Are ETFs to blame for market volatility?

For years concerns have been brewing among a growing number of participants that the staggering rise of index-tracking and exchange-traded funds (ETFs) would lead to much higher levels of volatility during times of crisis.

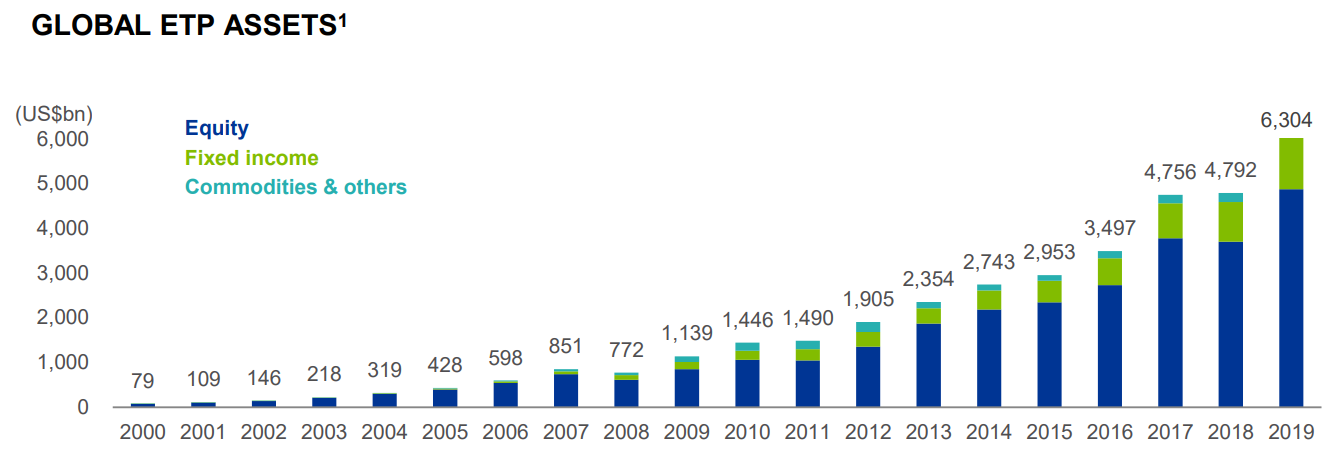

In 2019, index funds and ETFs hit US$4.27 trillion in assets under management, surpassing their active peers in the size for the first time in the United States. After reaching that milestone, the legendary hedge fund manager Michael Burry – who shorted CDOs during the sub-prime crisis and was portrayed in The Big Short – warned that passive funds are the next “subprime CDOs”.

Burry leads a camp of investors who believe that the concentration of assets within ETFs would exacerbate market moves and lead to indiscriminate selling in the event of a downturn.

Source: BlackRock Global ETP Landscape

But Tim Farrelly, Principal of Farrelly’s Investment Strategy, says pointing the blame at ETFs during times of market stress is fundamentally flawed.

Does indexing distort markets? At the edges, a little, he reckons, but says nothing like the "overblown claims" from the many active managers who simultaneously blame the rise of index funds for their underperformance and claim that the gain in indexing’s market share makes their job easier.

Image: Tim Farrelly, Principal of farrelly’s Investment Strategy

Farrelly’s advises financial advisers and dealer groups on model portfolios' design. He prefers investing in ETF over conventional managed funds as ETFs can easily traded, and have some real advantages when it comes to redemptions.

"Are ETFs some form of liquidity trap? Maybe, but that has nothing to do with ETFs per se. If all the capital in ETFs was invested with active managers, that capital would still find its way into the markets. If that capital ever decided it was time to exit, it would matter not one iota whether it is invested in ETFs, unit trusts or separately managed accounts. The same volume of securities would need to be sold."

He says investors need to understand that ETFs are a collective investment vehicle designed for investors to make strategic and tactical bets on the market. They of themselves do not distort markets any more than someone making the same bet in another vehicle.

“They are not in any way inherently dangerous. They are simply as good or as bad as the assets and strategies inside them. Just like unit trusts - and just like separately managed portfolios."

Navigating current markets with ETFs

Prior to the Covid-19 crisis, Farrelly had reduced his exposure to U.S. equities based on stretched valuations and is now finding good bargains in European shares via the Vanguard FTSE All-World ex-US ETF (ASX:VEU). Mixing this with a U.S. equity ETF allows you to dial-up or down your U.S. exposure, he says.

Fixed interest is another area where ETFs are available in ways that are not available elsewhere. He argues that from a medium-term time horizon (4-5 years), investment-grade credit generally beats TDs and government bonds.

The sweet spot is in A and BBB credits which pay healthy spreads above government bonds and experience moderate credit losses, normally much lower than the spreads.

But he warns investors about the catches with ETFs that invest in these securities:

- In times of panic (like now), spreads can blow out causing steep price falls. However, these falls tend to be quite short-term and, unlike falls associated with equities, tend to recover within a year or two. Hence the importance of a medium-term time frame.

- It’s difficult finding actively managed funds that concentrate on A and BBB securities. Either they have significant exposures to AAA and AA securities which reduces returns or they stray into junk bond territory, which substantially increases risk.

He likes the BetaShares Australian Investment Grade Corporate Bond ETF (ASX:CRED) and VanEck Vectors Australian Corporate Bond Plus ETF (ASX:PLUS).

The two have quite different maturity profiles.; CRED averages about 7.5 years which means that it will be volatile when bond rates are moving around. In the 2019 calendar year, it returned over 10% as bond rates fell sharply. PLUS is less volatile as it invests in shorter-dated bonds. More recently both have fallen heavily as yields on investment-grade credit have increased sharply and liquidity has dried up.

He notes that the drying up of liquidity is a function of the underlying market, not the ETFs themselves. Had either of these funds been a unit trust or a separately managed account the investors' experience would have been similar.

"In both cases, this short-term loss should be made up in the medium term by the higher interest rates now on offer – so once again, with a five-year time horizon in mind, these are reasonable options."

The questions facing investors looking at these vehicles are:

- Is my time horizon really five years?

- Do I understand why bonds might be volatile?

- How well do I understand credit risk?

- Is the return high enough to offset the credit risk?

“None of which are rocket science – but do take a while to master. It is worth getting advice on how these vehicles fit together."

Never miss an update

Stay up to date with my content by hitting the 'follow' button below and you'll be notified every time I post a wire. Not already a Livewire member? Sign up today to get free access to investment ideas and strategies from Australia's leading investors.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

3 topics

3 stocks mentioned

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

I have over 15 years’ experience covering financial markets and property, with a particular interest in ETFs and personal finance. I split my time between Australia and Canada to bring a global perspective to my work.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management