A franked discussion

Clime Investment Management

Clime Investment Management

The announcement by the Australian Labor Party (“the ALP”) of its policy shift to stop the cash rebate of franked dividends was predictable … and is alarming.

It was predictable because the cash rebates attached to franking could be accessed to an excessive extent by the “mega wealthy”. While they acted within the law, even these ultra-high net worth individuals would probably acknowledge that the franking cash rebates on their large equity portfolios (well above what is required for a pension scheme) was inequitable.

Wikipedia notes -

“A franking credit on dividends received after 1 July 2000 is a refundable tax credit. It is a form of tax paid, which can reduce a taxpayer's total tax liability, and any excess is refunded. For example, an individual with income below the tax-free threshold ($18,200 since 2011/12) pays no tax at all and can get the franking credits back in full as cash, after a tax return is lodged.

“Prior to 1 July 2000 franking credits were "wasting", any excess over one's total tax payable was lost. For example, an individual at that time paying no tax would get nothing back, they merely kept the cash part of the dividend received.”

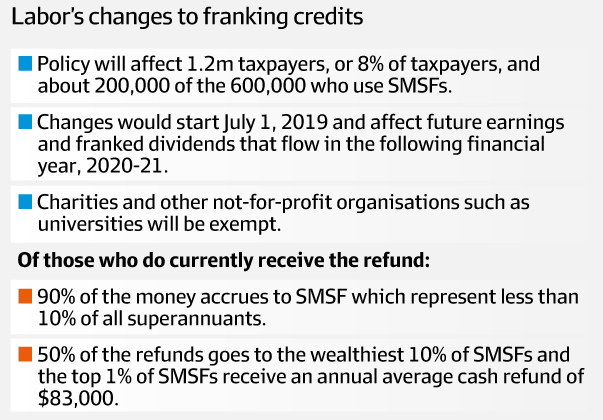

The following release by the ALP notes that about 7,000 SMSF (1% of the total) on average receive $83,000 in cash refunds from franking credits. To receive that amount of cash credit, those funds would need to receive $276,000 in franked dividends. On the assumption of a 4% franked dividend yield, those funds would need to have at least $6.9 million in Australian listed shares. The ALP is justifying a tax change targeting a very few - that has broad and far reaching consequences for the many. Its policy changes are arguably far beyond that which is necessary.

If the ALP is ostensibly targeting the “mega wealthy”, who have used their pension funds as tax minimisation schemes, then that appears to be a legitimate but belated policy shift. The ALP supported the introduction of cash franked rebates (when in Opposition in 2000), and when they were in Government (2007 -2013), they made no attempt to adjust the franking system. Therefore, many typical SMSFs have been managed based on a bi-partisan and enduring approach to franking. This week’s announcement is consequently alarming and will create concerns for many retirees. The proposed sledgehammer adjustment to the franking rebates will affect all pension fund returns (not just SMSFs). It is unwelcome and poorly structured given the low yield world that confronts all investors (see Australian bond yields below).

The proposed ALP policy change will lower the returns for many average SMSFs. These SMSFs, with (say) $1.6 million in pension assets per member (as legislated in the 2017 Federal Budget) are not the funds of the mega wealthy. We suspect that an actuary (adopting the proposed ALP franking cash adjustment on equities) could now question whether the $1.6 million pension cap would be sufficient for a 70-year-old pensioner with a longevity outlook of 18 years.

(In passing, we note that the after-tax returns of pension funds inside industry funds will also be affected. It is particularly strange for the ALP to suggest that only SMSFs will be affected. Is this a covert attempt to coax retirees to fall into industry funds?)

To explain the effect on cash returns of pension funds, consider the example of a “balanced” fund with about 40% invested in Australian listed equities. The $640,000 of equities on average generates a 4% franked yield ($25,600). The franking credit attached to these dividends is approximately $11,000 or 0.68% of the fund. In other words, the franking credit adds 0.68% to the total fund return - this is significant cash flow supporting pension pay out rates that approximate 6% of the fund.

In the above example, the “balanced” pension fund, if the franking credit is changed, will need to generate $11,000 of cash returns from some other asset class to maintain its cash earnings rate. At the same 4% cash income return (that is, 1% above TDs and 2% above ten-year bond yields), the fund will require an extra $265,000 in capital. The ALP has not even considered this consequence.

