Are Aussies splashing or stashing their cash?

The last six months has been a uniquely challenging period, with the COVID-19 disruption being significant enough to bring Australia’s 29 year recession-free streak to an end. Despite this, one notable bright spot has emerged: spending on consumer goods. This spending has been particularly strong in categories such as furniture, home improvement and electronics. The strength in these categories, which has clearly been supported by government stimulus, will inevitably decelerate from current levels over time. But are there reasons to be more optimistic on the outlook for consumer spending than the media headlines might lead us to believe? This newsletter covers recent data points which suggest that some optimism might be warranted.

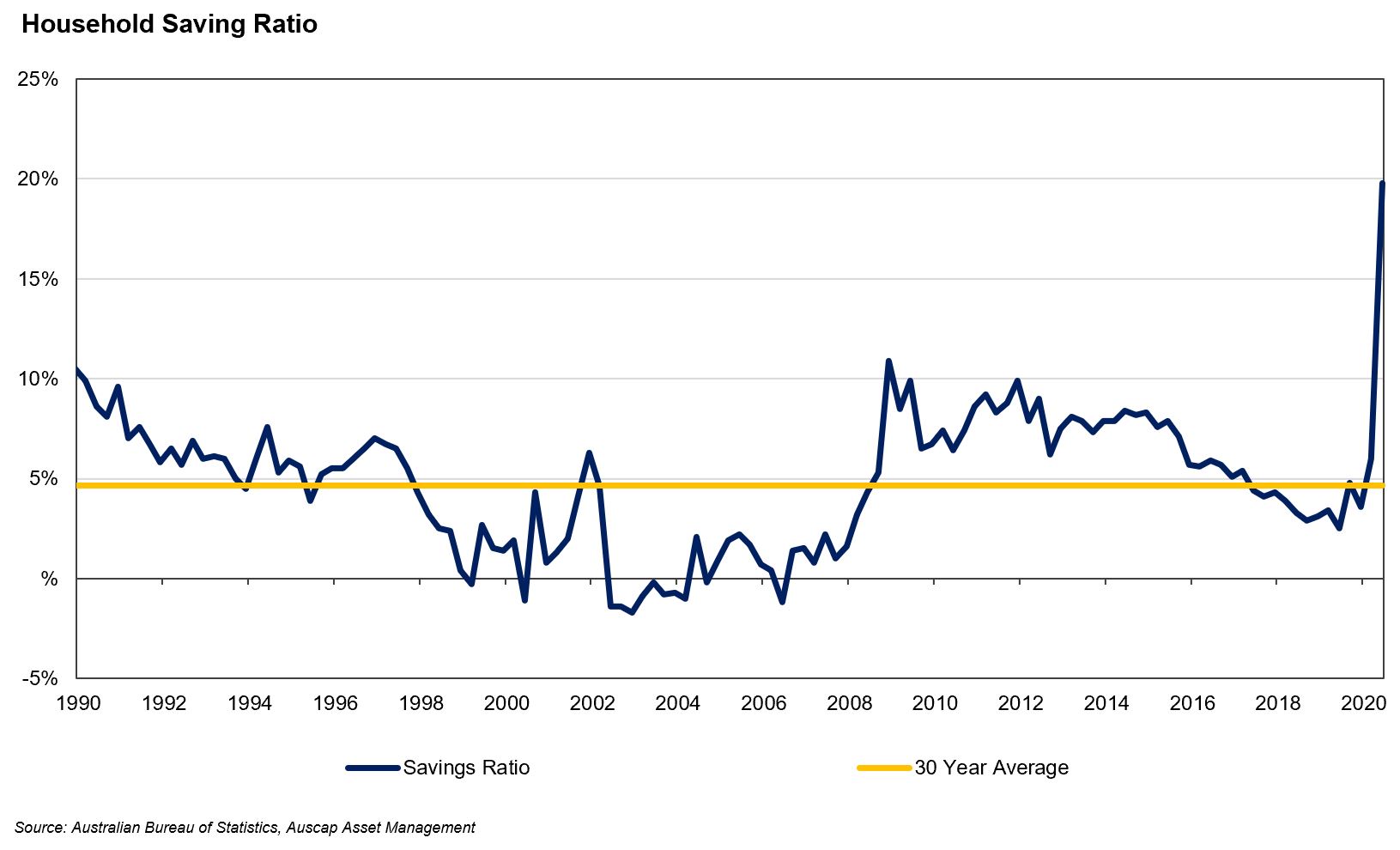

Over the last 30 years, Australian households have saved an average of 4.7% of their net disposable income per annum. In the June quarter just gone, this rate rose to 19.8%, the highest level recorded in 40 years. This extraordinary $42bn increase in household net savings was due to a $35.2 billion fall in household spending and a $7.1bn increase in income due to the Government’s income assistance measures. If the early access to superannuation scheme were included as a savings measure, the household savings ratio would have jumped to 24.8%.

