Are markets topping or pausing?

That was the first question I put to a panel of fund managers in front of a live audience of investors at a private event we held in conjunction with IRESS last week. The consensus view is that the current pull back is merely a pause before markets continue to advance higher. There were, of course, the usual caveats about ‘time in the market vs timing the market’, however, this big picture question set the tone for a cracking discussion on a range of issues confronting Australian investors today.

The session featured Ben Griffiths from Eley Griffiths Group, Perter Gardner from Plato and Andrew Mitchell from Ophir. Here’s a snapshot of some of the key issues discussed with a podcast of the full discussion available below.

Are markets topping or pausing?

The panel were unanimous in their views that the current advance in equities will remain intact and that the recent sell off has been a healthy pull back.

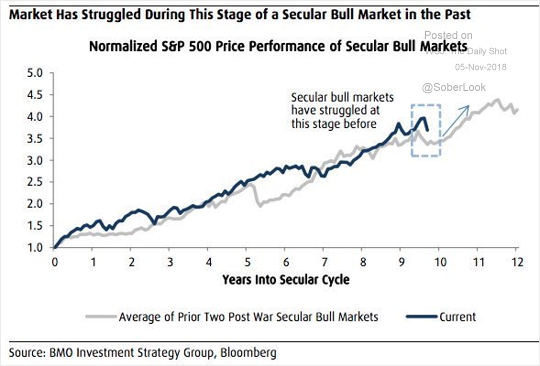

Griffiths pointed to the history of bull markets since the World War 2 (see chart) and highlighted that secular bull markets struggle in the 9th year of an advance.

There has to be a reset, and we've just gone through it, and it's been the third most painful in 40 years.

Gardner said fundamentals remain strong, however, issues like weakness in domestic housing are creating uncertainty.

Mitchell advocated owning higher quality companies as he expects them to outperform when markets fall. On the recent sell-off he explained that there had been a readjustment lower in terms of the earnings expectations in the US.

“That's caused a broader selloff, but we think this is a pause and a great buying opportunity for companies that are caught up in the cross hairs of the selloff.”

Three front page issues

I picked out three issues that appeared to be front of mind for investors. Rather than setting the agenda I asked the room to vote on the issues that were most important to them. Here they are in the order they were addressed.

Issue #1 Regulation and political uncertainty

I thought people may have had enough of talking about royal commissions and franking credits – clearly not. On the issue of scrapping franking credit refunds for retirees, Peter Gardner from Plato argued that the policy was highly discriminatory. However, he played down the likelihood of the policy getting through in the current format.

“What effect would this have on stock markets, or Franking Credit stocks? There will be some minor pressure, I think, on the banks, Telstra, and a lot of those high Franking Credit stocks, but I don't think it will be major.”

Andrew Mitchell said they try and avoid any stocks that are involved in royal commissions. He said the prices tend to stay in the 'sin bin' and that often the companies have management teams that don’t pass their filters.

“When they become a battleground sort of style stock, we don't like sticking around. They tend to go lower, and they stay in the sin bin for quite some time.”

Ben Griffiths made the point that these issues, whilst important for us as individuals, have the potential to become a distraction for investors. He said too much time and effort can be taken up with trying to anticipate the next move and potential outcome.

One thing's for sure, it always pays not to pre-empt.

Issue #2 Falling residential property prices

The discussion got quite intense around this issue and I was surprised how keenly attuned to this issue the three managers were. Perhaps, most alarming was Ben Griffiths’ revelation that the first bankruptcies in building companies are starting to happen.

“I'm surprised it's happened so early in the piece. We haven't really gone into the teeth of the slowdown, and we're already seeing companies going into receivership. I'm quietly stunned how quickly this has actually taken place.”

Mitchell shared Ben’s sentiment and pointed to the importance of consumption in the Australian economy.

If the housing market is weak, then it’s going to vibrate through the economy. We’ve already seen some of the discretionary retailers downgrade.

If there was a silver lining to the discussion it came from comments made by Peter Gardner. Given the prevalence of bank shares in the portfolios of many investors it was somewhat welcome news to hear that, in his view, bank dividends look sustainable.

