Strategies to protect your portfolio

Marcus Tuck

Mason Stevens

Straw hats are cheaper to buy in winter, and the best time to repair a leaking roof is when it's not raining. In a similar vein, when market volatility is low and inexpensive, it's often a good time to buy some protection for equity portfolios to guard against "X-factor" downside risks.

The X-factor, by definition, could come from anywhere. Geopolitical risks are rising. Whether it's impeachment risk in the US, escalating tit-for-tat retaliatory action between the US and Russia, missile launches in North Korea, tensions with China over the South China Sea and North Korea, or problems in the Middle East, the political temperature is rising. President Putin has ordered the US to reduce its staff at its diplomatic missions in Russia by 755, or nearly two thirds, in retaliation for new sanctions against Russia approved by Congress.

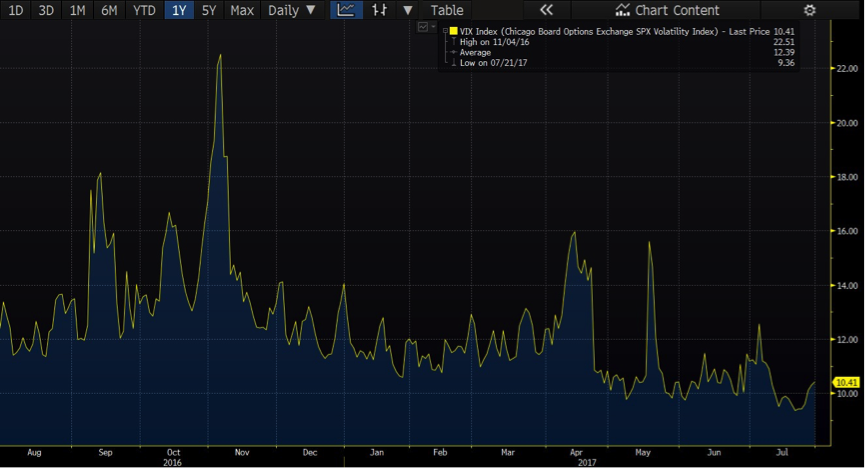

US stock market indices are at or near record highs and PE ratios are elevated. Offsetting this, earnings are growing and generally surprising on the upside, the interest rate outlook is fairly benign, and equity risk premia compared to bonds are not unreasonable. Whilst political risks can be easily overstated when it comes to equity markets, some downside protection would be prudent. The VIX volatility index is at 10.41, which is still low by historical standards but above its recent record intraday low of 9.04 (see chart).

Investors wanting to put some insurance protection into their equity portfolios might consider hedging their exposure using:

- Exchange listed options or

- Exchange traded funds (ETFs).

Hedging with put options

The easiest, and least capital-intensive, way of buying protection is to buy an ASX 200 index put option that expires in the coming months, say in December this year. The further out-of-the-money the index put is the cheaper the premium paid. As an example only, a 5700 strike put option (just slightly below the current index level of 5720.6) expiring on 21 December trades at a market premium of 233 points (at yesterday's close), with an implied volatility of 18.4%. Buying one put option contract costs $10 per point - in this example a payment of $2,330. The put option will increase in value if the market falls significantly, at which time one might look to close the position. Care needs to be taken with such instruments as put options though, because if the market level is not below the strike price at expiry they will expire worthless.

3 ETF's to hedge the market

An alternative way of hedging is by using bear ETFs. BetaShares has three bear ETFs listed on the ASX:

- The Australian Equities Bear Fund (BEAR.AXW),

- The Australian Equities Strong Bear Fund (BBOZ.AXW) and

- The US Equities Strong Bear Fund - Currency Hedged (BBUS.AXW).

The exposures are directly against the relevant index futures (minus a 1.19% p.a. management fee), with leverage of 2 to 2.75 times achieved in the case of the Strong Bear ETFs.

If following any of these hedging strategies they need to be carefully scaled and managed. If equity markets do fall then these strategies are a good way of hedging market risk. However, if equity markets rise instead, the payment lost should be viewed as paying insurance premiums against market risk, in much the same way as paying for insurance on any other asset. Please talk to your financial advisor if implementing any of these strategies.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

1 topic

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management