Assessing Australians' income options

With the COVID-19 pandemic continuing to disrupt economies and markets, investors are in uncharted territory, but the traditional benefits of a broad opportunity set remain. In March, the Reserve Bank of Australia cut the overnight cash rate target to a record low of 0.25%. The rate cut and ongoing economic fallout from the pandemic, including pressure on equity dividends, has had a significant impact on investors who rely on assets that produce steady streams of income.

In our view, diversifying income sources is key to avoiding left tail risks (the chances of a loss resulting from a rare event) that could drastically reduce an investor’s income, or worse, deplete their capital balances. Although rates are at record lows, for investors seeking steady income as well as capital preservation, it’s possible to construct a range of income-focused portfolios, some of which we estimate could deliver returns in excess of equities. And they can be selected based on an investor’s risk tolerance and liquidity requirements.

Assessing Australian investors’ typical income investments

When considering Australian investors’ income allocations, it is clear that many are comfortable with placing their capital in higher-risk assets in search of higher levels of income. In fact, allocations to equities and hybrid securities (which combine both debt and equity characteristics) are often the foundation of an Australian investor’s playbook. Individual property investments and real estate investment trusts (REITs), both of which add illiquidity and potential capital risk, are also popular income investments. Another component of many investors’ portfolios are term deposits; although these are perceived as low risk investments, they also are illiquid because they lock up cash, generally for 12 months or more, in pursuit of an incremental pickup in yield.

What are these typical income investments currently yielding?

- Equities: Globally, banks have either cut dividends or placed caps on dividends to ensure capital resilience. The latest data, as of 31 August 2020, for the Australian equity market shows that around 69% of companies on the ASX paid a dividend for the year ended June 2020 (down from 87% in the previous period) while dividends fell by 36% over the same timeframe.

- Property: Sydney rental yields have fallen more than 50 basis points (bps) to 2.92% in the June quarter, according to CoreLogic. Along with lower rental yields, the investment property market faces additional headwinds with rent-relief policies, including moratoriums on evictions.

- Term deposits: As of the end of September 2020, a one-year term deposit had halved in yield to 75 bps compared with the end of September 2019. In March 2020, the RBA announced a Term Funding Facility (TFF) that offers three-year funding to authorized deposit-taking institutions to support bank customers and help the economy through a difficult period. With this in place, Australian banks are well-funded and have less need of funding from deposits – term deposit rates are priced to reflect this.

Diversifying income sources: Income-focused fixed interest funds

We analysed a number of potential income models that comprise a range of fixed income investments and cater to varying risk tolerances. Each has been optimised and stress tested using our proprietary risk analytics infrastructure. The allocations range from primarily short-duration core bonds in the Conservative Income Model to income-generating assets such as diversified multi-sector bonds, including modest allocations to longer-dated credit strategies, in the High Income Model.

- Conservative Income Model: Australian short-duration bonds + global income-generating investments.

- Balanced Income Model: Australian short-duration bonds + larger allocations than in the Conservative Model to global income-generating investments.

- Growth Income Model: Australian short-duration bonds, global income-generating investments, and opportunistic global credit.

- High Income Model: Australian short-duration bonds, and larger allocations than in the Growth Model to global income-generating investments and opportunistic global credit.

