TOL - 5th Feb, 2021

4 key macro signals and how to position your portfolio

Alas, the start to 2021 is not as ‘fresh’ as we would have liked. We have not exited 2020 with a clean slate. A renewed global surge in the pandemic through December has delivered rising mobility restrictions in many regions as the year has got underway, even with a quickening vaccine rollout. Despite this, equity markets— and bond yields—have risen further to reflect optimism that a growth and earnings recovery still lies ahead. And, once again, asset valuations have become challenging. Top of mind for 2021 is whether we should, firstly, remain moderately ‘risk-on’ and secondly, if so, how to best manage portfolios through a year with likely elevated volatility and potential risks.

The virus, the politics and the policy…

A lot has transpired over recent months. While a ‘holiday season’ for many, key developments since our early December letter have had meaningful impacts on the outlook for economies and markets:

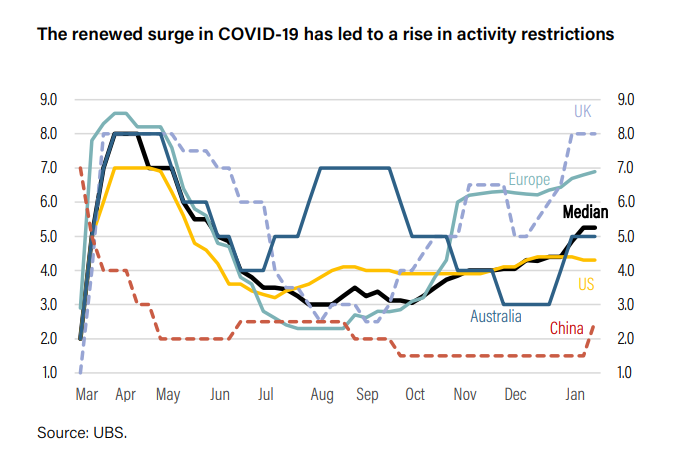

There has been a COVID-19 resurgence, most particularly in the UK, Europe and the US, while Australia and parts of the emerging markets have also had new outbreaks. This has led to a renewed pick-up in mobility restrictions (see the chart below), which will likely weigh noticeably on early 2021 growth.

Political uncertainty has eased. Beyond the affront to US democracy associated with supporters of former president Trump storming Capitol Hill, the transition of US power is behind us. The Democrats surprised by taking control of the Senate, a Brexit deal of sorts was done very late in December, and the Europeans finally agreed their stimulus deal.

Policy stimulus intensified, as President Biden announced his planned, larger-than-expected USD 1.9 trillion stimulus, the European Union’s (EU) EUR 750 billion recovery fund progressed, Japan approved its third stimulus package, and the UK flagged another stimulus post-April. More supportive monetary messages were also forthcoming from global central banks.

Overall, and to a significant extent, the drivers of a long-awaited economic

recovery have strengthened. Fears of a fiscal cliff have been further eased by

another round of support, equity-supportive record low rates appear in play for at

least the bulk of this year, and the various vaccines are being rolled out through

H1 2021 (and to date appear effective against evolving mutations).

However, the resurgence in virus cases and tighter mobility restrictions now seem certain to extend the loss of growth momentum in Q4 2020 that we predicted in our 2021 outlook, at least partially into Q1 2021. Markets appear to have taken this in their stride. As Longview Economics notes, “most key country/regional equity indices 15–25% in the past 2½ months”.

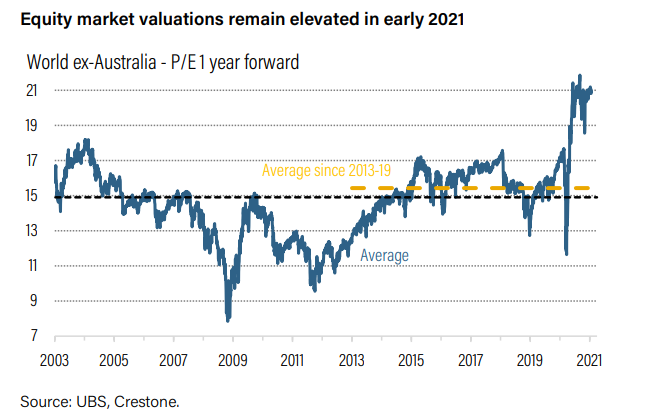

Indeed, our so far elusive improvement in equity valuations, reflecting a view that

elevated price-earnings (P/E) ratios can contract (as P rises, but E rises faster),

has yet to materialise (see the chart below). Equity valuations remain as

challenging as they were in H2 2020, and the risk of a near-term correction in

prices, or at least heightened volatility, has risen.

