7 considerations to help you invest in corporate bonds?

Elizabeth Moran

Elizabeth Moran Consulting

Investing direct or through exchange traded funds (ETFs), or managed funds has advantages and disadvantages; just like investing in shares, the decision depends upon the individual. While my preference is direct investment, the minimum needed is $250,000, making it difficult for smaller investors to access.

Here are seven key considerations for investors when deciding how to invest in bonds:

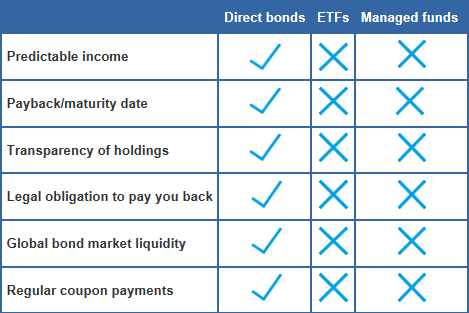

1. Four key direct bond benefits

- Funds are returned to you at maturity

- Interest is known at the time you buy the bonds as is the date when interest is paid

- Investment decisions are based on expected future returns

- The opportunity to outperform by investing in and trading a smaller number of good relative value bonds

Unfortunately, these features are lost when you invest in a managed fund. When bonds mature in a managed fund or ETF, funds are usually reinvested. Income is absorbed into the fund and the fund manager decides when to pay interest.

Bond funds advertise historical returns. Direct investment projects future returns giving you a better sense of expected income and overall yield to maturity.

Source: FIIG Securities

2. Control

Direct bond investment means you decide which companies’ bonds to invest in. While a bond broker might make suggestions about bonds to include in a portfolio, you make the final decision. Direct bond investors know all of the companies in their portfolio and there is complete transparency in this regard.

If you invest direct, you can build a portfolio that suits your investment goals whether these are based around; low risk, high return or the delivery of a monthly cashflow. You also then make the decisions on when to buy, sell or hold, depending on your needs. Bonds, like managed funds can be sold down in small parcels providing liquidity if needed.

On the other hand, if you invest in a managed fund then someone else makes the decisions about what to invest in, when to buy and sell and when to make distributions to investors. They don’t know what you already have in your portfolio, so if you have significant allocations to some sectors, these may be increased through managed fund investments.

You’ll need to decide if you want a passive fund (where there is no or little oversight) and the fund aims to beat a benchmark or an active manager that oversees the portfolio. The distinction is often reflected in the fees, where higher fees are charged for active management. Returns for active funds can significantly outperform passive funds, but this is not always the case.

In a low interest rate environment, it’s much harder for actively managed funds to outperform after higher fees are deducted. Some investors prefer not to invest in certain sectors for ethical or environmental reasons or just because they don’t think the sector is worth investing in. Direct investing allows for that flexibility.

What about ETFs?

Other investors may turn to ETFs, an index based portfolio of underlying assets such as stocks, bonds, oil futures, gold bars or foreign currency that divides ownership of those underlying assets into shares. ETFs are usually structured as a managed investment scheme, where investors hold units in a trust. They can be great tools for retail investors to access markets where only institutional players existed just over a decade ago. See below for advantages and disadvantages of ETFs.

Source: FIIG Securities

3. Time and confidence

Those wanting to invest directly need to take the time to learn about the asset class. If you don’t have the time or perhaps don’t yet have the confidence, managed funds may suit you better.

4. Those with less than $250,000 to invest in corporate bonds

Being able to trade bonds through a dealer/ broker gives you distinct advantages - access to expert opinions on which bonds represent good relative value, access to new originated bonds, not available elsewhere, research and the opportunity to build relationships. You are not just a number and one of many.

For those with less than $250,000 to invest, a corporate bond fund is a good place to start.

It’s really important to understand what you’ve invested in. Don’t make the assumption that all funds are diversified. A fund like the AMP Corporate Bond Fund is well diversified with the top 10 holdings representing just 22% of the fund. But there are others such as the Russell Investments Australian Select Corporate Bond ETF with 76% of its holdings invested in the bonds of the ‘big four banks’ and its only other holding is Telstra. There is very little point using such a fund if your objective is diversification.

5. Transparency fees

Most managed funds do not disclose more than their top ten investments. This means you don’t know what they have invested in. Fund managers typically don’t want competitors to know what’s in their portfolios but this makes it very difficult for investors to analyse the risk of the fund. Direct ownership means you know precisely what you own and can determine if the risk is appropriate for your circumstances.

One of the arguments against investing in bonds directly is the lack of transparency regarding brokerage fees. But anyone that transacts in bonds pays a brokerage fee, so whether you are investing directly or through a managed fund, you are paying brokerage. The advantage of the managed fund is that they buy bonds in larger quantities and so would achieve some scale.

6. Those needing guaranteed short term liquidity

Bond funds don’t actually guarantee liquidity, but it takes a pretty extreme liquidity crisis (such as late 2008) to cause a large corporate bond fund to block redemptions. In normal times, redemption occurs within a few days. Selling individual bonds typically happens on a trade + 2 business day basis.

7. Diversification across your portfolio

If you own a lot of bank stocks or residential property, one thing to watch with a corporate bond fund is the level of bank exposure. Most of the large corporate bond funds have a very high (20%+) exposure to global banks, which means if you already hold bank shares in your SMSF, you are creating a very high allocation to banks across your whole portfolio. Direct bond ownership means you can tailor your bond portfolio to fit in with the rest of your portfolio.

Are you ready to find out how you can earn over 5% pa* with corporate bonds? Click here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

3 topics

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Elizabeth Moran

Fixed Income Specialist

Elizabeth Moran Consulting

Nationally recognised expert in fixed income asset class. Career spans more than 25 years in banking and finance in diverse positions including: education, communication, media, credit research, credit ratings and retail and commercial lending.

Expertise

Comments

Comments

Sign In or Join Free to comment