A record year for buybacks

Marcus Tuck

Mason Stevens

Buybacks can support stock prices by reducing share counts and boosting earnings per share, although that is no guarantee of producing a rising share price. Fundamentals such as revenues, underlying earnings trends, competitive prospects and interest rates still count for more.

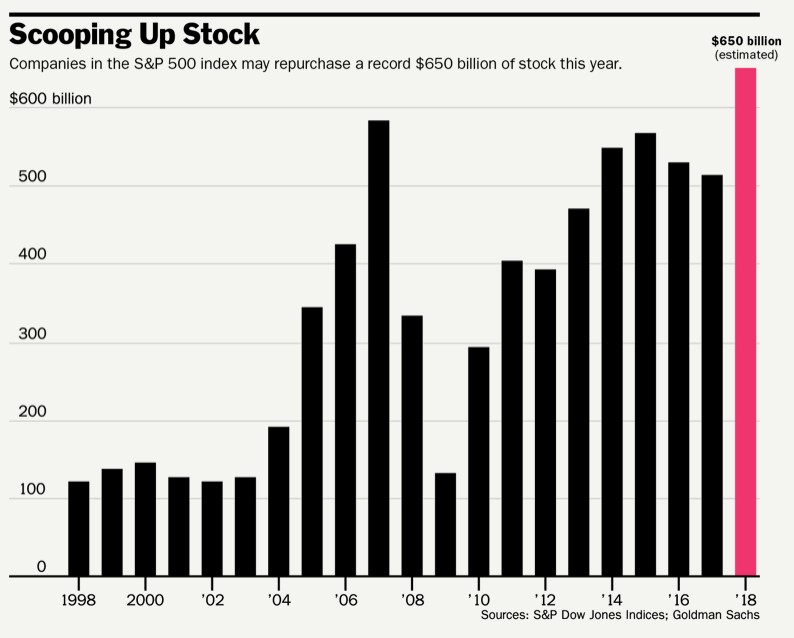

This year looks like being a record one for share buybacks by US companies. Apple's recent news of a US$100 billion buyback program at the time of announcing its stronger than expected March quarter earnings report helped propel the stock to a record high.

Goldman Sachs estimate that S&P 500 companies are on track to announce US$650 billion worth of buybacks this year, which would exceed the previous record of US$589 billion set in 2007 (see chart).

A recent Barron's article points out that the latest buybacks will on average offer investors an effective "yield" of about 3%, calculated by dividing the US$650 billion repurchases by the approximately US$23 trillion market value of the S&P 500 Index. Combine that with the 1.9% current dividend yield and investors should get a nearly 5% combined yield this year.

Better than bonds?

That combined yield stacks up well against alternatives, with US money market rates approaching 2% and the 10-year Treasury yield at 3%. It was this arithmetic and the prospect of higher corporate earnings and dividends that prompted Warren Buffett to say on CNBC earlier this year, "If you had to choose between buying long-term bonds or equities, I would choose equities in a minute."

Based on the 2017 buybacks plus dividend yields, companies that produced combined yields of 5% or higher last year included Citigroup 9.6%, Marathon Petroleum 9.1%, Marriott International 7.3%, Boeing 6.6%, JPMorgan Chase 6.0% and Apple 5.0%.

More buybacks coming

There are likely to be more announcements of big stock repurchases and dividend increases coming soon from the banks, once the Federal Reserve completes its annual stress tests in June. According to Barclays, the US banks should return nearly all of their net income to shareholders in buybacks and dividends in the 12 months starting in July, roughly two-thirds in buybacks and one-third in dividends. The repurchase yield among banks should average more than 5%, with Citigroup expected to buy back about 10% of its shares, and Bank of America and Wells Fargo 7% each. The average dividend yield is 2%.

There is ongoing debate over whether share repurchases really lift stock prices in the long term. IBM and General Electric are two notable examples of companies that executed large buybacks at higher prices and have now scaled back or eliminated those programs in the face of earnings pressures. There is also the question of whether a company would be better off using its cash to make productive investments rather than buy back its shares. However, there is little evidence currently that the big companies making buybacks are skimping on capital spending.

