Are resources safe in this environment?

2020 has certainly not started the way anyone would have hoped for, and we sincerely hope that you and your loved ones are safe and healthy. From what initially appeared to be an isolated health crisis in China, in the space of a couple of months the rapid spread of the virus across the globe has now become a major health crisis triggering a global economic recession. Deaths, unemployment and some wealth destruction are some of the dramatic fallouts that will emanate from it. Economically, the wave of the virus has transformed from a supply chain disruption - with everybody suddenly realising how much we depend on China - to a global demand shock which then triggered significant solvency and liquidity concerns. As portfolio managers, our role now is to protect investors’ capital as much as possible during this fall.

Resources stands out as a sector that has proven more resilient than most, but is it really a safe heaven?

Oil prices set to drop further

The fundamentals are very different amongst the various types of resources Australia produces – one needs to clearly differentiate.

Oil is not in a good place. Oil fundamentals are the worst they have been for a long time. As the demand shock around the world was about to sharply reduce demand by at least 15%, a dispute between OPEC and Russia as to who should bear the brunt of this fall has resulted in an battle of egos, with all parties deciding, instead of cutting production to balance the market and protect the price as OPEC normally does, to actually produce as much as they can, adding to the oversupply another 5% - or 5 million barrels - per day.

So lower demand and higher supply is resulting in a free-for-all until the next OPEC meeting in June. In the June quarter the surplus becomes a staggering 20%+ of world production, raising the issue of finding sufficient storage capacity. This will ultimately force production cuts as the lower prices will put marginal cash cost producers out of business instead of OPEC or Russian barrels, as was their intention.

A further complication is that the most marginal producers are in the US shale oil sector and are largely protected by price hedges in coming months, extending the required supply adjustment into the second half of the year. In meantime it is not inconceivable that oil prices drop to $15-20 per barrel. Such a violent drop in prices - at this point more than a 60% price correction - will lead to insolvencies and cause severe damage to oil producers, service providers and speculators exposed to the higher prices.

To be clear, if the price is sustained around the $25 per barrel level, none of the Australian large producers would be economic.

All companies need to cut their costs and growth capital expenditure plans in order to protect their balance sheets and liquidity. That has become the main priority.

It is unlikely that marginal producers will return until the price is back to $US50 per barrel, and this is only likely once demand has recovered (i.e. the virus is controlled), inventories have de-stocked and global supply discipline is re-established. There will certainly be an investment opportunity in the sector at some point, but now feels too early. Alphinity is underweight the sector.

What about the rest of the sector?

Base Metals (Aluminium, Nickel, Copper, Zinc): these are not very attractive at the moment as they are currently very exposed to global economic demand, unlike bulk commodities. The demand shock is too violent not to affect the fundamental rebalancing through lower prices. For some commodities, however, supply disruptions may limit the surplus as some businesses have had to shut down their operations, or at least run at much lower rates to protect workers from infection. We see this already happening in the copper market where around 7% of global supply is out of action, so far mainly in Peru and Chile. Longer term fundamentals for copper remain tight. We favour Oz Minerals in this space due to its growth profile and very strong balance sheet. We also note that the weak $A means that in its domestic currency, its cash flows are almost unaffected.

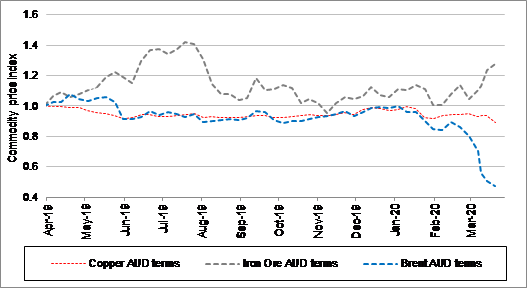

Commodity price movements in $A

Source: Credit Suisse, March 2020

Bulk commodities (Iron Ore and Metallurgical Coal): these still look robust, especially Iron Ore as it is the most exposed to Chinese domestic growth which appears to be on the verge of ramping up now that the very strict virus containment measures have largely been lifted. Underlying steel demand is already recovering fast.

We believe that once the Chinese government is confident that a second wave of virus containment is not required, it will then support the rebound of its economy through domestically-focused infrastructure programs.

This would restore confidence by physically demonstrating to its population that activity is back on track. While iron ore demand could still be negatively affected by falling Western world steel production, we note that Europe absorbs less than 10% of the seaborne market, and that the recent announcement of South Africa to suspend its mining industry for 21 days will further tighten the market. These tight fundamentals are currently reflected in a robust Iron Ore price. This, combined with a low $A, bodes very well for domestic producers such as Fortescue Metals, BHP and Rio Tinto.

Want the latest insights on Australian resources?

At Alphinity, I focus on the Energy, Materials and Utilities sectors. To be the first to receive my latest Livewire insights, hit the 'follow' button below.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

"Stephane is a Principal of Alphinity Investment Management. His focus is on the Energy, Materials and Utilities sectors, as well as portfolio management oversight.

Stephane was previously a Vice President and Research Analyst for AllianceBernstein’s Australian Equities Fund covering the same sectors from 2005 to 2010. Stephane’s prior background was primarily in management consulting, having worked with McKinsey & Company from 1997 to 2002 in South Africa and Australia, leaving the firm as an Associate Principal. Stephane holds a Commercial Engineering degree (with high honors) from the top-rated Universite Catholique de Louvain in Belgium. Stephane is fluent in French as well as German."

Featuring

Stephane Andre,

Alphinity Investment Management

"Stephane is a Principal of Alphinity Investment Management. His focus is on the Energy, Materials and Utilities sectors, as well as portfolio management oversight.

Stephane was previously a Vice President and Research Analyst for AllianceBernstein’s Australian Equities Fund covering the same sectors from 2005 to 2010. Stephane’s prior background was primarily in management consulting, having worked with McKinsey & Company from 1997 to 2002 in South Africa and Australia, leaving the firm as an Associate Principal. Stephane holds a Commercial Engineering degree (with high honors) from the top-rated Universite Catholique de Louvain in Belgium. Stephane is fluent in French as well as German."

2 topics

4 stocks mentioned

"Stephane is a Principal of Alphinity Investment Management. His focus is on the Energy, Materials and Utilities sectors, as well as portfolio management oversight. Stephane was previously a Vice President and Research Analyst for...

Expertise

Comments

Comments

Sign In or Join Free to comment