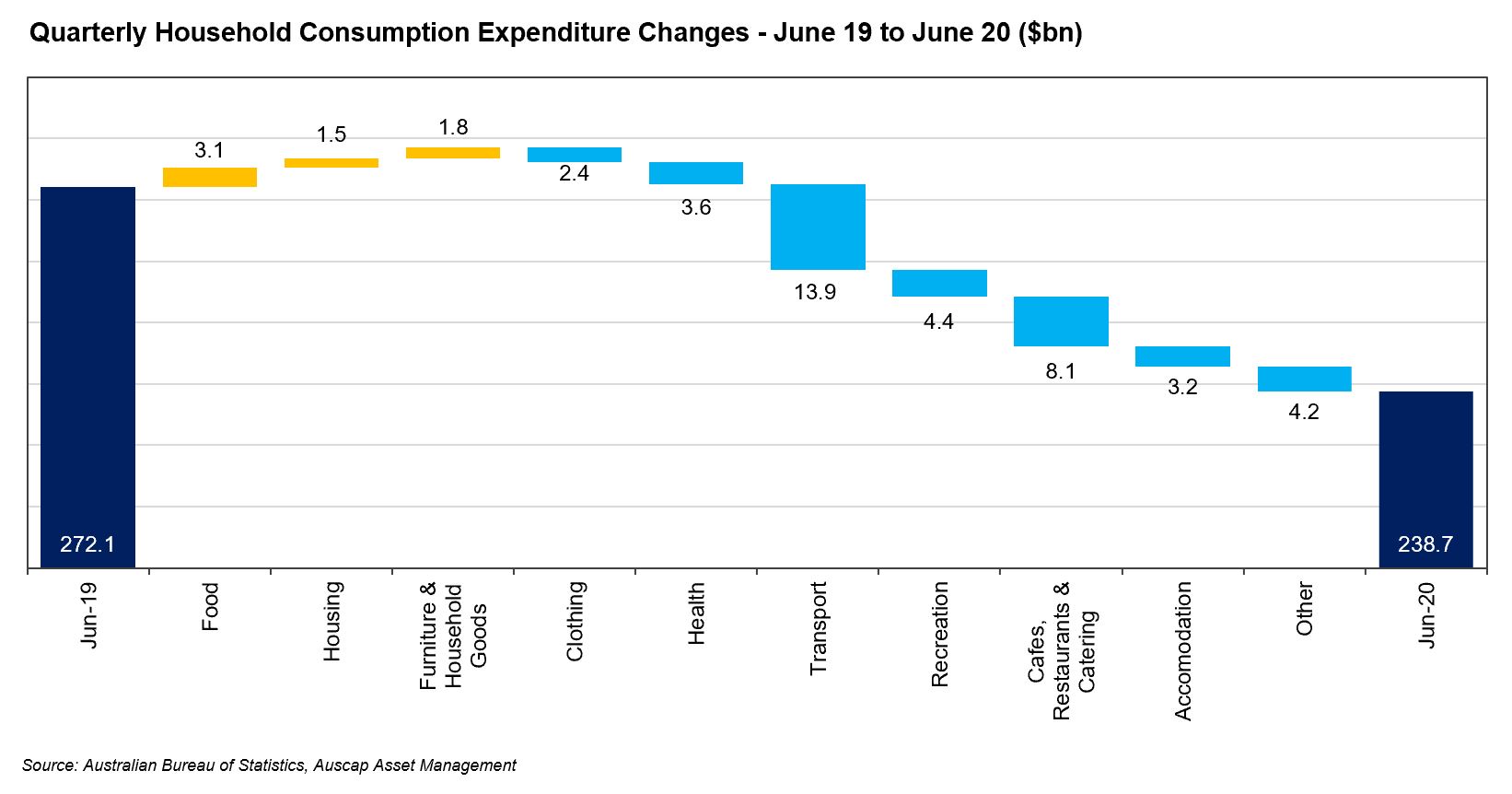

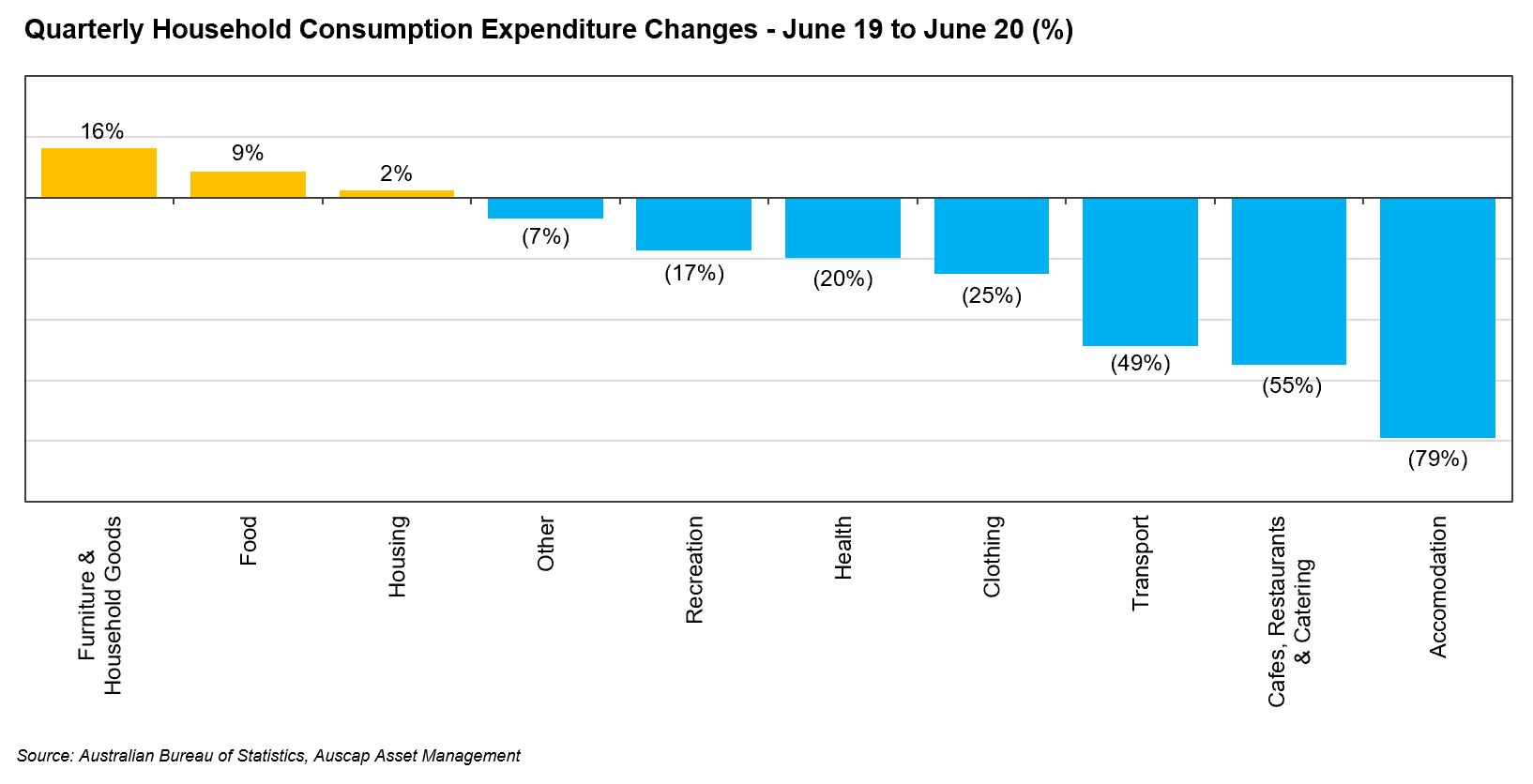

Whilst there has been much commentary on the acceleration of consumer spending on household items, it is worth putting this strength in context. Australian Bureau of Statistics (ABS) data suggests furniture and household goods spending accelerated by $1.8bn in the June quarter. However, this increase appears relatively minor in the context of material declines in most other major categories of expenditure, with a net reduction in expenditure of over $33bn.

