APRA closes the Committed Liquidity Facility

Matthew Johnson

Coolabah Capital

In a move that's a bit more aggressive than I had expected, APRA just announced that they will close the CLF (Committed Liquidity Facility).

The CLF will be reduced in four equal steps (1 Jan'22 - $104 billion; 30 Apr'22 - $70 billion; 31 Aug'22 - $35 billion, and $0 on 31 Dec'22). In practice, the reduction is a bit more aggressive, as from 1 Jan 2022 the first 100% must come from genuine High-Quality Liquid Assets (HQLA). From that date, Australian Deposit-Taking Institutions (ADIs) will be required to hold sufficient HQLA to meet the regulatory 100% minimum Liquidity Coverage Ratio (LCR). They can use the remaining CLF for their buffers.

In a surprisingly strong letter, APRA says that they expect "ADIs to purchase the HQLA necessary to eliminate the need for the CLF."

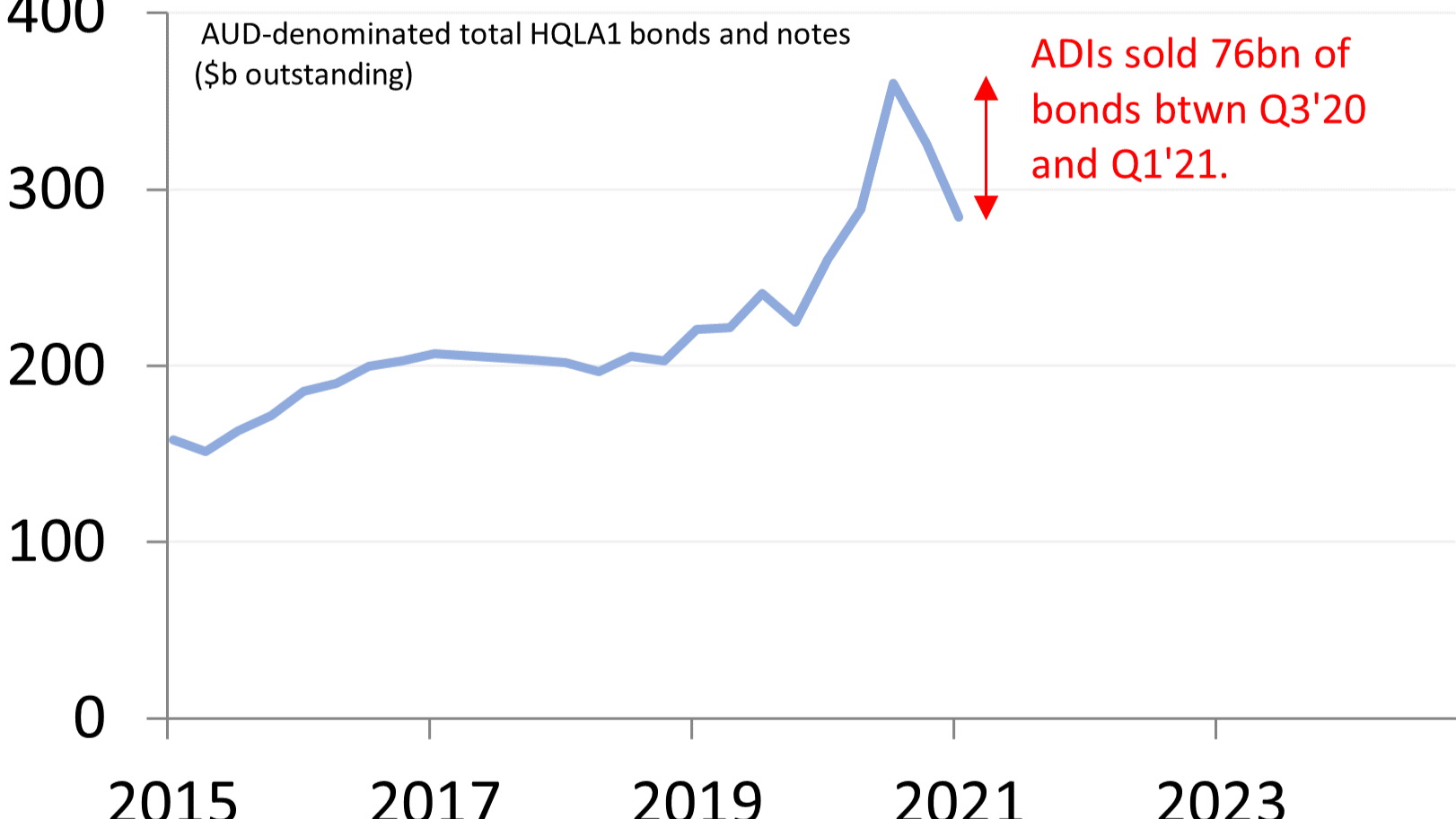

For the system as a whole, this won't be a problem upfront. According to APRA data, the aggregate Australian Dollar LCR for LCR-ADIs, excluding the CLF, was about 108% in Q2'21 (it was 132% including the CLF). However, the aggregate hides some important differences. We know from the various Pillar 3 reports that smaller banks tend to rely on the CLF to a much greater extent for HQLA, so they are going to come looking for assets.

As a general rule, banks like to get ahead of regulatory change, so I fully expect that they will seek to end their reliance on the CLF well before the closure at the end of 2022. This means that they'll also be looking for assets.

If they want to get to 125% without the CLF, they'll need to find a little over $80 billion of HQLA. If they want to get back to 132% on the AUD LCR, they'll need to find $116 billion of HQLA (not all of the $139 billion of CLF showed up as liquid assets stacks as reported to APRA).

Regulation (which I think should to be changed) means that ADIs won't necessarily hold all this extra HQLA as bonds -- though I think they will buy some more. The lack of revenue associated with that ES Cash makes it a bit hard to stomach, particularly for the smaller ADIs (who tend to have lower ROE hurdles).

All this means that Semis are likely to tighten a bit from here.

Related wires

Macro

Better aligning fiscal, monetary, and bank regulatory policy

View

Macro

Unravelling the Aussie bank liquidity mystery

View

Want more content like this?

Give this wire a like if you've enjoyed the discussion and hit follow to be notified when new episodes are released.

If you're not an existing Livewire subscriber you can sign up to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Matt is a portfolio manager at Coolabah Capital, an asset manager than runs over $8 billion in fixed-income strategies. Matt has 17 years of experience on both the sell-side and buy-side. He spent most of his career (2008 to 2020) at UBS, the last five years as a Managing Director; most recently as the Global Head of Rates Strategy. Prior to this he worked as the Head of AUD/NZD Rates Strategy in Sydney; and headed up the Asia Pacific Knowledge Network in Singapore. Outside of UBS, Matt has worked for Millennium (the Hedge Fund), ICAP (the inter-dealer broker), 4CAST (now Continuum Economics), and the Australian Productivity Commission.

2 topics

Matthew Johnson

Portfolio Manager

Coolabah Capital

Matt is a portfolio manager at Coolabah Capital, an asset manager than runs over $8 billion in fixed-income strategies. Matt has 17 years of experience on both the sell-side and buy-side. He spent most of his career (2008 to 2020) at UBS, the...

Matthew Johnson

Portfolio Manager

Coolabah Capital

Matt is a portfolio manager at Coolabah Capital, an asset manager than runs over $8 billion in fixed-income strategies. Matt has 17 years of experience on both the sell-side and buy-side. He spent most of his career (2008 to 2020) at UBS, the...

Comments

Comments

Sign In or Join Free to comment

most popular

Funds

The 5 best-performing super funds of the year

Livewire Markets

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets