Making money through the cycle

The recent equity market rally in response to dovish FED language again highlights how dependent equity markets are on government stimulus and sugar hits.

Unfortunately, commonly used approaches to building portfolios rely heavily on equity markets and other mainstream asset classes rising to make returns at a time when longer term prospects for traditional portfolios appear glum. The problem is that super-stimulatory monetary policies over many years have pulled forward returns in these markets, flattering the past effectiveness and returns of long only strategies which depend upon them. This has made future returns less prospective and mainstream asset classes highly susceptible to turning down simultaneously in a meaningful way. In fact, traditional assets could easily disappoint together in coming years, for example if interest rates rise or governments default under their excessive debt burdens in the next economic downturn. Longer term proactive investors need to take serious account of these substantive risks and in many cases change what they are relying upon.

Most investors genuinely require portfolios to produce positive returns reliably over time, and not be a simple binary or short term bet on monetary and fiscal policies - such as whether the FED can keep monetary policy stimulatory or not. In order to achieve this objective, investors now need genuine diversification and highly skilled active management more than ever. While allocations of around 20% to alternatives are commonly used in multi-asset multi-manager portfolios and can be somewhat helpful, much greater allocations are often required in portfolios which are genuinely outcome orientated and return seeking, and which want to be more resilient to large traditional market downturns when they eventuate.

Most advisers also very much desire and need their portfolios to have less risk of very large drawdowns. Greed is only good in bull markets! Furthermore, client orientated advisers also understand that their clients also want to avoid very large drawdowns and in fact will often not be able to withstand them when they occur. The quandary is that while investors need meaningful and positive absolute returns, they are not thrilled at the prospect of very large double-digit losses across their entire portfolios when the sugar hits stop. Hence, there are both market and client related reasons for why investors should consider portfolio construction and their portfolio approach critical in reducing the risk of large losses.

With strong market and client reasons, it is hence no surprise that genuinely outcome orientated investors (such as ourselves) support larger allocations to alternative managers and lower allocations to long only traditional investments in portfolios.

The most useful alternatives in a portfolio need to avoid relying upon traditional equity and bond markets rising to make returns. The return of alternative managers should ideally be uncorrelated to traditional markets, relying instead on genuinely alternative and differentiated strategies. The best alternatives tend to be “niche” in nature, performance orientated, and are quite often not broadly used or easily available. They are not a “me too” investment found in your average default “low (direct) cost” institutional investment product. Unfortunately, low direct costs can easily equate to high indirect costs over time.

The reality is, however, that it is not easy to identify compelling alternative managers. Many of them disappoint over time, often for predictable reasons. As with all active strategies, good alternative managers are hard to find and investors shouldn’t expect them to be readily available, but obviously should consider their suitability carefully when they are – particularly given the scarcity of and value of their offerings as part of a broader portfolio.

So how can investors improve their chances of choosing the right alternatives for their portfolio? What should investors look for when choosing an alternative fund? We list four considerations below.

(1) Low market correlation and sensitivity for genuine diversification

A market neutral fund does what its name suggests. It avoids significant sensitivity to market movements or reliance on markets going up to make a return, making it an extremely useful component in a broader portfolio. In other words, its uncorrelated to market movements i.e. its returns are independent of whether the market goes up or down.

Investors can see some evidence of this by looking at the historic correlation and beta of the fund – given a sufficiently long history – to that of equity markets. Investors should also gain an understanding of where the return comes from, and assess the likely correlation of the fund manager’s returns with other managers.

