Anatomy of the fall (an update)

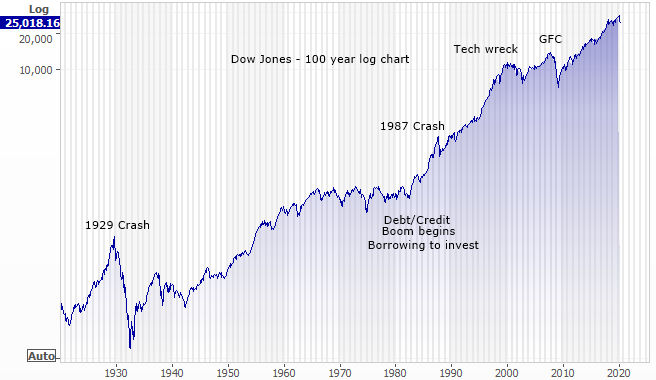

You are supposed to use a log scale on a share price chart if looking at charts over a long period of time. The basic explanation is that a log chart shows two equivalent percentage price changes represented by the same vertical distance on the scale and to accommodate that the distance between the numbers on the scale decreases as the price of the asset increases.

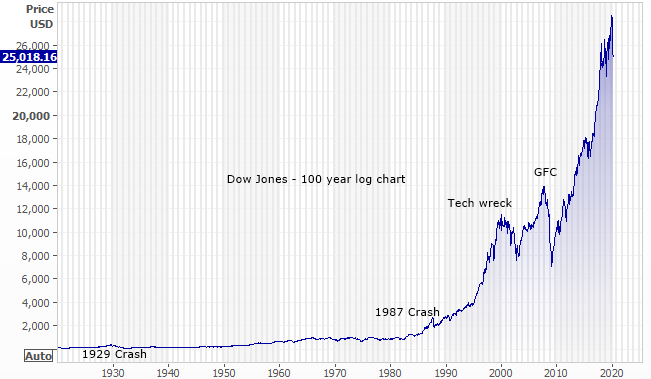

I read one article this morning talking about the ‘Historic’ coronavirus correction. This is a 100-year chart of the Dow Jones using a normal price scale. The 1929 Crash and the 1987 Crash, because they were so long ago when the index was just a few hundred points, are now considered, on this chart, irrelevant.

But if you lived through 1929 or 1987 they were not irrelevant, they were disastrous. To illustrate that you use a log chart. Here is the same chart using a log scale. Suddenly the 1929 Crash and the 1987 Crash are in perspective to how devasting it was. And suddenly the Coronavirus Correction is in perspective.

Sorry, but the ‘Coronavirus Correction’ is hardly historic. Not yet anyway….

ANATOMY OF THE FALL

I wrote an article at the beginning of last week called the “Anatomy of the Bounce” which included a look at the stocks that had fallen the most and were (presumably) likely to bounce the most on a relief rally.

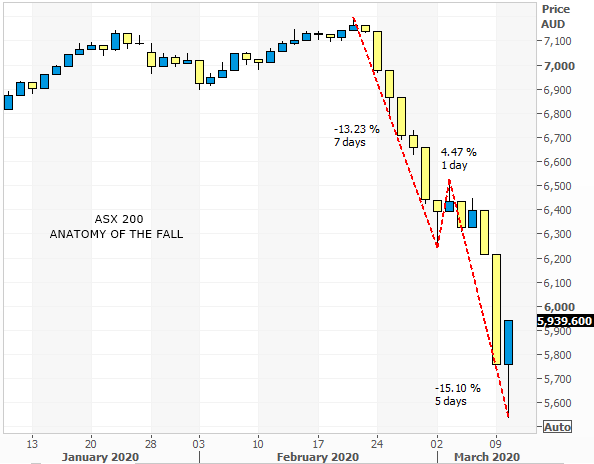

At the time the ASX 200 had dropped 13.23% from top to bottom and was clearly about to bounce. It bounced 4.47% from the low that day to the top the next day. Since then it has fallen another 15.10% to yesterday’s low.

As of Trump’s speech yesterday the markets have bounced for the second time in this correction. He has belittled the coronavirus saying 25,000 to 70,000 people die in the US from influenza every year and the country’s infrastructure doesn’t have to grind to a halt because of it, so why now for a few hundred cases. His speech started to turn things glass half full. When he started speaking our market rallied 7.23% from the low yesterday to the high yesterday.

With a little bit of optimism we start focusing on the better news. Things start to look more glass half full for the first time in three weeks. The cases in China have (apparently) peaked and fallen, Xi is brave enough to visit Wuhan, and the publication of the mortality rates so far suggest the problem is minor for those without pre-existing medical conditions that are under 70.

