TOL - 5th Feb, 2021

Are risk markets entering a correction zone?

Chris Manuell, CMT

Jamieson Coote Bonds

The market adage of January being the barometer for equity market performance for the year will always get tossed around as investors outline their roadmap for the year ahead particularly coming off the historic events of 2020. The RBA may also be paying particularly close attention to the performance of the US equity market given the strong marriage of the pair since the nadir in risk markets last March. The RBA governor could become a fan of seasonals, with strong statistical evidence that the S&P 500 Index performance for the start of the year drives returns for the remainder of the year. With this in mind, the S&P 500 Index fell -1.11% (for the first month of 2021) in price terms and Deutsche Bank has studied data going back to 1872 that shows negative first months of the year have a strong impact on the performance for the remainder of the year, with 58% resulting in down years.

The RBA will be very disappointed that after embarking on an aggressive QE campaign it has failed to generate the transmission mechanism into the exchange rate that it would of anticipated – an 8% rally since November 2020 would have figured deeply in the surprise move to extend QE by another 100 billion of bonds or 5 billion a week for a further six months. The currency has managed to continue on its ascent with the global liquidity pump switched on full power mode driving a strong performance in commodities markets – with iron ore 22% of our exports – and domestic data surprising to the upside as the fiscal cheque book keeps printing alongside a successful Covid-19 suppression strategy.

The weakness of the USD has also played its part in providing a tailwind for the AUD which will stymie any attempts for the RBA to achieve its overly optimistic target of getting inflation consistently in the 2-3% target band. The RBA is not alone in lamenting the weakness in the USD with the ECB continuing to talk down its currency as USD strength will continue to undermine global economies’ attempts to escape a post-Covid world.

We monitor price action, sentiment and investor positioning as part of our rigorous investment framework and within that there are some subtle signs that indicate that risk markets may be entering a zone where they could pause or correct from their recent moves.

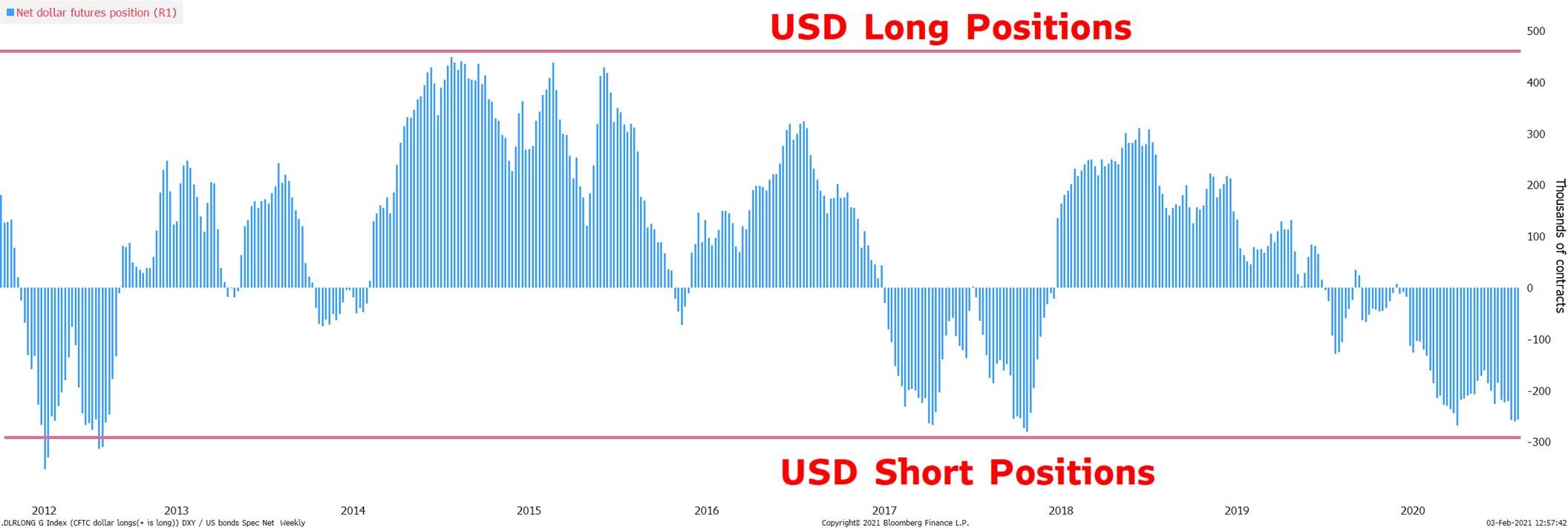

The record short positioning in the USD is a dangerous development with the market all on one side of the boat leaving it very unstable and vulnerable to any unexpected shocks which can generate aggressive unwinding.

The below chart highlights the historically stretched positioning of USD bears which will make it difficult for another secular leg lower in the USD currency as sellers become exhausted.

Source: Bloomberg

Source: Bloomberg

The robust correlation between the AUD and risk markets is well documented and is interesting to note that the price action of late has showed some signs of that marriage starting to sour which provides investors with a salient reminder of the old risk-on/risk-off nature of financial markets and of the possibility that the text-book philosophy of interest-rate differentials may become in vogue again in 2021. The intention of the RBA to weaken the currency with its outsized bond buying program might finally gain some traction if the US/Australian yield differential reasserts its downward trend. Careful what you wish for, as a weaker Australian currency could also suggest trouble lies ahead for risk markets in general.

Performance of Australian Dollar (RHS) and US Equities (LHS)

Source: Bloomberg. Past performance is

not indicative of future performance.

Source: Bloomberg. Past performance is

not indicative of future performance.Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Chris oversees a range of investment strategies for institutional and retail clients. He is a bond investment specialist with over 20 years of experience gained at Merrill Lynch, Société Générale and The Royal Bank of Canada, here and abroad.

........

This information is provided by JamiesonCooteBonds Pty Ltd ACN 165 890 282 AFSL 459018 (‘JCB’) and JamiesonCoote Asset Management Pty Ltd ACN 169 778 189 AR No 1282427. Past performance is not a reliable indicator of future performance. The information is provided only to wholesale or sophisticated investors as defined by the Corporations Act 2001 (Cth). Neither JCB nor JCAM is licensed in Australia to provide financial product advice or other financial services to retail investors. This information should not be considered advice or a recommendation to investors or potential investors in relation to holding, purchasing or selling units and does not take into account your particular investment objectives, financial situation or needs. Before acting on any information you should consider the appropriateness of the information having regard to these matters, any relevant offer document and in particular, you should seek independent financial advice.

2 topics

Chris Manuell, CMT

Senior Portfolio Manager

Jamieson Coote Bonds

Chris oversees a range of investment strategies for institutional and retail clients. He is a bond investment specialist with over 20 years of experience gained at Merrill Lynch, Société Générale and The Royal Bank of Canada, here and abroad.

Expertise

Chris Manuell, CMT

Senior Portfolio Manager

Jamieson Coote Bonds

Chris oversees a range of investment strategies for institutional and retail clients. He is a bond investment specialist with over 20 years of experience gained at Merrill Lynch, Société Générale and The Royal Bank of Canada, here and abroad.

Expertise

Comments

Comments

Sign In or Join Free to comment