A slippery slope for the Australian dollar?

The Australian dollar / US dollar cross was something of a one-way trade in 2018. After appreciating to slightly above US$0.80 in January, the exchange rate deteriorated steadily for the remainder of the year. On 2 January 2019, the rate finally breached the US$0.70 level. In this paper we examine what’s been behind the move and, more importantly, what it might mean for Australia in the future.

Now trading in the late US$0.6…s, the Australian dollar is at its weakest level relative to the ‘greenback’ for three years. In January 2016, the rate troughed at US$0.686. Technical analysts have suggested the pair might re-test these lows now that the US$0.70 level has been breached. If so, the ‘Aussie’ will be in rarely charted waters; the currency has not traded lower against the US dollar since early 2009.

Why the weakness?

Theory suggests currencies fluctuate primarily according to countries’ relative economic fundamentals and interest rate differentials. In reality, the inter-connectedness of the global economy means there are many more forces at play. This helps explain why the Australian dollar was so weak in 2018, even though the economy saw its 27th year of unbroken growth. The latest data suggests Australian GDP growth is tracking at an annual pace of nearly 3%; hardly the sort of conditions that would be expected to see a currency depreciate so significantly.

Moves in the Australian dollar / US dollar cross appear more attributable to developments in the US, where growth has been accelerating steadily for most of the past three years. Fuelled by government stimulus, the US economy has rarely been in better shape. More than two million jobs were created in the US in 2018, pushing the unemployment rate down to its lowest level in nearly 50 years. The manufacturing sector is also performing well, arguably buoyed by corporate tax cuts last year and the introduction of tariffs that have made imported goods more expensive.

The favourable economic backdrop and tightening labour market in the US are seeing wage growth pick up. On average, American workers are enjoying wage growth of more than 3% a year – the highest level in nearly a decade. This is helping to push inflation higher, in turn prompting the Federal Reserve to raise US interest rates four times in 2018. In fact the Federal Funds rate has been raised eight times since mid-2016; Australian interest rates have remained unchanged over the same period.

At the same time, Australian inflation has been moderating – the 1.9% annual rate reported for the September quarter was a slowdown from earlier in the year. Against this background it appears unlikely that the Reserve Bank of Australia will raise interest rates in 2019, while further hikes are anticipated in the US. Comments from Federal Reserve officials suggesting US monetary policy will continue to be tightened this year supported the US dollar towards the end of 2018 and helped push the Australian dollar below the US$0.70 threshold in early January. Essentially, global investors continue to allocate money into US assets in the pursuit of higher returns. The US dollar also tends to be seen as a ‘safe-haven’ currency, further enhancing its appeal given recent market volatility.

How has the ‘Aussie’ performed on a trade-weighted basis?

It’s important to note that the Australian dollar was not alone in weakening against the US dollar in 2018. The ‘greenback’ appreciated against most major currencies over the year, including the euro, sterling and Chinese yuan. With this in mind, it’s worth monitoring how the ‘Aussie’ has performed against other peers.

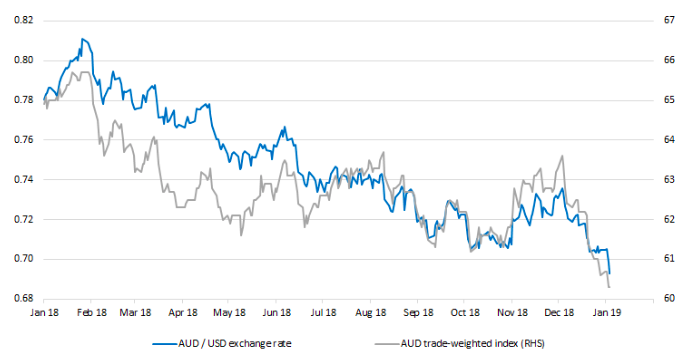

In the chart below, the blue line shows the performance of the Australian dollar relative to the US dollar; tracking the move from above US$0.80 to below US$0.70. The grey line shows Australia’s trade weighted index – the weighted average performance of the Australian dollar against the currencies of its trading partners. Interestingly, the Australian dollar has been just as weak against a basket of other currencies as it has against the US dollar.

The ‘Aussie’ has been weak on a trade-weighted basis, not just against the US dollar

Source: Bloomberg, 1 January 2018 to 3 January 2019

This suggests weakness against the US dollar cannot be entirely attributed by strength in the US economy and the higher Federal Funds rate. Other forces appear to be at play too.