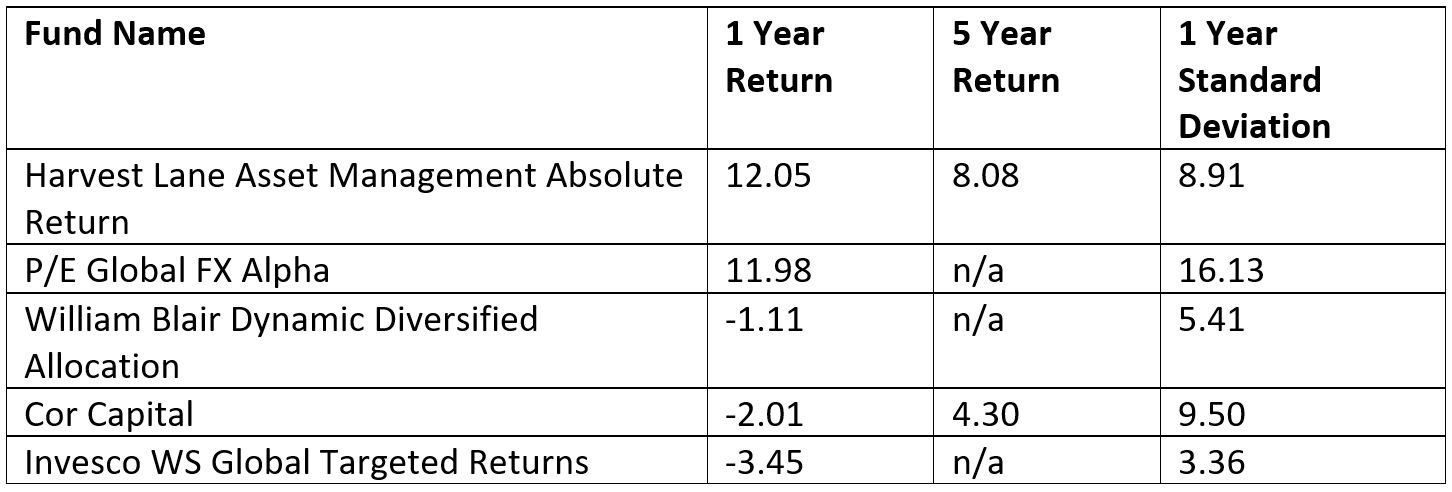

For example, the high ranking “market neutral” Harvest Lane Absolute Return fund (see table below) has demonstrated that it has no correlation or beta to the equity market over its more than 5 year history in a liquid daily priced offering. This is unsurprising given its strategy depends primarily on the idiosyncratic risk from low risk M&A transactions, and equity market risks are actively hedged as necessary.

In contrast, some alternatives (e.g. unlisted property, infrastructure and equity) invest long in property, equity and credit markets, but rely on “stale” pricing to deliver the appearance of a low correlation. If equity or property markets turn down, their prices should and will eventually reflect this – just in a lagged fashion. In other words, their diversification qualities are somewhat spurious. That is not to say they may not make good investments, simply that they are not as useful in a portfolio seeking to mitigate large downside risks and provide genuine diversification from long only strategies dominant elsewhere in the portfolio. They will and can be challenged by any collapse in pricing in the “bubble in everything”. Interestingly and as an aside for investors of these funds, leveraged unlisted property, infrastructure and equity investments are frequently used by large super funds to lower the apparent risks and volatilities of their funds. Good market neutral funds tend to have more limited capacity meaning they’re effectively inaccessible for large institutional investors, a paradox given these investors tend to be most understanding of their value!

(2) Genuine return potential and history of performance

The reality is it is not easy to make money for investors when you take out the free (historical?) kick of market returns. Many if not most alternatives have found it very challenging to do so in recent years, struggling with intense competition in most markets and massive amounts of reactionary government intervention in markets distorting capital allocation and pricing signals. We can’t see this changing any time soon! Investors hence need to choose carefully and look for a good investment approach that makes sense to them and which they can back over time through the inevitable ups and downs and as part of a broader portfolio, as is the case with all active strategies.

Top SQM Rated Funds Ranked by 1 Year Return

Source: SQM

In our view, true added value is best found in market niches, spaces which are unattractive to others due to a lack of expertise or the “business opportunity” for the manager being limited in scope. For example, M&A in Australia is a market niche with sufficient opportunity for small and midsized investors, but insufficient capacity for large institutions. It requires years of dedicated experience to do well, a disciplined investment approach, and significant resourcing and monitoring. The relatively small (albeit sufficient) opportunity set, requisite experience and focus needed, and significant cost from required resourcing for constant market monitoring, means that it is an unattractive space for most fund managers. It is niches like this that are the best spaces to look for good alternative managers.

Furthermore, investors should expect to see good results being produced from their managers over multi-year periods. A good result from a true alternative is far superior to a good result from a long only equity manager in a bull market, given there is no free kick from markets going up or from carrying additional beta risks. Many active managers were caught out in October from carrying excessive market risks, and investors have little reason to think this won’t happen again. While short term performance will always be somewhat unpredictable - with the odd month like October providing meaningful information - over the longer term an effective investment process is most likely to work, and a collection of these strategies even more so.

