A key question most investors ignore, do you?

Investors ask themselves many different questions when considering an investment thesis; how fast can the company grow? How expensive is it? How good are the management? But one question they often fail to consider is, 'am I wrong?' Troy Angus, Head of the Australian Equities Fund at Paradice Investment Management, says it’s important for investors to always consider the counter factual.

“When a stock goes up, and you don’t own it, prima-facie, you’re wrong. You should be constantly reassessing the investment case and wondering, ‘what did I get wrong here?”

This is a question they were forced to ask themselves again recently, as expensive technology stocks on the ASX have continued to rally.

Hear the rest of the story in this week’s episode of The Rules of Investing podcast. He also shares one thematic that’s a major beneficiary of recent policies, and his preferred exposure to that theme.

Time stamps

- 2:02 – Troy’s story: from Darwin to London

- 4:42 – The Paradice history and philosophy

- 6:44 – What does the perfect investment look like?

- 7:45 – How does a large-cap strategy compare to small and mid-ones?

- 9:23 – Where are we on the boom and bust curve?

- 12:50 – Are equity prices reflecting our current reality?

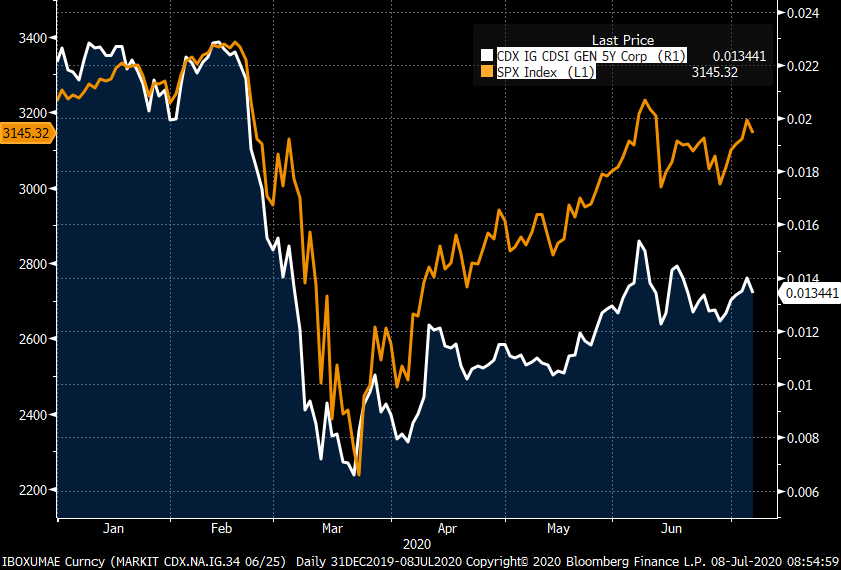

- 15:10 - The disconnect between equity and credit markets

- 16:44 – The significant changes Troy’s made in his portfolio recently

- 22:08 – Is it a good idea to chase momentum stocks?

- 23:55 – IDP Education: are the headwinds currently reflected in the share price?

- 27:23 – What to expect from oil markets

- 31:06 – The enduring challenges faced by the financial industry

- 33:33 – An investment Troy favours over the medium to long-term

- 39:32 – Troy answers our three favourite questions

Accompanying content

Currently credit markets imply the SP500 should be about 10% lower

Gold historically has had periods where it very significantly outperforms the SP500

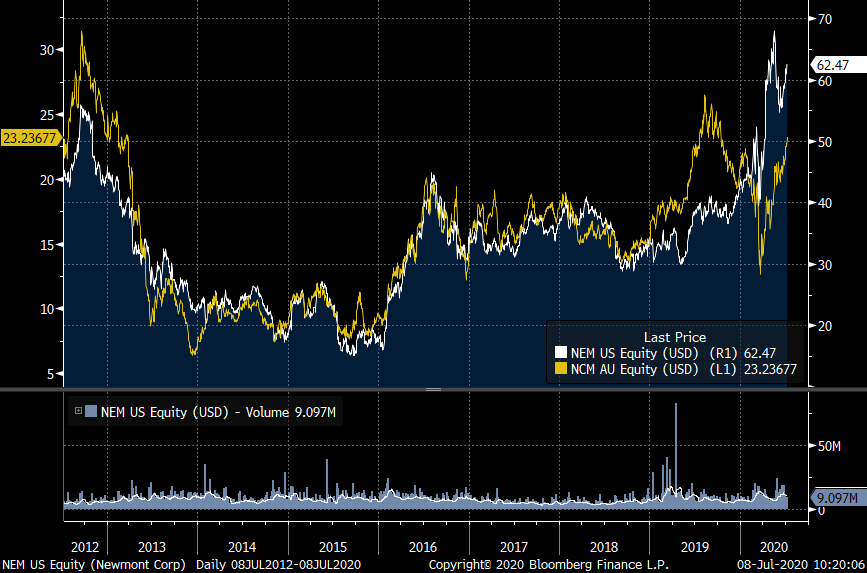

Newcrest (yellow) in USD has underperformed its rival, Newmont (white)

Book recommendation. Valuation: Measuring and Managing the Value of Companies. By Tim Koller, Marc Goedhart, and David Wessels.

Clients and performance come first

The Paradice difference comes down to accountability, alignment, experience and performance. Click the ‘contact’ button below to get in touch.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

The Rules of Investing is one of Australia's top investing podcasts. We interview the leading investment minds from Australia and overseas to better understand their processes and philosophy. After launching in October 2017, there have been over 150 episodes published - you can access all content on Livewire Markets, Spotify and Apple Podcasts.

Featuring

Troy Angus,

Paradice Investment Management

Troy is a Director at Paradice and manages the Australian Large Cap Equities portfolios. He has over 19 years’ finance experience with 17 of those gained in the Australian equity market. Troy also has an MBA from London Business School.

........

Livewire gives readers access to information and educational content provided by financial services professionals and companies ("Livewire Contributors"). Livewire does not operate under an Australian financial services licence and relies on the exemption available under section 911A(2)(eb) of the Corporations Act 2001 (Cth) in respect of any advice given. Any advice on this site is general in nature and does not take into consideration your objectives, financial situation or needs. Before making a decision please consider these and any relevant Product Disclosure Statement. Livewire has commercial relationships with some Livewire Contributors.

4 stocks mentioned

Livewire Markets

The Rules of Investing is one of Australia's top investing podcasts. We interview the leading investment minds from Australia and overseas to better understand their processes and philosophy. After launching in October 2017, there have been over...

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management