LWE - 14th Nov, 2020

Afterpay – buy now, pain later?

Afterpay has been a sharemarket darling, with its share price rising almost tenfold over the past two years alone. The price has fallen a little since starting this article, but market consensus remains optimistic. To us, however, the risks seem heavily skewed to the downside. We explore Afterpay’s attractiveness, or lack of it, from a long-term investment perspective below.

Afterpay is a buy-now-pay-later facilitator which allows its users to split the cost of purchases into four equal two-weekly instalments over six weeks (with the first instalment paid at the time of purchase). It does not charge its users interest, caps late fees and pauses accounts when customers miss a payment. Its revenue is derived by charging retailers a percentage of the merchant sales facilitated by Afterpay.

Let’s start with some numbers

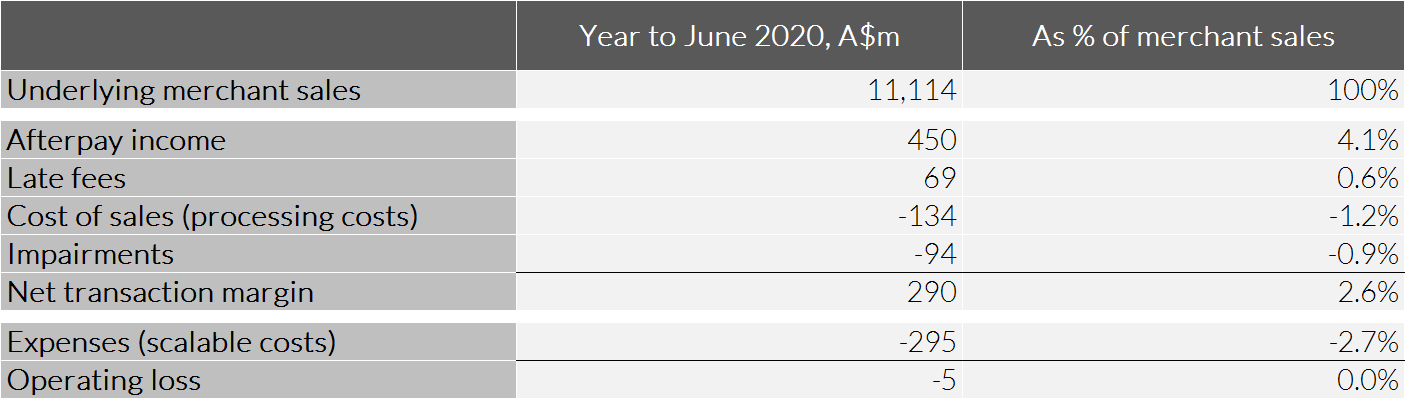

Afterpay’s business is best understood with reference to its unit economics. The table below shows its 2020 annual result with reference to its underlying merchant sales.

Source: Afterpay Annual Report 2020

For the year ended 30 June 2020, A$11.1 billion of merchant sales were facilitated by Afterpay. On average, retailers were charged 4.1% of merchant sales, the company made a further 0.6% of merchant sales on late fees and incurred non-scalable processing costs totalling 1.2% of merchant sales. Effectively an unsecured short-term lender, it is unsurprising that it incurred bad debts of 0.9% of merchant sales in 2020. The net of all these amounts is what Afterpay calls its net transaction margin (NTM) which was A$290m in 2020 or 2.6% of merchant sales. It targets an NTM of greater than 2%.

Below this NTM are almost $300m in annual costs dedicated to business development, head office costs, IT development and so on. These costs are scalable and whilst currently above the dollar NTM (rendering the company unprofitable), these costs are reasonably expected to rise more slowly than NTM. Afterpay will therefore become profitable and move to fund its growth (or a portion of its growth) through earnings retention rather than equity issuance. Not reflected in the table above is $22m of interest costs in 2020. For now we’ll ignore these costs and give Afterpay the benefit of the doubt, but it seems reasonable to reduce the NTM by the effective 0.2% of merchant sales.

What might a mature Afterpay look like?

At over A$100 per share recently, Afterpay had a market capitalisation of approximately A$30 billion. Recent share price weakness has reduced this somewhat.