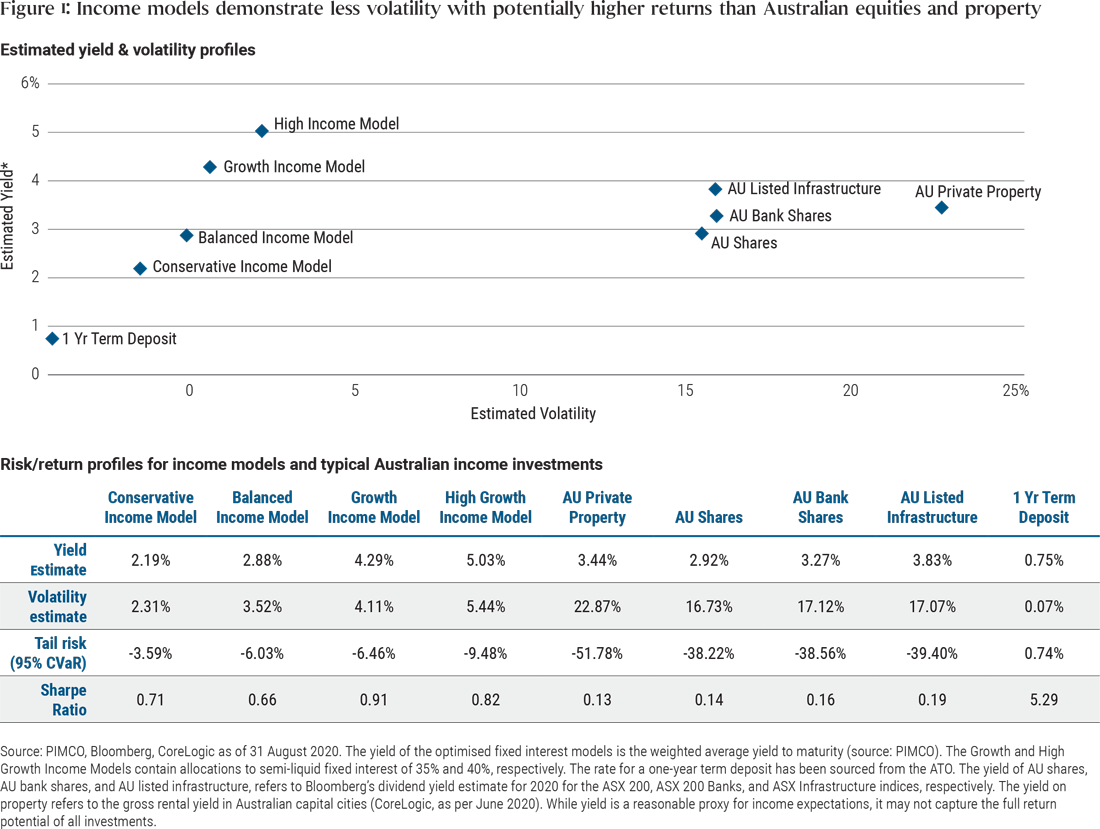

As Figure 1 shows, all of the income models demonstrate lower volatility than Australian equity and property investments. For more risk-conscious investors, our analysis estimates that a conservative income portfolio would outperform term deposits by more than 1 percentage point each year, thereby protecting purchasing power, while modestly increasing annualized volatility by 2 percentage points.

For investors prepared to assume more risk, our analysis estimates that by investing in a High Income or Growth Income portfolio, investors could achieve expected total returns greater than 5%. This is higher than our estimate for Australian equities, yet demonstrates only a third of the volatility and a quarter of the left tail risk as Australian equities or property investments (see Figure 1).

Figure 1: Income models demonstrate less volatility with potentially higher returns than Australian equities and property

Click to enlarge

Diversification can lead to better income outcomes

Australian investors have historically been willing to take on more risk to derive greater levels of income. While the current environment has placed enormous pressure on some of the traditional sources of income – equities, property and term deposits – all is not lost. For those seeking steady income as well as capital preservation, income-focused fixed interest funds can offer an alternative that matches an investor’s income objectives and risk tolerances by deriving that income from a diversified pool of assets.

Invest with the worlds premier fixed income manager

Want to find out how fixed income can play a role in your portfolio? Hit 'contact' to get more information, or click here to learn more about PIMCO's credit solutions and latest views on opportunities in the credit market.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Robert co-oversees the portfolio management teams in Asia. Previously, he was a portfolio manager in Munich and head of the European investment grade corporate bond team. He has 35 years of investment experience.

........

Past performance is not a reliable indicator of future results. Interests in any PIMCO fund mentioned in this publication are issued by PIMCO Australia Management Limited ABN 37 611 709 507, AFSL 487 505 of which PIMCO Australia Pty Ltd ABN 54 084 280 508, AFSL 246 862 is the investment manager (together PIMCO Australia). This publication has been prepared without taking into account the objectives, financial situation or needs of investors. Before making an investment decision investors should obtain professional advice and consider whether the information contained herein is appropriate having regard to their objectives, financial situation and needs. Investors should obtain a copy of the Product Disclosure Statement (PDS) and consider the PDS before making any decision about whether to acquire an interest in any PIMCO fund mentioned in this publication. The current PDS can be obtained via www.pimco.com.au. This publication may include economic and market commentaries based on proprietary research, which are for general information only. PIMCO Australia believes the information contained in this publication to be reliable, however its accuracy, reliability or completeness is not guaranteed. Any opinions or forecasts reflect the judgment and assumptions of PIMCO Australia on the basis of information at the date of publication and may later change without notice. These should not be taken as a recommendation of any particular security, strategy or investment product. All investments carry risk and may lose value. To the maximum extent permitted by law, PIMCO Australia and each of their directors, employees, agents, representatives and advisers disclaim all liability to any person for any loss arising, directly or indirectly, from the information in this publication. No part of this publication may be reproduced in any form, or referred to in any other publication, without express written permission of PIMCO Australia. PIMCO is a trademark of Allianz Asset Management of America L.P. in the United States and throughout the world. © PIMCO, 2019

1 topic

Robert co-oversees the portfolio management teams in Asia. Previously, he was a portfolio manager in Munich and head of the European investment grade corporate bond team. He has 35 years of investment experience.

Expertise

Robert co-oversees the portfolio management teams in Asia. Previously, he was a portfolio manager in Munich and head of the European investment grade corporate bond team. He has 35 years of investment experience.

Expertise

Comments

Comments

Sign In or Join Free to comment