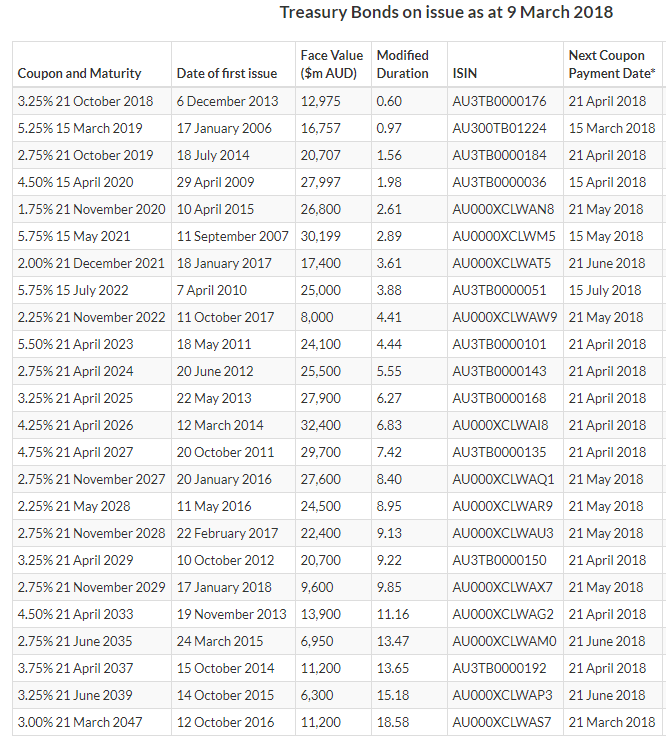

The cash flow problem for balanced funds is exemplified in the next table, which highlights the current yields of Australian Commonwealth bonds on issue. In the past, it was said that the allocation to bonds (supposedly “low risk” assets) should rise as a beneficiary of a pension fund aged. A pithy “rule of thumb” was that the percentage asset allocation of a fund to bonds should correspond with the age of the member. For instance, a 60-year-old would have 60% of their pension fund in bonds, and an 80-year-old would have 80%. Of course, in that bygone era, bond yields were significantly higher than inflation and therefore generated a reasonable risk-free return that could match pension liabilities. Today, pension funds must look elsewhere for yield and the equity market, with franking, fills the breach.

A more logical approach

To some extent, the changes announced in last year’s budget to limit SMSF pension fund assets (and tax-free status) to $1.6 million were designed to restrict tax benefits flowing to “overfunded” funds and the extremely wealthy. A super balance above $1.6 million now attracts an accumulation tax of 15% on fund income.

The ALP is arguing that those legislated changes did not go far enough; but their proposals will erode the returns of pension funds and upset the balanced asset allocation approach increasingly adopted by retirees.

While there is still debate as to whether the $1.6 million pension fund limit is reasonable (given it is not age adjusted), we can use it as a basis to design a more sensible alternative to the ALP sledgehammer policy.

In our view, the claim for franking credit rebates should be based upon a “reasonableness test”. Based on the government pension rate, the tax-free threshold of $18,000, the average 6% pension payout on a $1.6 million fund and a notional allocation of 30% to 40% to Australian equities in a balanced pension fund, we think that a $12,000 franking rebate limit could be introduced. This limit could be claimed by each member in pension mode in a SMSF and therefore supplement the income generated from non-equity and lower risk investments. This rebate would allow a member to have $1 million in Australian equities (assuming a 4% fully franked yield), before the rebate is fully utilised.

Some consequences of the ALP policy

As noted above, we suspect that the ALP policy makers have not properly considered or understood the full consequences of a cash rebate change. The biggest issue is the asset allocation design of a SMSF to meet the progressive needs of pension payments with a risk/return analysis.

If the policy were adopted, we perceive two consequences and risks.

1. The value of equity investments would be affected as the pre-tax yield flowing from franking credits would fall. The lower yield on equities would push more asset allocation to higher yielding investments, eg high quality direct property rental streams would become well bid; and

2. We wonder whether the hybrid yield market could become an unintended victim and suffer fallout. Most hybrids include in their terms a “gross-up” adjustment in the event of franking becoming unavailable or a tax change occurring. In this case, the franking stays attached to a hybrid distribution, but the cash franking rebate is lost. Our concern is whether the hybrid securities have contemplated such a change.

While it is good that taxation is now on the political agenda, it is paramount that both sides of parliament agree that a proper universal review of tax is needed … not a piecemeal approach. Once again, the ALP has proposed policy in a vacuum, and it reminds us of their attack on salary packaging in the run up to the 2015 election.

“I have to live fast and die young because of poor retirement planning”

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

5 topics

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Clime Investment Management

Funds Management & Stock Research

Clime Investment Management

The Clime Group is a respected and independent Australian Financial Services Company, which seeks to deliver excellent service and strong risk-adjusted total returns, closely aligned with the objectives of our clients.

Expertise

Comments

Comments

Sign In or Join Free to comment