In years to come Afterpay should eventually become a mature business, having fully penetrated its user base and targeted geographies. Once Afterpay’s extraordinary growth has plateaued, a mature Afterpay should be as cyclical as any other short-term money lender. Its fortunes will rise and fall with the economic cycle that already sees retail spending (upon which it relies heavily) and bad and doubtful debts fluctuate.

One does not have to look much further than the world’s banking sector to realise that companies like these trade at much lower than 10 times ‘normal’ pre-tax profits. You could argue that a mature Afterpay should not trade at a multiple this high. Its loan book is completely unsecured (as distinct from the banking sector which has significant security over its loan book) and its business would contract rapidly during economic downturns (its loan book has six weeks’ duration at inception, versus a bank’s which often extends into decades). But again, giving Afterpay the benefit of the doubt, let’s assume 10 times is reasonable.

If today’s price is reasonable, a mature Afterpay will need to earn $3 billion in pre-tax profits.

Using this level of profitability and the unit economics detailed above, it is possible to calculate what underlying merchant sales Afterpay will need to achieve. First we need to make three important assumptions:

- that the current NTM of approximately 2.5% is sustainable, and

- that Afterpay’s scalable cost base will only grow by half of the dollar transaction margin growth, and

- that no additional capital will be required to fund future growth.

The first of these assumptions seems generous – not only is their target “above 2%”, there are a host of reasons why even that might be optimistic. But we’ll get to that later. With respect to the cost growth assumption, Mastercard is a useful comparator. Between 2001 and 2019, its revenues grew tenfold and its costs grew fivefold. Mastercard is not unique. The world’s best compounders grow their costs at approximately 50% of revenue growth. This assumption assumes Afterpay rubs shoulders with the best of them. The third assumption is just plain unrealistic, but given that it helps the Afterpay thesis, we’ll ignore this for now.

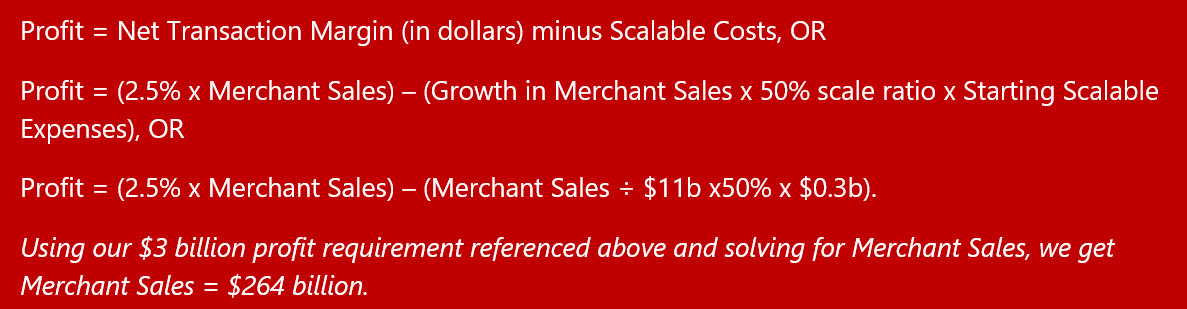

We can calculate the sales required for Afterpay to make $3 billion in pre-tax profits by using a formula for profit as follows:

Said differently, in order for Afterpay to make $3 billion in annual pre-tax profit, and assuming our assumptions hold true, merchant sales would need to be A$264 billion per annum. At a little over 20 times 2020’s merchant sales and taking into account their 112% growth in 2020 alone, this would be achieved in four and a half years.

To determine how likely this is, we first need to assess its addressable market.

How large is Afterpay’s addressable market?

In order to determine Afterpay’s addressable market, we could first focus on its home market, Australia. In Australia, retail sales were A$342 billion for the 12 months to September 2020 . A significant part of this is from food retailing (e.g. Coles, Woolworths, IGA, etc.), cafés, restaurants and takeaway food services which doesn’t form part of Afterpay’s addressable market (that is unless we’re moving towards a society that pays off our coffee in four instalments). Stripping these amounts out, in Australia, Afterpay’s addressable retail spend was $104 billion for the 12 months to September 2020. In Australia, Afterpay’s share of this market was 6% in 2020 (59% of Afterpay’s $11.2 billion merchant sales were in Australia).