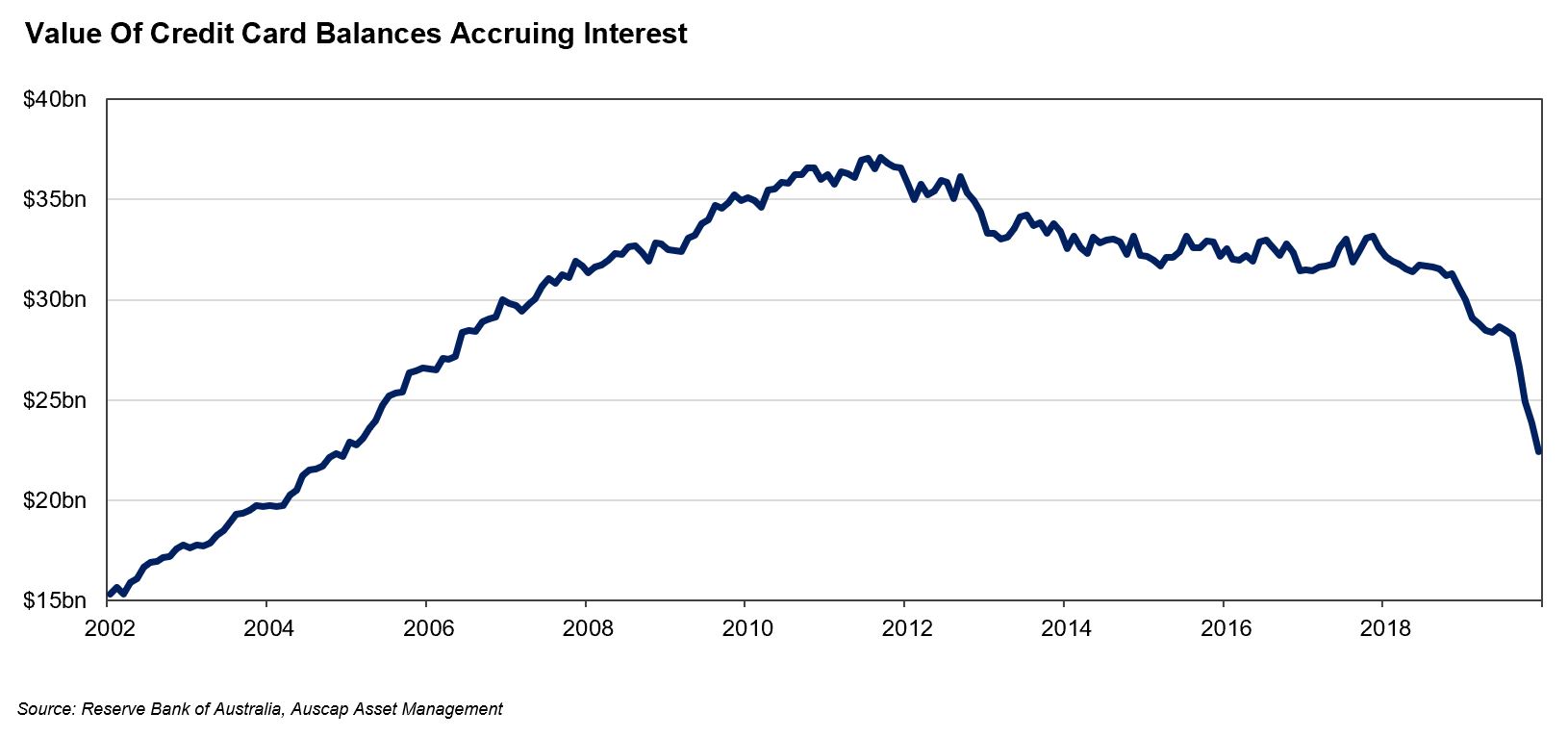

Rather than using the Government’s income support and reduced expenditure in categories such as travel and transport to splurge on discretionary goods, it appears that the majority of households have prudently decided to improve their personal balance sheets. Australian credit card debt has fallen over 20% to $22.4bn in June 2020 from $28.4bn in December 2019, as shown in the following chart. The Commonwealth Bank of Australia has reported that its savings accounts and term deposit balances have grown 5% between January and July 2020. Similarly, leading alternative finance company Zip has seen its customer repayment rate increase from 13% in December 2019 to a high of 16% in May 2020. Clearly, a number of Australians are using COVID-19 as an opportunity to save.

