Aged care under royal pressure

Historically, our view has been that there is a supply and demand imbalance in the aged care sector, with the lack of supply and rising demand only going to be exaggerated over the next few years as the bulge bracket of the Australian population moves deeper into retirement. The proportion of people aged 65 years or over in the total population projected to increase from 15.3% in 2017 to 21.8 per cent in 2056.*

We therefore share the view that the potential for the aged sector is very good. However, the sector’s reliance on government spending and the associated regulatory risk makes it a difficult sector to pick at the corporate level. In 2016/17 governments spent about $17 billion on aged care, with 69% of this going towards residential aged care.** The vast majority of this funding comes from Federal Government.

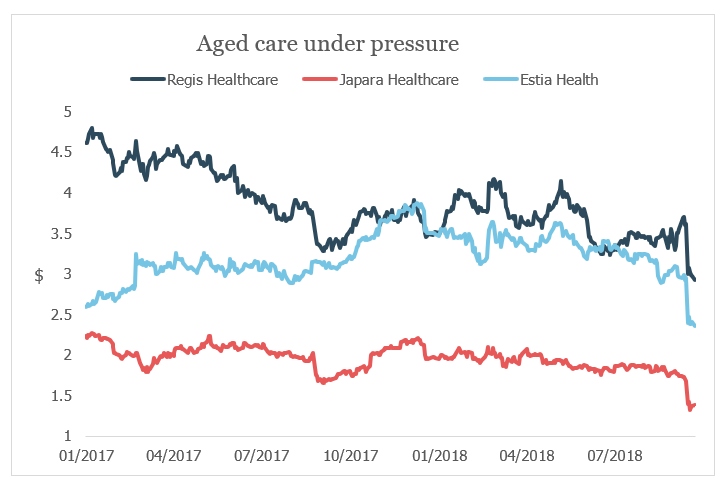

Companies like Regis Healthcare, Japara Healthcare and Estia Health are heavily regulated businesses and run off largely government-mandated revenues. When these stocks originally listed, investors preferred to concentrate on the top line market growth rather than the regulatory risk – the funding for residential care has risen from $9.7 billion in 2011/12 to $12.1 billion in 2016/17.*** Investors predicted that the increasing public spending, plus the supply and demand imbalance, would continue to drive valuations in the sector, and therefore put the stocks on significant premiums to the broader market.

However, the regulatory risks have come back to bite them. About 96% of government spending comes from the Federal Government. By some estimates, the cost to the budget of delivering aged care is set to eclipse the entire cost of Medicare by 2031-32. **** It would be silly to think that such a drain on the government coffers would not warrant more attention as to service levels, and therefore corporate costs.

The Federal Government is looking to pull back on spending, claiming it will not be able to afford this level of growth in the future. This has affected the valuations of the corporate players in the sector – even before the royal commission into the aged care sector was announced earlier this month.

"It is difficult to tell what providers may receive the largest dressing down in the commission and what that will mean for confidence levels."

As anyone with experience of the financial services royal commission will bet, there is a good chance that this new commission will look into stories about the mistreatment of clients and poor management. This will affect the reputations of the companies in the sector, when the sector is dependent on clients and their families being able to trust providers to do one of the most personal (and difficult to track) jobs – looking after older Australians. It is difficult to tell what providers may receive the largest dressing down in the commission and what that will mean for confidence levels (hence why all the major players were hit after the commission’s announcement).

Over the longer run – no matter the outcome from the royal commission - we will see the government refusing to increase what it pays the sector to the same extent as it has had in the past. In such an environment it is difficult to see how the sector earns a positive return, particularly when there will be pressure to increase staffing levels and improve facilities.

However, the royal commission may find that funding has to be increased to deal with the increased demand for beds as the baby boomers enter their 80s. If that is the outcome that happens, then it actually will be positive for the industry. But look at what the insiders are doing. In the past 12 to 24 months Regis, Japara and Estia’s acquisitions have been diversifying them away from aged care into retirement villages. This reduces their risk in the midst of aged care funding changes, but they have had to pay top dollar for these retirement village development opportunities as house prices in Sydney and Melbourne peak.

Is there a buying opportunity in the aged care space? Yes, potentially, over the longer term. But the fact is that the underlying fundamentals of the sector will not continue to grow to the same extent as they have, as the government pulls in the reins.

Uday Cheruvu

Portfolio Manager, PM Capital Australian Companies Fund.

** (VIEW LINK)

*** (VIEW LINK)

**** (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

At PM Capital we are not afraid to be different, we search the world for undervalued stocks, we avoid the trap of “group think” and prioritise company valuation over all other aspects. Founded in 1998, PM Capital is part of the Regal Partners Limited stable of alternative asset managers and specialise in Global & Australian equities and Global Fixed Interest strategies. We believe the very best way to minimise investment risk is through understanding valuation, as such, we avoid companies who are hard to understand or difficult to value and are well known for our discipline in resisting short term market noise and ability to hold investments through full industry cycles.

3 topics

PM Capital

At PM Capital we are not afraid to be different, we search the world for undervalued stocks, we avoid the trap of “group think” and prioritise company valuation over all other aspects. Founded in 1998, PM Capital is part of the Regal Partners...

Expertise

PM Capital

At PM Capital we are not afraid to be different, we search the world for undervalued stocks, we avoid the trap of “group think” and prioritise company valuation over all other aspects. Founded in 1998, PM Capital is part of the Regal Partners...

Expertise

Comments

Comments

Sign In or Join Free to comment