Of course Afterpay is not just an Australian-focused company. But it is useful to use its Australian addressable market to infer the total addressable market from the geographies in which it is seeking to grow. In Australia, Afterpay’s addressable market represents approximately 5% of gross domestic product ($104 billion in retail sales and close to $2 trillion in GDP). Assuming the same is true for the countries in which Afterpay is currently expanding, it is possible to arrive at its total merchant sales addressable market.

The combined GDP of the United States, Australia, United Kingdom, Canada, Spain, France, Italy and Portugal was US$33.7 trillion in 2019 (and likely lower in 2020). Assuming the same 5% addressable market share, Afterpay’s addressable market would be US$1.7 trillion or about A$2.4 trillion in merchant sales.

In the previous section we calculated that a mature Afterpay would require A$264 billion in merchant sales to warrant its current valuation. This is 11% of the addressable market we’ve calculated above.

Is this achievable?

In 2019, the global addressable market (ex-China) for Consumer-to-Business (C2B) purchases was US$33 trillion. 53% of this was from non-cards (mostly cash and cheques), 26% Visa (credit and debit), 14% Mastercard, 4% Amex, and 3% the remaining card networks (other networks and domestic schemes that are not at least Visa or Mastercard co-branded). So 11% market share in Afterpay’s addressable market is three times Amex’s current share and close to Mastercard’s market share today. It is less than half of Visa’s market share.

Before determining whether this market share is achievable, it is worth noting that Afterpay’s addressable market is a subset of the incumbent card companies.

New customers are limited by how much they can spend in any given transaction on Afterpay. Seasoned account holders with excellent payment histories are also limited, albeit at a larger transaction size. The same is not true for Visa and Mastercard, where the issuing bank sets the credit limit and it is usually several thousand dollars, often much more. Consequently, there are likely trillions of dollars of transactions which are greater than Afterpay’s permissible level, but well within reach of Visa and Mastercard customers.

We don’t have good data on the distribution of retail purchases by value, but it is likely that Afterpay’s $264 billion in merchant sales would put its share well above Mastercard’s and possibly even towards or greater than Visa’s. This seems like a very tall order, but it is certainly possible.

Opportunities and challenges

The proponents might reasonably argue that the above does not factor in any Afterpay success in Asia or South America. That’s true, the analysis above has only covered North America, a large part of Europe and Australia. Also, history is littered with incumbents like Visa and Mastercard falling to the swords of minnows, like Afterpay is today. The same could happen again. Afterpay could expand into healthcare (like dentistry and cosmetic surgery) thereby significantly increasing its addressable market. Afterpay could capture a large share of the 53% C2B market (although in reality Afterpay’s user base has already shunned cash with ceded share more likely to gravitate to the incumbent card companies). Unit economics might improve rather than deteriorate. And of course, who’s to say that 10 times pre-tax profits is the right multiple for a mature but sexy company, what if we use 20 times?

But the road ahead is not without its challenges, some of which we list below:

- Capital – increasing merchant sales from A$11 billion (in 2020) to A$264 billion will require significant amounts of capital. Up to $30 billion of it ($253 billion increase in merchant sales multiplied by the funding cycle of six weeks out of 52 weeks). This could either be equity funded (as is mostly the case for Afterpay today) or debt funded. This is either very dilutive to existing shareholders today or it will require even greater merchant sales and market share than the $264 billion calculated above so as to absorb the interest costs and sustain the $3 billion pre-tax profit. As it is, $22m of interest costs in 2020 have been completely ignored in Afterpay’s unit economics above which could reasonably reduce the NTM to below 2.5% already!

-

Competition – a competitive response from incumbents and other BNPL companies will likely reduce Afterpay’s NTM.

-

Bad debts – it’s unlikely that Afterpay could increase its loan book from the current A$800m to over $30 billion without an increase in risk and, ultimately, bad debts and impairments. This too would reduce NTM to something closer to or below its own 2% target.

-

Regulation – it’s not clear that Afterpay’s costs will scale as well as we’ve assumed given the increased regulatory oversight its success might attract. This is certainly true of banks, which spend vast and seemingly unscalable sums on responsible lending and anti-money laundering initiatives.