In the second half of 2018, the Australian dollar may have been hampered by perceived links to China. The Chinese economy and its currency, the yuan, also came under pressure as the US introduced tariffs on goods imported from China. While not directly affected by the tariffs on Chinese goods, the Australian dollar appeared to sell off reflecting the importance of China as a trading partner. More broadly, the Australian dollar is perceived among traders to be a ‘commodity currency’ and, as a result, a proxy for global growth. The currency was therefore marked lower as the introduction of import tariffs – and the threat of more in the future – prompted global growth forecasts to be lowered.

Political instability has also done little to support the Australian dollar, given the recent change in Prime Minister and the likelihood of a Federal Election within the next six months.

What does this mean for Australians and local businesses?

A weaker currency is typically bad news for companies whose costs are partially denominated in other currencies – manufacturers, for example, that source raw materials from abroad and pay for them in local currencies. These higher input costs cannot always be passed on to consumers, resulting in margin erosion and, potentially, lower profitability.

A depreciation in the Australian dollar is not bad news for everybody in Australia. While international travel becomes more expensive for Australians, the weaker currency will likely increase the appeal of Australia as a destination for visitors from overseas. Australia has welcomed more than nine million international visitors over the past 12 months, boosting the economy by well over $40 billion. The prospect of more expensive overseas trips might also encourage more Australians to take holidays at home, providing further support to the domestic tourism industry. Similarly, the lower dollar makes Australia a more cost-effective location for international students. More than half a million overseas students are already enrolled at Australian colleges and universities; an influx that is estimated to contribute more than $30 billion annually to the economy.

A lower Australian dollar can help support other areas of the economy too, particularly manufacturers and other exporters. A weaker currency makes Australian exports cheaper and therefore more competitive globally. This improves the prospects for individual companies that export goods overseas and might potentially improve Australia’s trade balance, which in turn should help to support the currency. Over time, a more buoyant manufacturing sector should support the economy through higher employment, in turn boosting consumer spending and services sectors in general. Given the likelihood of resulting inflation, Australian interest rates could then be raised; thereby improving the appeal of Australia as an investment destination and further supporting the currency. It’s a cycle. Recent currency weakness will not persist indefinitely, though for now it is difficult to know where the dollar will find support.

What are the implications for funds?

Many funds that invest in overseas assets are hedged against currency fluctuations. Movements in the Australian dollar – either positive or negative – do not influence returns as the hedging arrangements that are in place effectively counteract any movement in underlying exchange rates. For funds that are unhedged, weakness in the Australian dollar will boost returns from overseas assets, and vice versa.

The ‘Aussie’ can act as a return volatility hedging mechanism for Australian investors. Typically, as prospects for the global economy deteriorate, and global equity returns fall, the Australian dollar will weaken – helping to offset those negative returns for Australian-based investors. This was highlighted in the December quarter and in 2018 as a whole.

The MSCI World Index fell -13.3% over the December quarter and -8.2% in 2018, both in US dollar terms. These were the worst December quarter and calendar year returns for global equities since the Global Financial Crisis. Yet in Australian dollar terms, the MSCI World Index fell -11.0% in the December quarter and actually rose 1.8% over the year. Still disappointing, but not as savage as the negative returns for US investors.

Further, some of our diversified fixed income and multi-asset portfolios utilise active currency positioning. In these cases, funds can be deliberately positioned to capture expected movements in exchange rates. Depending on the portfolio we can establish positions in one currency versus another, or implement long or short positions in currencies individually. A degree of currency volatility can therefore be desirable for these funds, as it presents opportunities to improve overall returns through active management.

Want to learn more?

A series of regular news updates, research papers, investment strategy updates and thought pieces from some of Colonial First State Global Asset Management's leading experts can be found here

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

First Sentier Investors is a global asset management group focused on providing high quality, long-term investment capabilities to clients. We bring together teams of active, specialist investors who share a common commitment to responsible investment principles.

We are a stand-alone asset management business and the home of investment teams AlbaCore Capital Group, FSSA Investment Managers, Igneo Infrastructure Partners, RQI Investors and Stewart Investors. All our investment teams – whether in-house or individually branded – operate with discrete investment autonomy, according to their investment philosophies.

First Sentier Investors

First Sentier Investors is a global asset management group focused on providing high quality, long-term investment capabilities to clients. We bring together teams of active, specialist investors who share a common commitment to responsible...

First Sentier Investors

First Sentier Investors is a global asset management group focused on providing high quality, long-term investment capabilities to clients. We bring together teams of active, specialist investors who share a common commitment to responsible...

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

High conviction: What we’re backing for the long term

Livewire Markets