Addressing the ‘franking credit dilemma’: Is bank subordinated bank debt the answer? Possibly!

Labor’s proposed tax changes could result in investors experiencing a decline in income as many may be unable to redeem surplus franking credits. For such investors holding bank hybrids it is tempting to consider that shifting to bank subordinated debt may be the answer. But is this really the case?

What is the ‘franking credit dilemma’?

The ‘franking credit dilemma’ refers to the issue of how to replace the income lost in the event investors are unable to make full use of franking credits due to Labor’s proposed tax changes i.e. many investors will be prevented from redeeming surplus franking credits. For such investors franking credits beyond a certain level will become less attractive and they will increasingly look for other higher yielding non-franked investments to make up any income shortfall.

So what is the alternative? Subordinated debt?

It is tempting to consider that bank subordinated debt (‘sub-debt’) could be a viable higher yielding alternative to hybrids as they are often viewed as exhibiting the same risk characteristics. Unfortunately, this is not currently the case. A typical hybrid issued by the major banks trades at a margin of around 3.70% over bank bill (including franking credits) and 2.00% over bank bill (excluding franking credits). In contrast major bank sub-debt trades at around 2.00% over bank bill. With bank sub-debt trading in line with the yield on hybrids (excluding franking credits) at first glance they cannot offset the decline in income.

The reason for the difference in yields is due to two key factors:

Firstly, at a fundamental level sub-debt exhibits lower risk characteristics than hybrids and so should, all else being equal, trade at a lower yield. To understand the difference in risk characteristics it is necessary to distinguish between banks as a ‘gone concern’ as opposed to a ‘going concern’. In a default situation, or ‘gone concern’ situation, both hybrids, as additional (or alternative) tier 1 capital, and sub-debt, as tier 2 capital, rank equally and so exhibit the same risk characteristics; i.e. absorb losses on a ‘gone concern’ basis. However, hybrids are higher risk as, unlike bank sub-debt, they can be converted by the regulator in the absence of a default, if the regulator views that conversion is necessary to ensure the bank remains a ‘going concern’.

Secondly, at a technical level the bank sub-debt market is currently an institutional market with yields being compressed by the current strong demand for higher yielding investments.

Both these factors create fundamental and technical reasons why sub-debt currently trade at a lower margin to hybrids.

But the environment may be changing

The dynamics driving the technical factors may however be changing due to developments arising from changes in the regulatory environment (set out in the Australian Prudential Regulatory Authority (‘APRA’) discussion paper on “Increasing the loss-absorbing capability of ADI’s to support orderly resolution” released in November 2018).

At a high level the discussion paper sets out a framework establishing the capital requirements deemed necessary to facilitate the orderly resolution of Australian authorised deposit-taking institutions (‘ADIs') while minimising the need for taxpayer support. The key conclusions reached are that :

- A new requirement for ADI’s to maintain additional loss absorbency for resolution purposes.