The market constantly evaluates management decisions on the use of capital and judges which uses will offer the best returns. A company such as Amazon is better off investing capital in high-returning businesses, whereas investors are happy to see a more mature business such as Apple use some of its cash for buybacks.

Apple likely to continue doing buybacks

Apple certainly isn't starving its operations of capital. It ploughed nearly US$13 billion into research and development and capital spending in the first half of its current fiscal year ending 30 September. In the first quarter, Apple made US$23.5 billion of stock repurchases, which is a record amount. It has now repurchased US$200 billion of stock since its program began in 2012. To balance it, Apple emphasized that it plans US$30 billion of domestic capital expenditures in the next five years and will create 20,000 new jobs in the US.

Analysts expect Apple to buy back US$70-80 billion of stock annually in the next few years. That translates into an impressive buyback yield of 7% to 8%. Apple is funding the repurchases with its ample earnings power, now about US$60 billion a year, and by gradually bringing down to zero its net cash position of US$145 billion. After a 16% increase in its dividend payout recently, Apple yields 1.5%. Apple is a good example of an American company bringing back cash from abroad under the Trump administration's new tax regime, with much of it going into buybacks and dividends.

Berkshire Hathaway is Apple's biggest shareholder with about a 5% stake. Warren Buffett said at his recent annual meeting, "I'm delighted to see them repurchasing shares. I love the idea of having our 5% [stake] maybe grow to 6% or 7% without our laying out a dime." Apple's share count, which stands at 4.9 billion, could drop by 15% by September 2020. It already has fallen almost 25% since the repurchase program began.

Two other companies sitting on a big pile of cash are Berkshire Hathaway itself and Alphabet. Both have roughly US$100 billion of cash. But neither are keen on buying back a lot of their own stock. Alphabet began a share repurchase program in late 2015, but it's modest in size and hasn't been enough to offset the large amount of stock-based compensation it hands out. Alphabet bought back US$4.8 billion in stock last year, and issued US$7.7 billion in shares to employees. Its share count edged up to 705 million at the end of the first quarter, from 702 million a year earlier.

Well-executed buyback programs are done opportunistically whenever share prices drop, subject to blackout periods a month before earnings announcements. With a record amount of buyback firepower waiting in the wings, it should contribute to the well-established trend of buying share market dips for a while longer.

Disclaimer

This article is prepared by Mason Stevens Limited (Mason Stevens) ABN 91 141 447 207 AFSL 351578 and is general advice only and does not take into consideration yours or your client’s personal objectives, financial circumstances or needs and should not be relied upon as personal advice. You should consider this information, along with all of your other investments and strategies when assessing the appropriateness of the information to your individual circumstances. Securities, by nature, rise and fall and as a result investing in securities including derivatives involve risk. Past performance is not a reliable indicator of future performance and may not be achieved in the future. Mason Stevens and its associates and their respective directors and other staff each declare that they may hold interests in securities and/or earn fees or other benefits from transactions arising as a result of information contained in this article.

Mason Stevens ensures that the information provided is accurate and complete but does not warrant its accuracy or reliability. Opinions and or information may change without notice and Mason Stevens is not obliged to update you if the informationchanges. Mason Stevens and its associated companies, authorised representatives, agents and employees exclude to the full extent by law, liability of whatever kind, including negligence, contract, fiduciary duties or otherwise, to investors or anyone else in respect of any loss or damage, including indirect or consequential loss or damage, foreseeable or not, arising from or in connection with this information.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

4 topics

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Marcus Tuck

Head of Equities

Mason Stevens

Responsible for identifying domestic and international equity investment opportunities. 25 years of financial markets experience as an equity strategist, economist, analyst, portfolio manager and consultant.

Expertise

Comments

Comments

Sign In or Join Free to comment