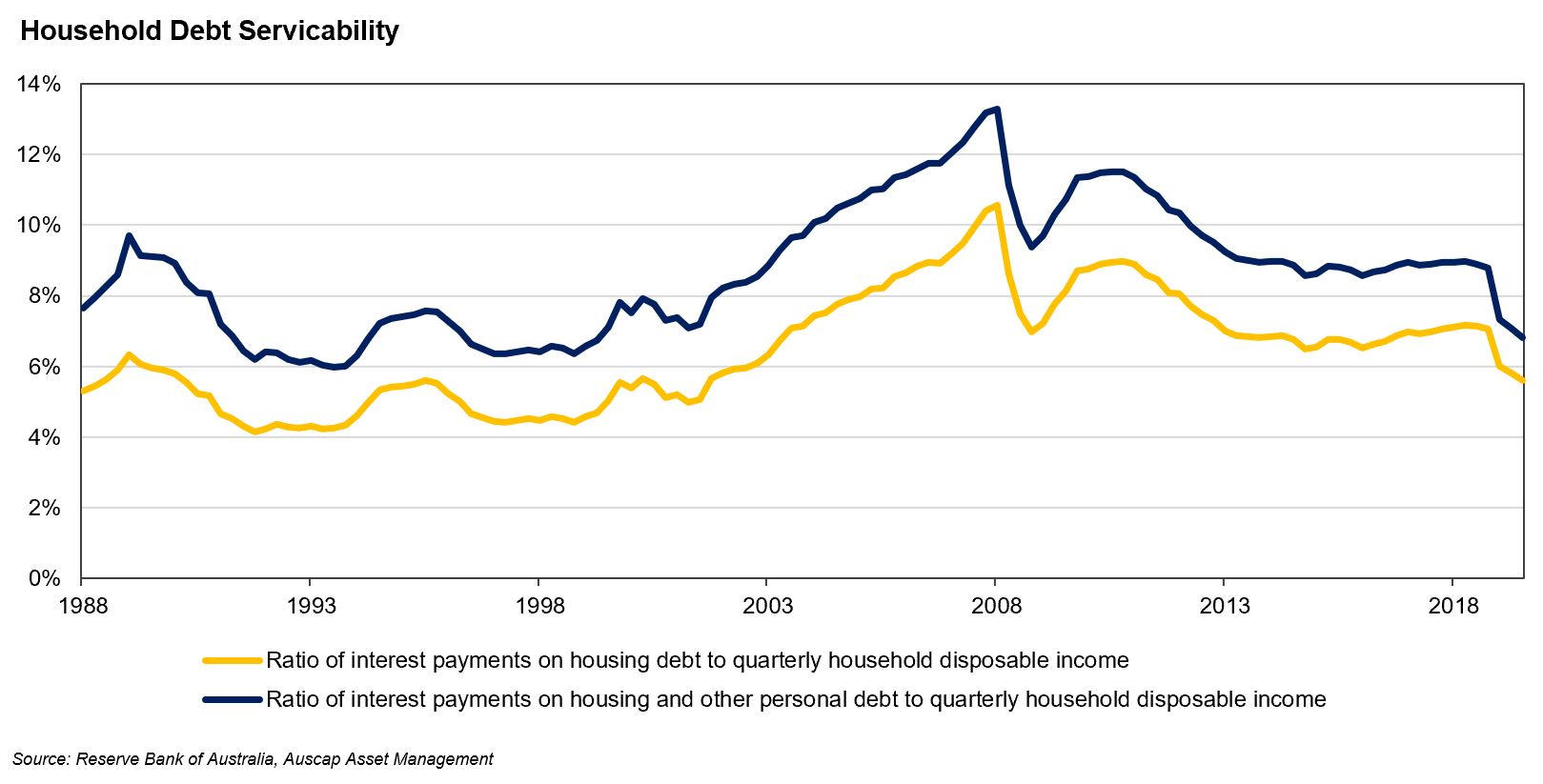

While it is positive to see consumers reducing their high-interest bearing credit card debt, most Australian household debt relates to housing. With the Reserve Bank of Australia cutting the cash rate to a record low 0.25% and providing forward guidance that they are unlikely to increase this rate for “at least three years”, housing debt interest serviceability has dropped to 5.6%, a level not seen since 2002. Total interest payments as a percentage of household disposable income now sits at 6.8%, the lowest level in two decades.