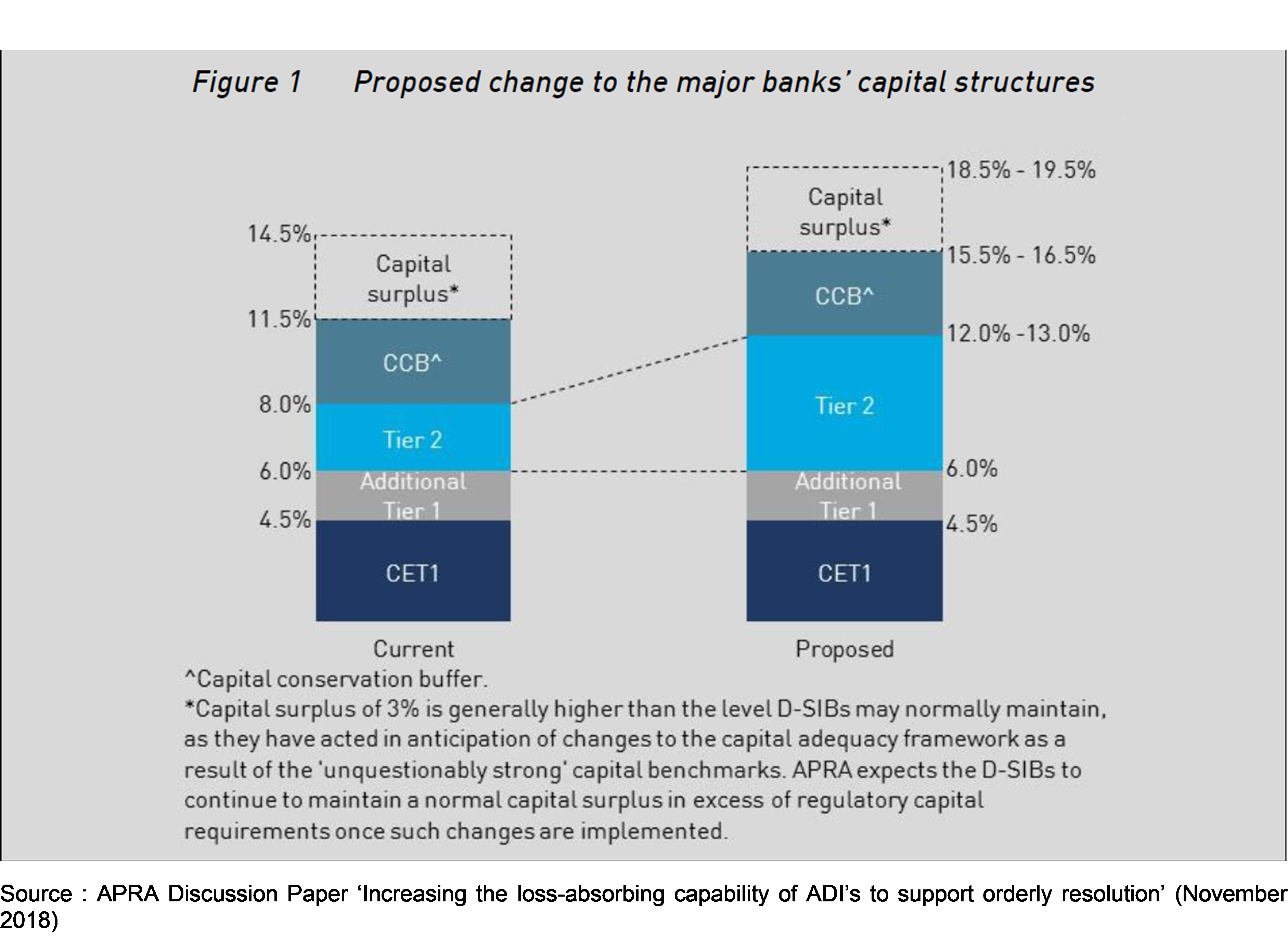

- For domestic systematically important banks ('D-SIBs') to increase total capital by around 5% over the next 4 years; i.e. increase in total capital ratio from 14% to 18.5%-19.5%.

A schematic of the new proposed capital structure for D-SIBs is shown below (Figure 1):

The key implications from the proposed changes to major bank capital structures are :

- Tier 2 capital is the preferred source of additional loss absorbency for resolution purposes.

- Places Australian senior bonds at an advantage over global peers where the regulators count the issuance of senior bonds as ‘bail-in-able’ instruments.

- No indication that banks can use tier 3 capital (basically shorter dated sub-debt) though this may change after feedback from the banks.

- Material increases in the issuance of tier 2 capital (around $60+bn) by the four major banks over the 4 years following the new capital requirements becoming effective.

With the potential that the tax treatment of franking credits may be revised, the proposed changes to bank capital structures becomes particularly timely and relevant. The key reason is that the new capital structures require the major banks to materially increase the level of sub-debt (whether in the form of tier 2 or tier 3 capital) over a defined period. Given the required increase in sub-debt it is highly likely that banks will seek a broader range of issuance channels so as not to be overly reliant on any one market. This raises the potential that the banks may seek to develop a retail market for sub-debt. If the development of a retail market eventuates then the issuance yields for sub-debt debt are likely to be materially higher than the yields currently accepted by the institutional market i.e. closer to current hybrid yields including franking credits. Therefore, while at current yields sub-debt cannot make up the franking credit income shortfall, the evolution of the market may yet assist in closing the yield gap*.

Though a lot of the dynamics discussed are longer term in nature, post 2020, the current evidence suggests that there are reasons to believe that sub-debt will not be issued at the same effective yield as hybrids. This does not mean that the current yield differential may not close providing investors with a more attractive yield while remaining below that of hybrids. While bank sub-debt yields may not rise high enough to fully offset the income decline from changes in the dividend imputation rules they may yet provide part of the answer investors are looking for. What is also clear, if history is any guide, the financial markets are dynamic and if there is a strong demand for high yielding unfranked securities as an alternative to hybrids, then the market is likely to respond in one way or another.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

By

Clive Smith,

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance degrees from Macquarie University and is a CFA ® charterholder.

3 topics

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Clive Smith is an investment professional with over 35 years experience at a senior level across domestic and global public and private fixed income markets. Clive holds a Bachelor of Economics, Master of Economics and Master of Applied Finance...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Equities

What a 40% year taught us: 4 lessons from the past 12 months (and 3 new stocks to buy)

Seneca Financial Solutions

Equities

How to invest $100k for growth

Livewire Markets