A new player riding the infrastructure boom

Andrew Smith

Perennial Value Management

We first heard of Acrow (ACF) many years ago before it was listed, when researching listed competitor GCS. This was before the east coast infrastructure boom, and thus the business was struggling and capital deprived under private equity ownership. Despite that, there were several corporates interested in acquiring the assets at the time. So when a broker approached us to cornerstone the back-door listing recently we were already familiar with the business.

We were also pleasantly surprised by the quality of the proposed board, in particular with Chairman Peter Lancken who brought excellent experience from his days managing Kennards (in addition the Kennards family were also participating in the raising). Another director we were familiar with was Mike Hill who is also on the board of Rhipe Limited and Janison Education – two other successful investments in our Microcap Opportunities Trust.

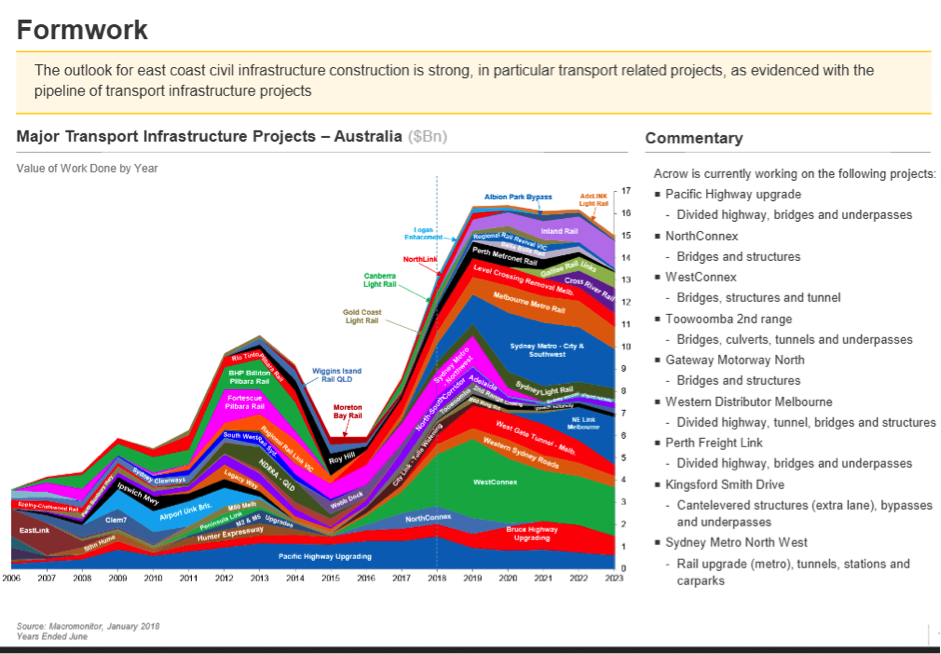

Exposure to the East Coast infrastructure boom

The key driver, and one of the main reasons for our investment, is the exposure Acrow has to the east coast infrastructure boom, with key Acrow contracts shown below.

Source: Acrow FY18 Investor Presentation

In addition to providing a visible and growing pipeline, the scale and complexity of this work reduces competition from smaller, less capable private operators. Furthermore, the long-term nature of the work enables a better cost structure due to forward planning.

We also see the pipeline of infrastructure work growing beyond what is depicted below with Badgerys Creek airport as well as recent announcements in QLD and VIC providing further upside to sector demand and pushing the peak activity to 2023 on our estimates.

How was this missed by the market?

The typically poor performance of businesses listing post IPO ownership probably turned several investors away. We are equally cautious buying from private equity but in this case it was the last asset in the fund and from what we could observe after a failed sale process some years earlier they were motivated sellers. We also saw strong ongoing equity alignment with the board and senior management.

The second factor potentially was a perceived reliance on residential construction which was clearly starting to peak at the time of the raising. This was also an area we were concerned with, however, the recent pivot to civil infrastructure and the prospect of recovering commercial construction more than offset the residential weakness we were forecasting.

Considerable further upside

While the stock has already performed strongly from the 20c raising we see considerable further upside. We have the stock currently on a PE of 7x FY19 (a 58% discount to Small Ords average), which is a considerable discount to market.

We don’t have pre-determined price targets (preferring instead to look at relative valuation to the market each day) however as an indication in the current market and given the nature of the business, a PE of 10x (equating to EV/EBIT of 9x) would seem appropriate – using this multiple would give a 75c share price

Opportunities from recent acquisition

In addition to a strong result in FY18 and the attractive exposure to infrastructure, we believe the recent strong share price reflects the quality of the recent Natform acquisition. This is a high-end engineering solution providing adjustable screening during commercial high rise construction. The business is currently operating only in NSW, ACT and QLD and we expect future growth to be driven by geographic expansion as well as cross-selling to the existing Acrow client base.

The metrics of the acquisition were also attractive with a 4x EBITDA multiple with upside to the vendor from a two-year earnout. Again we took comfort from an alignment of interest with Acrow shareholders, with the vendor Margaret Prokop continuing to run the business and also joining the Acrow board. In addition, $3.5m of the deal was taken in Acrow shares.

Disclaimer: Please note that these are the views of the writer and not necessarily the views of Perennial. This article does not take into account your investment objectives, particular needs or financial situation.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew commenced with Perennial Value in July 2008.

Prior to joining Perennial Value, Andrew was Head of Research at Linwar Securities, a boutique broker specialising in smaller company research. Andrew joined Linwar in 2003 and during this time he gained a deep understanding of stocks across the small cap spectrum.

Andrew commenced his career at Tyndall in their graduate program, where he gained experience across a number of functions including accounting, product development and stock analysis. Andrew is responsible for managing the Small and Microcap portfolios at Perennial Value.

Andrew attained First Class Honours in Finance while achieving his Bachelor of Commerce degree at Sydney University.

1 topic

1 stock mentioned

Andrew Smith

Head of Smaller Companies and Microcaps

Perennial Value Management

Andrew commenced with Perennial Value in July 2008. Prior to joining Perennial Value, Andrew was Head of Research at Linwar Securities, a boutique broker specialising in smaller company research. Andrew joined Linwar in 2003 and during this...

Expertise

Andrew Smith

Head of Smaller Companies and Microcaps

Perennial Value Management

Andrew commenced with Perennial Value in July 2008. Prior to joining Perennial Value, Andrew was Head of Research at Linwar Securities, a boutique broker specialising in smaller company research. Andrew joined Linwar in 2003 and during this...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management