And the US market rallied 5.5% from its low the day before to the close last night.

Here is the anatomy of the fall using daily candles on the ASX 200:

PERSONAL OPINION

Personal opinion (guesswork) is that we have a typical “Trump” inspired moment of groundless confidence, another moment of hollow market manipulation. And that’s the depth of this bounce. Its hollow, its short term and its not fundamental.

Looking at the real news we have the Qantas impact, the oil war, Italy closed (a whole country closed). And we have a host of downgrades in the pipeline. They’re coming. BHP have told us they are coming.

BHP said in its recent results statement “For 12 months ahead, we assess directional risks to prices across our portfolio are mixed, with the coronavirus outbreak a major source of uncertainty” – “If this viral outbreak is not demonstrably well contained within the March quarter, we expect to revise expectations for economic and commodity demand growth downwards”. BHP is warning us that it is cum a profit warning if coronavirus doesn’t disappear by the end of this Q (it hasn’t). And if BHP is on alert you can imagine the earnings issues for other companies that are more directly exposed.

There are hundreds of companies globally that are yet to publish specific COVID-19 affected earnings guidance, and in Australia we can expect a rash of earnings downgrades as companies get to the end of March and confess to the impact. Downgrades are in the pipeline not just in the travel, tourism, education and cyclical sectors, but in the US, Europe and the rest of the world. Apple, German car manufacturers, its significant and unquantified, the extent of the profit cost is yet to be exposed.

Meanwhile, in Australia, since the results season all the research is brand new and up to date for the February results but is ‘coronavirus unaffected’. Its out of date already. At the moment, out of 417 stocks covered by broker research in Australia 286 are trading more than 10% below the average broker target price (over 10% 'cheap'). 94 are trading more than 30% below the average broker target price. Broker research generally does tend to be optimistic but this is out of whack - the research is behind reality and the earnings numbers and target prices need updating.

In which case this Trump bounce appears to be an injection of hollow confidence rather than the representation of a factual improvement in the coronavirus outlook. A real negative economic impact in the first Q is now ‘in the bag’, inevitable, the RBA and FOMC rate cuts make that clear, and the debate is not about blind confidence it’s about how long and deep the economic damage ends up being beyond Q1. And that’s still an unknown. In which case any market buying today is speculative at best.

The Marcus Today Team (we run around $40 million of client funds) discussed selling into it this morning (we already have 56% cash and are definitely not buying yet) but decided we’d see if it could develop some momentum first, we are due a more material reversal than the last one.

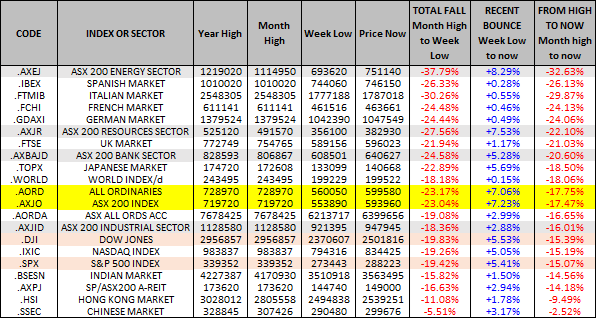

ANATOMY OF THE FALL

Here is a table showing the performance of the ALL ORDS and ASX 200 compared to other international markets in this correction. They are listed in order of worst falls first. The three right hand columns show:

- The fall from top to bottom.

- The size of the recent bounce.

- The fall from the high to now (after the bounce yesterday).

Australian sectors are in grey.

Observations:

- The Energy sector is in a world of sentimental hurt and is going to come ripping back one day. It bounced 8% yesterday, showing its recovery colours.

- Resources and banks have underperformed the rest of the market. Judging from the 7% rallies in Resources and Banks yesterday these two sectors are also going to bounce when the bounce comes.

