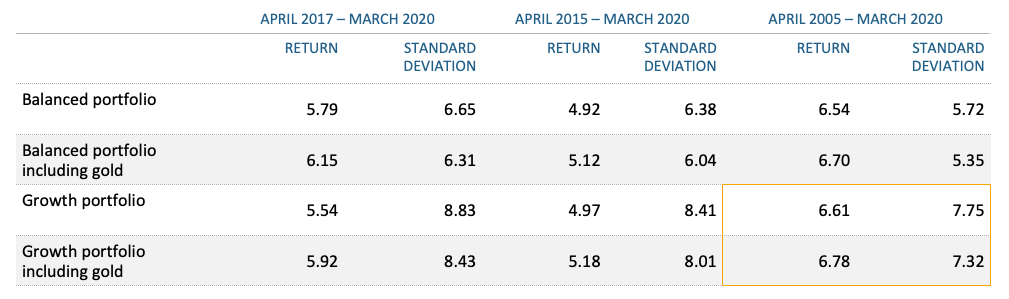

If we test this weight on a historical basis, we can see that a 3% allocation (at the expense of equities) would have improved portfolio risk across a wide range of time periods, with the added benefit of boosting return across longer periods. For example, over the last 15 years, adding a 3% SAA weight to our current growth SAA would have improved the return from 6.61% p.a. to 6.78% p.a. while reducing the volatility from 7.75% p.a. to 7.32% p.a.

Adding gold can improve the risk-return profile of a portfolio

Source: Crestone.

For those investors not comfortable including gold as a strategic holding, there may be some merit in using it as a tactical play. As mentioned earlier, gold has historically delivered a negative correlation to rising inflation and to a falling US dollar, therefore delivering a portfolio hedge for investors fearing those conditions. Additionally, gold tends to increase in value when financial system stability comes into question or when other major shocks impact riskier assets.

What is the best way to implement gold?

For those wishing to invest in gold, the method of implementation is a key consideration. Holding the asset physically, via an exchange-traded fund (ETF) or investing in listed gold mining companies are the three obvious choices, and there are advantages and disadvantages to each.

Physical—The purest form of gold ownership is simply to purchase gold bullion, however there are a number of complications which impact this option. The largest consideration is that the gold must be stored, and this comes with a cost. There are also question marks over security and whether the gold is segregated or commingled with other owners’ holdings.

ETFs—A more straightforward option than physical ownership is to purchase an ETF. This is fairly intuitive for most investors who would typically already buy and sell equities in the same way. Synthetic offerings use derivatives to replicate gold price movements, whereas physically-backed products actually hold the gold to back the investment. Both options come with costs, but the risk of price movements deviating from the gold price and of counterparty default make synthetic options less attractive than physically-backed ETFs.

Gold miners—Another common way to gain gold exposure is to invest in the listed equities of gold mining companies. The fortunes of these stocks are obviously heavily reliant on the price of gold, but additional factors are at play, making this type of exposure much more complicated. One notable downside is that, while the price of gold and the performance of gold miners tend to be highly correlated over the long term, there can be short-term divergence—for example, during a stock market crash when sentiment drives the whole market lower. This may reduce the diversification benefits for those holding mining stocks instead of physical gold (either directly or via an ETF). Individual mining companies are also subject to operational considerations, which could have a material impact on stock price, regardless of the price of gold.

In summary

The merits of holding gold in diversified portfolios have been debated for many years but traditional analysis is difficult to apply as there are challenges estimating gold’s expected risk and return. We find that a strategic holding of between 0% to 3% allocated to the real assets’ component of the alternatives asset class is appropriate for investors with balanced or growth risk profiles. Investors not including gold in their SAAs may wish to consider gold as a tactical play when favourable market conditions are expected. The question of implementation is not without complication either, but we believe that physically-backed ETFs deliver the best combination of secure and efficient exposure to gold price movements.

Learn what Crestone can do for your portfolio

With access to an unrivalled network of strategic partners and specialist investment managers, Crestone Wealth Management offer one of the most comprehensive and global product and service offerings in Australian wealth management. Click 'contact' below to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Rob is an Asset Allocation Specialist with experience across a wide range of asset classes (Equities, Fixed Income, FX) and investment functions (portfolio management, implementation, analytics and asset allocation).

Featuring

Rob Holder,

LGT Crestone

Rob is an Asset Allocation Specialist with experience across a wide range of asset classes (Equities, Fixed Income, FX) and investment functions (portfolio management, implementation, analytics and asset allocation).

4 topics

1 contributor mentioned

Rob Holder

Asset Allocation Specialist

LGT Crestone

Rob is an Asset Allocation Specialist with experience across a wide range of asset classes (Equities, Fixed Income, FX) and investment functions (portfolio management, implementation, analytics and asset allocation).

Comments

Comments

Sign In or Join Free to comment