(3) A transparent, understandable and coherent investment approach

Too many alternative managers are “blackbox” in nature and their strategies incomprehensible. They are effectively saying “trust us” to their investors. However, and very importantly, their interests may not be aligned with yours as an investor. For example, they be rewarded by asset gathering due to the collection of large fixed fees on a large asset base, whereas investors need uncorrelated positive performance alone. Investors hence need to understand the investment strategy and the alignment of the manager.

Many alternatives also operate in intensely competitive markets or charge large amounts for simple approaches that are relatively easy to replicate, relatively non-diversifying and/or challenged by volatile and choppy market conditions. For thoughtful investors, it does not make sense to overly rely upon these to build alternative allocations, and certainly not do so ahead of the inclusion of more value adding alternatives.

(4) Strong alignment of interests

If they really believe in their strategy and working for their clients, many fund managers could demonstrate stronger alignment of interest with their investors. Investors could also demand it more and support those managers who unequivocally and quite obviously align themselves with investors. Too many alternative managers benefit by asset gathering alone rather than by performance; if a manager is managing a large amount of funds with significant base fees, their interests are not as well aligned with investors as they could be. Simply put, if your manager can make millions while you make nothing or lose money, you might want to consider whether there is a better way! Hence, I believe investors should look for managers which clearly signal to everyone that their interests are aligned with their investors. One way market neutral managers can do this is by being remunerated purely on positive results above cash, which is highly aligned with clients. This usually demonstrates strong conviction by the manager in their return prospects, which is also a useful signal for investors. Highly aligned fees are particularly important for alternative managers when so many alternative managers charge large fees to produce mediocre performance. As an aside, investors should be prepared to pay more for alternative managers which are capacity limited and rely upon resource intensive approaches, particularly those with greater alignment with clients.

Summary

Investors need to be proactive if they are to avoid too much damage from an eventual and potential retracement in the “bubble in everything”, while still having good prospects of making strong returns. Advisers and many funds are not doing nearly enough to make their portfolios non-binary in nature, and are not properly addressing the big picture risks and issues in the current market environment. There are incredibly strong reasons for forward looking outcome orientated investors to have more substantial alternative allocations in their portfolios, and in many cases to reorientate their current alternative allocations to more prospective and aligned managers. Alternative managers also need to do more to bring more useful and aligned offerings to market; I can guarantee at least some interest in them!

Investors need to choose their alternatives managers carefully if they are to maximise the benefits and minimise the risks from highly attractive alternatives.

The following attributes are key factors to consider:

- Lack of market correlation and sensitivity

- Genuine return potential and history of demonstrated positive outcomes in difficult market conditions

- A transparent, understandable and coherent investment process, ideally in a market niche with less competition.

- Unequivocal strong alignment of interests with investors e.g. a performance fee only approach.

Important Notice

Jerome Lander is Managing Director of boutique investment firm Procapital and an Authorised Representative of Harvest Lane Capital Pty Limited AFSL No. 425334, which manages the Harvest Lane Absolute Return Fund. This communication is for informational purposes only and is a thought piece which represents the views of the author alone. It is not intended as an offer for the purchase or sale of any financial instrument. It does not constitute personal or formal advice of any kind and should not be relied upon as such. Its accuracy cannot be assured. All opinions and views expressed constitute judgment as of the date of writing and may change at any time without notice and without obligation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's more challenging investment environment. Jerome has achieved net returns for clients of around 20% in both the challenging 2020 year and in 2021, with much lower drawdowns and volatility than Australian equities and hence much superior risk adjusted returns. His Wealthlander Diversified Alternative fund targets double digit returns annually for wholesale clients, with lower volatility and greater consistency than Australian equities, using a diversified multi-asset portfolio approach.

2 topics

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Dr Jerome Lander is a highly experienced, proven Portfolio Manager and a specialist in outcome-based and absolute return investing, which is a client centric approach aligned with many peoples' preferences - and one which is well suited to today's...

Expertise

Comments

Comments

Sign In or Join Free to comment