“At the moment, our models are continually updating and changing as conditions change, but at the moment we don't see any short-term pressures on the banks to cut their dividends.”

When you factor in franking ANZ NZ (ASX:ANZ) and Commonwealth Bank (ASX:CBA) are yielding ~9% with National Australia Bank (ASX:NAB) and Westpac (ASX:WBC) offering double digit yields. Gardner says he will be keeping a close eye on bad debts as a lead indicator that dividends could come under threat.

At the moment the banks are a cosy up Oligopoly... There are levers that the banks can pull to try and increase their earnings.

Issue #3 Rising US interest rates

As I write the S&P500 has just had a 600+ point rally sparked by dovish comments from the Chair of the Fed Reserve. Clearly, investors had been on edge that the Fed was going to crush this market with rate hikes. On reflection, the points below from Ben Griffiths appear pretty much spot on and drives home the value of having access to the fund managers.

“What's of most interest, I think, is, and this is really a development that's taken shape in the last four weeks or so, and that is that there is increasing evidence to hand in the U.S. market, the U.S. economy, that around the edges things are slowing.”

“There's enough slowdown, within what has been a buoyant economy, to actually wonder whether the Fed doesn't hike when it meets December 20 of this year.”

It would appear the Ben had some good mail and investors have once again celebrated growth and risk assets in a world of low interest rates.... for now.

A few key ideas

Against that setting I pushed the panel for a few key ideas on areas to invest in or to avoid. Here are a few that popped out for me.

Avoids

Peter Gardner singled out AMP as a stock likely to cut the dividend. He also made the case for further dividend cuts for Telstra (ASX:TLS) in the coming years.

“Management is effectively signaling that we're going to cut dividends again at some point in the future. They're announced that they're going to keep it for the next year, I think it is, but after that we wouldn't be surprised if that dividend cuts.”

Ben Griffiths said that with the exception of Afterpay (ASX:APT) they are steering clear of hyped up and expensive technology stocks. He also issued a warning on A-REITS:

“There's a time when you might want to own property trusts. They're a big part of our benchmark. They're often a good place to hide in uncertain times. We wouldn't be going there. We'll let cash stay rather large in the allocation.”

Key ideas

Andrew Mitchell used Reliance Worldwide (ASX:RWC) as an example of a stock they’re happy to own even if markets take a turn for the worse.

“From our perspective, we're seeing high quality businesses that are on cheap valuations now, and this is a good time to buy those. If we say that we're late cycle, then they're exactly the stocks that you want to take down in a big market retraction.”

On the income front, Peter Gardner said that he still thinks resources stocks are in a great position to pay out dividends. He highlighted both RIO (ASX:RIO) and BHP Billiton (ASX:BHP), which are yielding ~7% fully franked.

“Generally, you don't want to invest in resource companies when they're doing major investments... But when they're just sitting, doing their knitting, returning cash to shareholders, that's when resource companies generally do well, and that's at the moment, the cycle that we're in.”

Griffiths made an interesting point that he had let cash build up to the highest level in 18 months. Expanding on his comments about the US rate hiking cycle he singled out the resources stocks as potential beneficiaries should there be weakness in the US dollar and highlighted the key event he is watching.

“I think there's a fair chance that December 20, we'll get some tempering in that whole rate hike trajectory. That might be enough to see the U.S. dollar lower and things change.”

“What will happen then is the U.S. dollar will sell-off on the back of the tempering. That's when resources come into their own.”

The full discussion

Thanks to IRESS for hosting the event and thanks to Ben, Andrew and Peter for sharing their views. You can access a recording on the link below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions.

Safe investing and thanks for reading Livewire.

10 stocks mentioned

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions. Safe investing and thanks for reading Livewire.

Expertise

Livewire is Australia’s #1 website for expert investment analysis. We work with leading investment professionals to deliver curated content that helps investors make confident and informed decisions. Safe investing and thanks for reading Livewire.

Expertise

Comments

Comments

Sign In or Join Free to comment

most popular

Investment Theme

If 24 LICs ran the Melbourne Cup, which ones would we back?

Affluence Funds Management

Equities

Buy Hold Sell: 5 ASX stayers built to go the distance

Livewire Markets