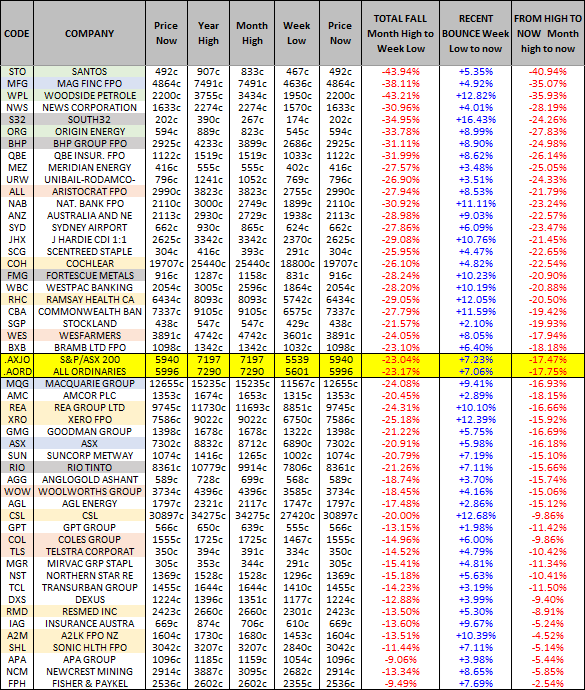

STOCKS TO BUY FOR A BOUNCE

(if you are so inclined – we aren’t yet)

For those that want to buy something here is an update of the WHAT TO BUY IF YOU WANT TO BUY lists.

It highlights the stocks that have fallen the most and (mindlessly) suggests that these are the stocks that will bounce the most when market sentiment improves which is did yesterday.

Again I have broken this down into the TOP 50, the NEXT 50 and the WORST OF THE REST. Again the three right hand columns show:

- The fall from top to bottom in this correction.

- The size of the recent bounce (yesterday’s bounce).

- The fall from the high to now.

The stocks are listed in order of worst performers since the recent highs first.

TOP 50

Observations – Stocks to buy for a bounce:

- Oil stocks the obvious stocks – STO, WPL, ORG

- Resources another bounceable sector – BHP, FMG, S32…to a lesser extent RIO (doesn’t own oil assets, BHP does).

- Stock Market Stocks – MFG, MQG, ASX

- Growth stocks – COH, ALL, RHC, REA, XRO, CSL

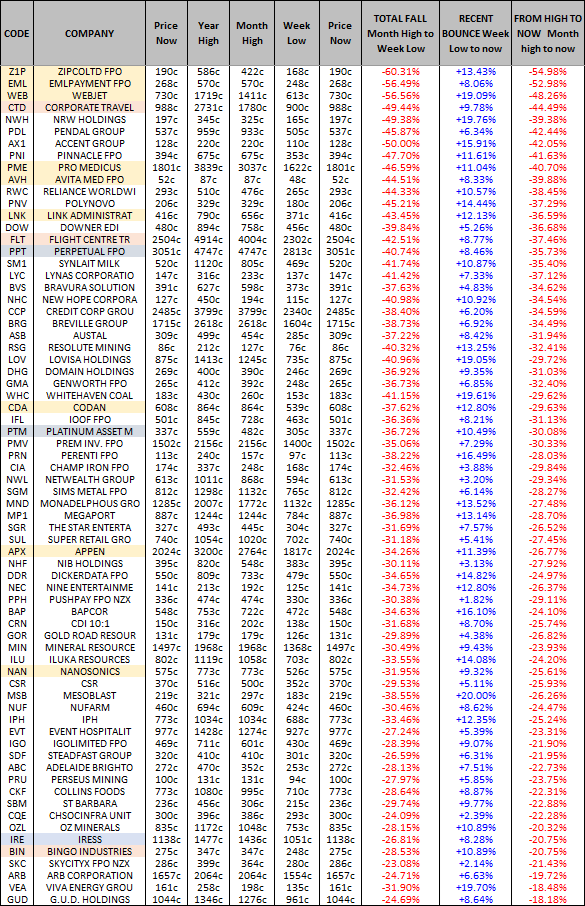

THE NEXT 50

Observations – Stocks to buy for a bounce:

- Growth stocks – WTC, ALU, IEL, APT

- Oil stocks – OSH, BPT, WOR

- Others – CPU, QAN, HVN, JBH

WORST OF THE REST

Observations – Stocks to buy for a bounce:

- Growth stocks – Z1P, EML, PME, AVH, APX, NAN

- Travel - WEB, CTD, FLT

- Stock market stocks – PPT, PTM

Read more from Marcus

Marcus Padley is the author of the Marcus Today stock market newsletter. To sign up for a 14-day free trial please click here.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and informing private investors with insightful, honest, straight-up independent stock market research and ideas. Marcus likes to call it as it is without agenda, puts subscribers first, and this has paid off for real people with real money.

1 topic

12 stocks mentioned

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Marcus Padley founded Marcus Today in 1998 and leads the team of analysts and market commentators that publishes a daily stock market newsletter, presents four podcasts and runs an $80m Australian equity fund. He is passionate about educating and...

Expertise

Comments

Comments

Sign In or Join Free to comment