APRA's new capital rules: initial thoughts and implications for the banks

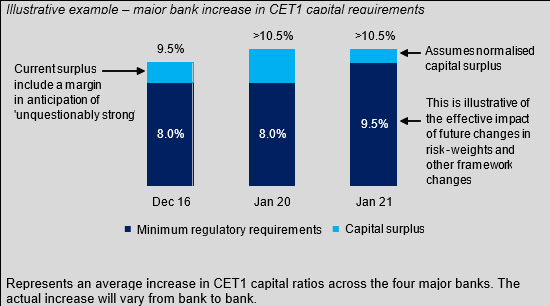

APRA have finally come out with their capital rules to fulfil the ‘unquestionably strong’ requirement of the Financial Services Inquiry. The focus is on is the Common Equity Tier 1 ratio requirement (CET1), which is the amount of equity the banks need to hold relative to risk weighted assets (loans). The minimum for the big 4 is currently 8% and they all hold a minimum buffer of at least 1% above that. The minimum is going to move to 9.5%, plus the 1% buffer, meaning they will need to hold at least 10.5%. As of their last results they all hold high 9’s to low 10’s already in anticipation.

Source: APRA

What does this mean for the banks?

All else being equal, the task is pretty small over the next three years for the big 4 banks ($1.5-3bn for CBA, NAB and WBC and ANZ will likely be in surplus, and definitely so post selling their Wealth business). It is unlikely to result in an immediate capital raise by the banks – APRA themselves noted the major banks can get to the required level organically. DRP discounts are likely to continue to help grow capital and at worst perhaps an underwritten DRP or two in the next couple of years to get there. The time line is reasonable, as they have until 2020 to meet requirements.

Some questions remain unanswered

1. Finalisation of Basel IV international rules. APRA wants to make sure they are in line with the outcome of those rules. This will be in the form of calibrating mortgage risk weights with whatever Basel IV finally lands on, as well as the operational risk framework. APRA have said that they have effectively taken that into account already (that risk weights are going up) and any further changes won’t be additive to the capital requirements announced today. So whilst risk weights will rise, to be in line globally, total capital requirements won’t. That is a big positive relative to expectations.

2. Mortgage concentration risks in Australia. APRA are concerned the banks have too much exposure to one asset class. They specifically have noted investor lending and higher LVR lending. So there is more to come on mortgages. It is a little contradictory to their first statement, however what it appears to mean is that while on average there is no change once mortgage risk weights are finalised. Banks with more mortgages - especially more investor mortgages or higher risk lending - will have to hold more capital, those with less will hold less. I would note that Westpac and CBA are the ‘mortgage banks’ whilst NAB and ANZ are more ‘business banks’. The initial reaction will unlikely differentiate between them, but that will come over time.

Positive implications for the banks

- Reduced risk of capital raisings upfront (capital does need to rise slowly in the next 2-3 years but can be done organically).

- The market finally knows where (on average) capital needs to sit for the banks which is in line to better than feared, so we can finally mostly move on (except for the details on mortgages later this year).

- ROE will still be under pressure however they have several years to slowly reprice as capital rises.

The market is broadly neutral to underweight banks, partly on these fears, so we expect to see some covering as this is an issue that has shadowed the banks for years now. Given the bank repricing coming through this half (quite material), plus lower deposit pricing/competition, plus no capital raisings, it seems as if the outlook for the domestic banks has improved in the near term. However risks remain, it is still a tough grind for them overall, especially in the medium term where growth is low and a credit cycle will eventually occur, and volumes are likely to remain low to falling, but near term looks a little better. Political risk remains present however and is unlikely to go away, but at least we can tick off one of the large overhanging risks.

For more insights from Alphininty Investment Management, please visit our website: (VIEW LINK)

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Andrew is a Principal of Alphinity Investment Management. His focus is on the Financials and IT sectors, as well as portfolio management oversight. Andrew was previously a Vice President and Research Analyst for AB’s Australian Equities Fund, as well as oversight for the management of the Australian Concentrated Fund. Prior to joining Alliance, he spent several years with JB Were Stockbroking as Senior Analyst covering the gaming and insurance sectors respectively. Andrew is a Fellow of the Institute of Actuaries Australia and holds a Bachelor of Economics from Macquarie University, and a Graduate Diploma in Applied Finance and Investment from the Securities Institute of Australia.

3 topics

4 stocks mentioned

Andrew is a Principal of Alphinity Investment Management. His focus is on the Financials and IT sectors, as well as portfolio management oversight. Andrew was previously a Vice President and Research Analyst for AB’s Australian Equities Fund, as...

Expertise

Andrew is a Principal of Alphinity Investment Management. His focus is on the Financials and IT sectors, as well as portfolio management oversight. Andrew was previously a Vice President and Research Analyst for AB’s Australian Equities Fund, as...

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management