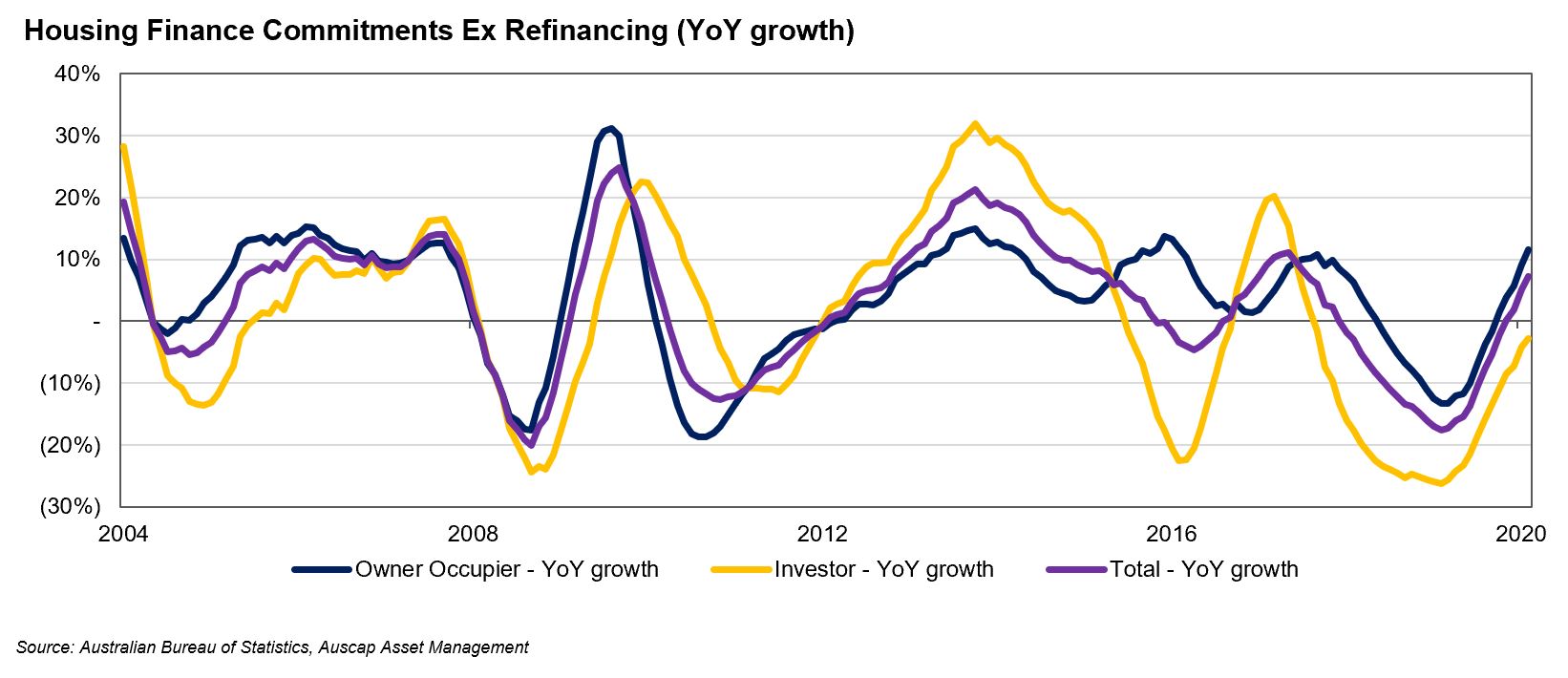

Given the low interest rate environment and improving consumer balance sheets, interest amongst Australians in investing in property, particularly in the owner-occupier category, looks to be re-emerging. New housing loan commitments rose 8.9% on a seasonally adjusted basis in July, which the ABS called out as “the largest month-on-month rise in the history of the series”. This data is shown in the following graph on a twelve-month rolling basis.