Top of mind for 2021 is, therefore, whether we should remain moderately ‘risk on’ and, if so, how we best manage portfolios through potential volatility and risk. As far as answering the first question, our core positive outlook for 2021 (as discussed in December’s Core Offerings) remains intact. Though, arguably, the ‘good news’ of falling new virus cases and recovering growth, driven by the reopening of economies, may be more evident in Q2 than in Q1 (as we had first hoped). Our forecast recovery is delayed, not derailed.

Indeed, we note that relative to December, forecasts for global growth have moved higher, predicated on falling virus trends prior to mid-year. UBS has lifted its 2021 growth forecast from 6.1% to 6.2%, with 2022 seen similarly buoyant at 5.3%. The International Monetary Fund in late January also raised its 2021 forecast from 5.2% to 5.5%.

Still, it is worth considering the key macro-economic signals for 2021 we are

watching closely to ascertain whether any disappointment is temporary or a

reason to reshape our thinking.

Some key macro signals for 2021

As 2020 showed, a year is a long time in forecasting! Yet, amid uncertainty, there are some drivers we believe remain reasonably assured. These include ongoing policy stimulus (at least relative to pre-COVID-19), with any fiscal cliff largely deferred until 2022 and official interest rates pegged as close to zero as possible. Moreover, for a change, we expect macro-economic activity trends may play a more dominant role for markets than geo-politics.

1. The pace of the vaccine rollout (and its success against mutations)

This will garner increasing market attention and provide a bellwether on the likely timing of a sustained decline in new COVID-19 cases. In the UK, the government is targeting 15 million inoculations by mid-February. UBS is expecting a third of the world’s population to be inoculated in 2021, leading to a sustained downward trend in new virus cases by mid this year. Whether the pace of the vaccine rollout proves faster or slower than expected, and whether current (or new) vaccines can prove effective against the virus’ mutations will be key to assessing the extent to which mobility restrictions can be eased and growth momentum recover.

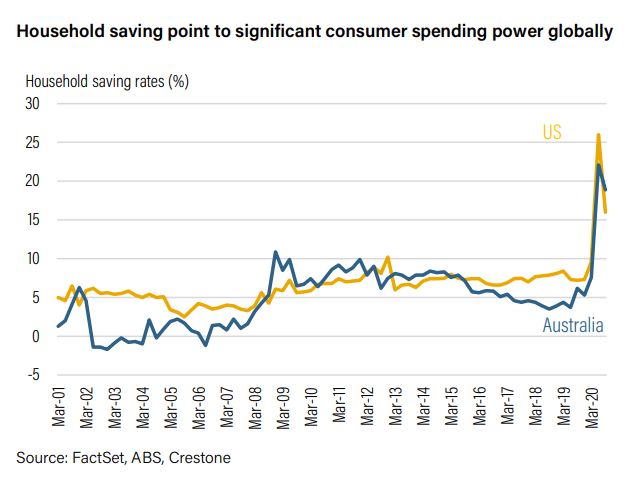

2. Will easing consumer fear and high savings drive spending?

The coming year is likely to be characterised by an accelerated vaccine rollout, falling new virus cases, and easing mobility restrictions globally. While it is our strong belief, there is no certainty that less consumer fear will combine with the recent sharp increase in consumer purchasing power (reflected in sharply higher saving rates globally, see the chart below) to drive faster consumer demand. It has, however, been true for Australia and China. The pace at which consumer spending picks up will be key to assessing the outlook for global growth, and the extent to which corporate earnings can recover in line (or not) with expectations. The outlook for inflation will also be impacted by the strength of consumer demand. The significant acceleration in property sectors globally, including Australia, the US and the UK, should also boost consumer confidence and spending through rising wealth impacts.

3. Inflation pressures could surprise, albeit they will likely not be sustained

A sustained structural pick-up in near-term inflation appears unlikely any time

soon, reflecting vast swathes of spare capacity and high unemployment rates

across most economies, including Australia. However, it would not be surprising

to see a H1 2021/mid-year burst of cyclical (not structural) inflation as a

reacceleration in consumer activity (as mobility restrictions are eased) outpaces

the recovery in supply and production chains.

A higher-than-expected burst of inflation, especially in the US, could spook

equities and other risk markets. But given global demand is not expected to

regather its pre-virus level until late 2021 (and that pace was not obviously

pushing inflation above central bank targets), any inflation surprise is unlikely to

be sustained in 2021. Signs of a faster fall in unemployment, or rising wage

pressures globally, will be a more important longer-term signal to watch.