-

Changing preferences and behaviours – it is dangerous to analyse future outcomes in a bubble. As a retailer’s sales become increasingly skewed to Afterpay, their margins will likely fall. Pushing an extreme, if 100% of a retailer’s sales were facilitated by Afterpay, one could reasonably expect its margins to fall by 4.1% of sales (the same number used in the unit economics table above) less a much lesser percentage paid to the incumbent card companies. In many cases this would render the retailer unprofitable. For the best retailers, it would reduce profits by 50% or more. To give an example, Super Retail Group (a well-respected retailer in Australia and owner of the Rebel Sport, Macpac, Super Cheap Auto and the BCF network of stores) has retail margins less than 8%. We believe that with Afterpay’s success will come unintended outcomes which, pushed to extremes, can’t coexist with the strength of the retail networks and consumers upon which they rely.

-

Sensitivities – when you consider how sensitive our analysis is to the assumptions we’ve used, things begin to get very difficult. Relaxing the 2.5% NTM assumption to 2% alone results in Merchant Sales in the formula above equalling A$471 billion, roughly 20% market share. Or worse, when you assume that an extra $30 billion of capital is required and assume that is equity funded, suddenly the market capitalisation doubles, the required profit rises to $6 billion per annum and solving for Merchant Sales results in A$528 billion at a 2.5% NTM (22% share) and $940 billion at 2% NTM (39% share). Even worse when you further adjust for capital – as merchant sales rise above $264 billion, so does the $30 billion capital assumption, the required profit and resulting merchant sales.

-

Time – we haven’t factored in the time it might take to get to the $264b in merchant sales. All that while, you could instead hold a mature, self-funding company sustainably earning $3b in income and probably collecting a good dividend to boot. These ‘lost’ earnings would surely carry some opportunity cost were one to invest in Afterpay instead?

Conclusion

We can see an upside from a long-term investment in Afterpay. But it would take world domination and the toppling of massive incumbents who are unlikely to watch from the sidelines. And even then a long-term investment in Afterpay today might just be okay and nowhere near as high returning as investors have enjoyed over recent years. To us, the risks seem heavily skewed to the downside.

Want to learn more?

Contrarian investing is not for everyone, however there can be rewards for the patient investor who embraces Allan Gray’s approach. Visit the Allan Gray Australia Equity Fund profile to find out more.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan Gray in 2006 as an analyst, bringing with him a strong background in finance from previous roles at Alliance Bernstein, Macquarie Bank, and Deloitte & Touche. Simon holds a Bachelor of Business Science (First Class Honours) in Finance and Business Strategy, along with a Postgraduate Diploma in Accounting, from the University of Cape Town. He was a Chartered Accountant and is a CFA Charterholder. Known for his contrarian, long-term, value-driven investment philosophy, Simon speaks frequently at industry events and appears in media interviews, offering perspectives on specific securities, as well as portfolio positioning and the Allan Gray contrarian investment strategy.

Featuring

Simon Mawhinney,

Allan Gray

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan Gray in 2006 as an analyst, bringing with him a strong background in finance from previous roles at Alliance Bernstein, Macquarie Bank, and Deloitte & Touche. Simon holds a Bachelor of Business Science (First Class Honours) in Finance and Business Strategy, along with a Postgraduate Diploma in Accounting, from the University of Cape Town. He was a Chartered Accountant and is a CFA Charterholder. Known for his contrarian, long-term, value-driven investment philosophy, Simon speaks frequently at industry events and appears in media interviews, offering perspectives on specific securities, as well as portfolio positioning and the Allan Gray contrarian investment strategy.

........

Past performance is not a reliable indicator of future performance. There are risks involved with investing and the value of your investments, including in the Allan Gray Funds, may fall as well as rise. This article represents Allan Gray's view at a point in time and may provide reasoning or rationale on why we bought or sold a particular security for the Allan Gray Funds or our clients. We may take the opposite view/position from that stated, as our view may change. This article constitutes general advice or information only and not personal financial product, tax, legal, or investment advice. It does not take into account the specific investment objectives, financial situation or individual needs of any particular person and may not be appropriate for you. Before deciding to acquire an interest in any financial product or making any other investment decision, please read the relevant disclosure document. We have tried to ensure that the information in this article is accurate in all material respects, but cannot guarantee that it is.

1 stock mentioned

1 fund mentioned

Simon Mawhinney is the Managing Director and Chief Investment Officer of Allan Gray Australia, where he leads the company’s investment strategy and oversees the performance of its Australian equity and multi-asset portfolios. Simon joined Allan...

Expertise

Comments

Comments

Sign In or Join Free to comment