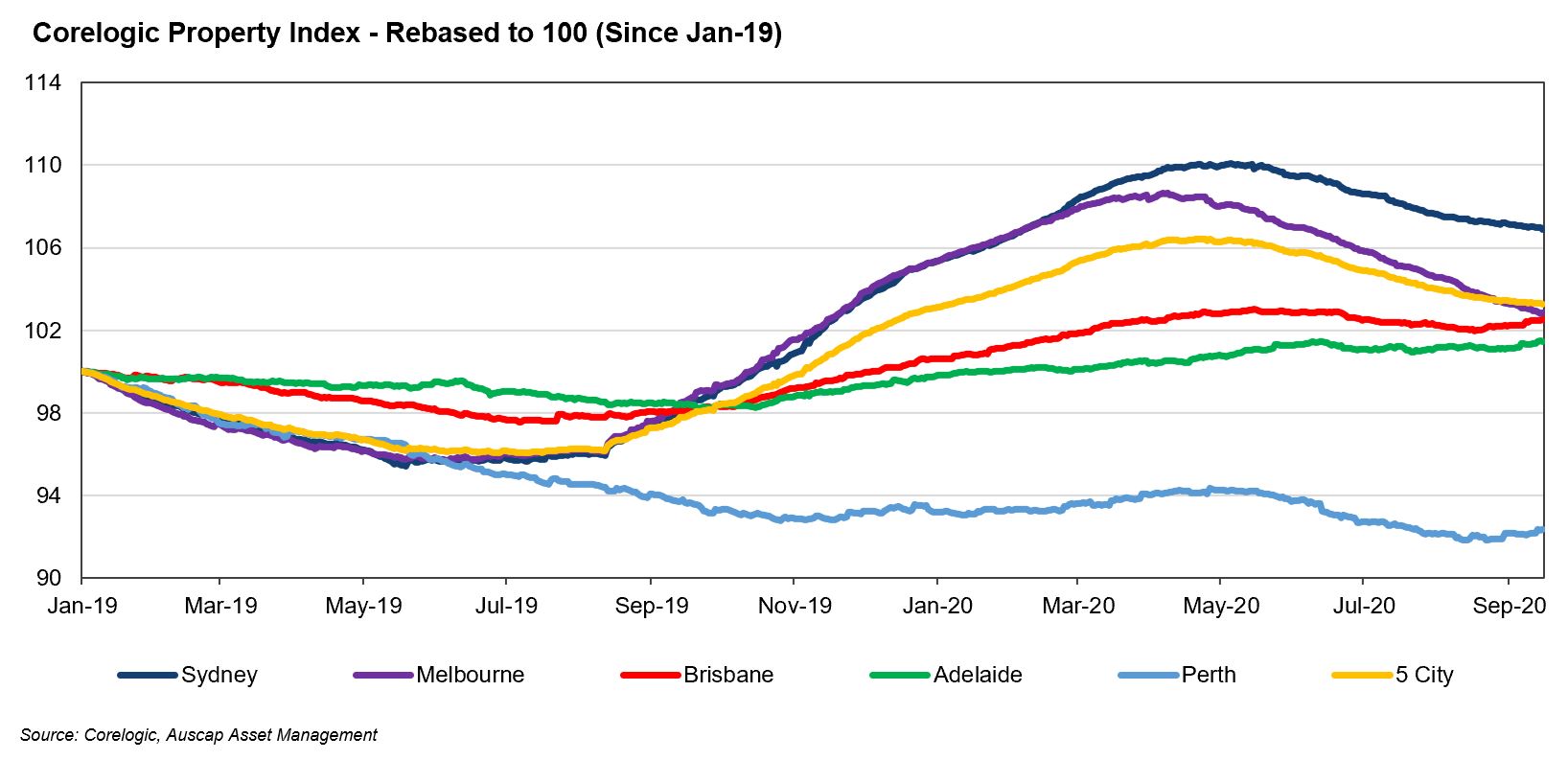

At the height of COVID-19 uncertainty, market economists overwhelmingly predicted double digit falls in Australian house prices. Corelogic property price data indicates that capital city house prices have fallen circa 3% from the April 2020 high. However, this only puts house prices back to January 2020 levels, and the recent moderation in declines suggests that the probability of widespread “negative equity” in the case of defaults is currently low, absent a further significant fall in property prices.

The market is justifiably focused on a pull-forward of consumer demand and elevated spending in some categories, the rise in unemployment and the impact of the gradual withdrawal of stimulus. However, the household balance sheet repair and serviceability of household debt provide reasons to be optimistic about the medium term outlook for consumer demand.

Not already a Livewire member?

Sign up today to get free access to investment ideas and strategies from Australia’s leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short portfolio using Proprietary funds. Prior to 2007 he worked at Macquarie Bank within the Investment Banking Group. Tim is a CFA charterholder, a CMT charterholder, a Senior Associate of FINSIA, a Graduate of the Australian Institute of Company Directors (GAICD) and has a Bachelor of Laws (Hons) from the University of Sydney and a Bachelor of Commerce from the University of Sydney.

........

Tim Carleton is a Principal and Portfolio Manager at Auscap Asset Management (Auscap), a boutique equities long/short investment manager. This article contains information that is general in nature and does not constitute investment or any other form of advice. This article does not take into account the objectives, financial situation or needs of any particular person nor does it constitute a recommendation to be relied upon when making an investment or any other decision. You need to consider your financial needs before making any decision based on the information in this article and a person should obtain and consider the relevant disclosure document before deciding whether to invest in an Auscap fund. No part of this article is to be reproduced or disclosed without the prior written consent of Auscap. In relation to any MSCI data in this article, the MSCI data is comprised of a custom index calculated by MSCI for, and as requested by, Auscap. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Tim founded Auscap Asset Management in 2012. He has 19 years’ experience in the financial services industry. From 2007 to 2011 he was an Executive Director at Goldman Sachs where he was responsible for managing an Australian equities long/short...

Expertise

Comments

Comments

Sign In or Join Free to comment