4. When will central banks change their tone?

It’s hard to deny some level of exuberance in equity markets as 2021 gets

underway. History is, however, relatively clear that markets typically run into

problems when central bank liquidity is withdrawn. As Charles Kindleberger

famously notes in his 1978 book, Manias, Panics, and Crashes, while there are

typically four things that define a bubble, there’s only one thing that has

historically burst them, namely the withdrawal of cheap money.

A cyclical burst of inflation in H1 2021 is unlikely to foster talk by central banks of

tapering. They will hold firm to messages of sustained stimulus (not least to

support the financing of government deficits) for much of 2021, alluding to high

unemployment as their defence. But a shift in tone through H2 2021, that may be

positioning for reduced liquidity in 2022, may have a potential early and significant

impact on long-dated yields and equity valuations.

Maintaining our current positioning in early 2021

Our answer to the first question, despite the macro risks to be monitored, is that we should retain our recommended moderate risk-on positioning for portfolios, as discussed in December’s 2021 outlook. On a three-year horizon, return expectations remain under downward pressure. However, sustained low yields should continue to favour returns in equities (particularly non-US equities) relative to fixed income. We have retained our neutral positioning in listed credit markets, albeit we view them as favourable sources of relative return in fixed income. With traditional equity and bond valuations stretched, we continue to recommend full allocations to alternative investments.

Some key strategies for 2021

So, considering the second question, how should we manage portfolios through 2021? Put another way, what ‘correction’ in equity markets would we not buy? Any pull-back driven by a short-term inflation burst, delay in the pace of the vaccine’s success, or a more cautious consumer recovery is likely to foster ongoing policy support (as a structural uplift in inflation is further delayed). In contrast, a multi-year pull-back in risk is more likely if evidence mounts of a structural inflation uplift or a collective failure of vaccines against the virus and its mutations. These latter risks, for now, appear low.

Bring portfolios into line with strategic positioning—Be conscious that equity weights have likely drifted higher, given market gains over recent months. Prior reluctance to invest in sovereign bonds should also be curbed, given US 10-year Treasuries have risen from lows of 0.60% to 1.10% recently. With most portfolios still short of strategic allocations to alternative investments, this should remain a focus in 2021, particularly given the relatively high prices for traditional fixed income and equity assets. Allocations to emerging market equities are also worthy of focus.

The equity growth-to-value rotation has further to go—The recent rotation to value (and cyclicals) from growth (and defensives) has been significant, as we expected. While this should not be overplayed from here, given the quality focus in our portfolios and momentum in tech and ‘green’ themes, a likely further rise in bond yields during 2021 suggests this rotation has further to go. A lack of exposure to cyclicals and industrials and non-US equities (relative to US) could lead to underperformance over the coming year.

Consider investing in multi-year structural themes—Investing in durable multiyear themes can provide less volatility in the short-term and more sustained long-term gains. These have been refreshed for 2021 and include decarbonisation and accelerating tech adoption, among others.

Bonds are a necessary defence, but real assets can help—Record low policy rates are challenging medium-term fixed income returns. Duration risk on a one to three-year view has led some to question the value of bonds relative to cash. However, at over 1%, US and Australian bonds now provide more portfolio defensiveness than they did last year. Any equity correction is likely to see a renewed bond rally. Defensive alternatives, such as real assets, that have a similar risk profile (albeit less liquid) can also be considered as a partial substitute for listed defensive income assets (sovereign bonds).

Build appropriate allocations to alternatives—It’s not unusual for portfolio allocations to be above their tactical weight for equities and below their strategic allocation for alternatives. But with traditional assets relatively expensive, 2021 is an opportunity to build alternative allocations. Given the current point in the macro and market cycle, alternatives can also provide:

- a hedge against inflation via real assets

- defensive income through real assets, and potentially

- less vulnerability via unlisted private markets (both equity and credit) to market volatility.

Look for opportunities to lift cash and yield returns—With the Reserve Bank of

Australia (RBA) policy rate at a record low and term deposits returning less than

1%, investors should look for solutions to maintain liquidity and earn returns above

the cash rate. This could be actively managed short-maturity cash and fixed

income strategies for those with high liquidity needs. For those able to tolerate

higher levels of illiquidity, cash and liquidity allocations could include private

market alternatives with predictable yields, such as alternative debt and

real asset.

Learn what Crestone can do for your portfolio

With access to an unrivalled network of strategic partners and specialist investment managers, Crestone Wealth Management offer one of the most comprehensive and global product and service offerings in Australian wealth management. Click 'contact' below to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

1 contributor mentioned

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Scott has more than 20 years’ experience in global financial markets and investment banking, providing extensive economics research and investment strategy across equity and fixed income markets.

Expertise

Comments

Comments

Sign In or Join Free to comment