Aussie dollar's wildest week since GFC

Sean Callow

Westpac Bank

A week is a long time in politics and certainly in FX markets. Last week the US Dollar Index was close to 18 month lows, undermined by the rapid spread of Covid-19 in the US where preparation was clearly too slow and markets were pricing in aggressive Fed easing, removing much of the US dollar’s yield advantage. But today the US dollar is at its strongest levels in 3 years.

The greenback’s surge comes despite the Fed delivering early on rate cut expectations, making its announcement on Sunday US time, feeling the need to act 3 days ahead of their scheduled meeting. The FOMC cut its Fed funds rate by 100 basis points to 0.00-0.25%, back to its GFC low. In addition, the Fed pledged to buy at least $700bn in Treasuries and agency mortgage-backed securities to quote “support the smooth functioning of markets.”

So the US dollar has shed much of its substantial yield premium over other G10 currencies, yet it is up against all of them over the week, even the safe havens Japanese yen and Swiss franc. Emerging market currency falls extend to around 9%.

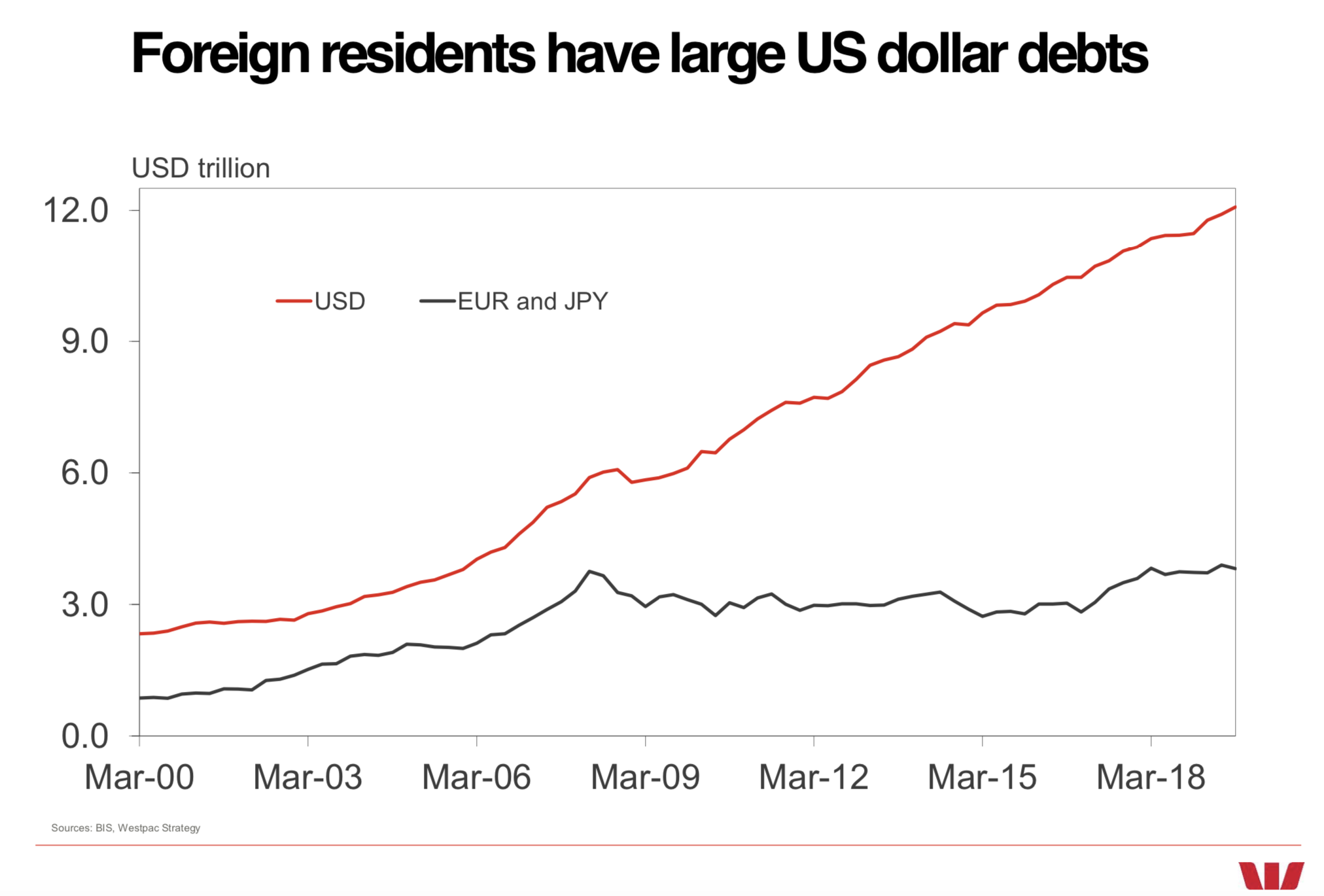

Such price action suggests significant market stress, particularly on the wide range of entities outside the US that have borrowed in US dollars. Central banks this week took steps to “ease strains in global funding markets” but the Covid-19 crisis will cause turmoil in a range of markets for some time to come.

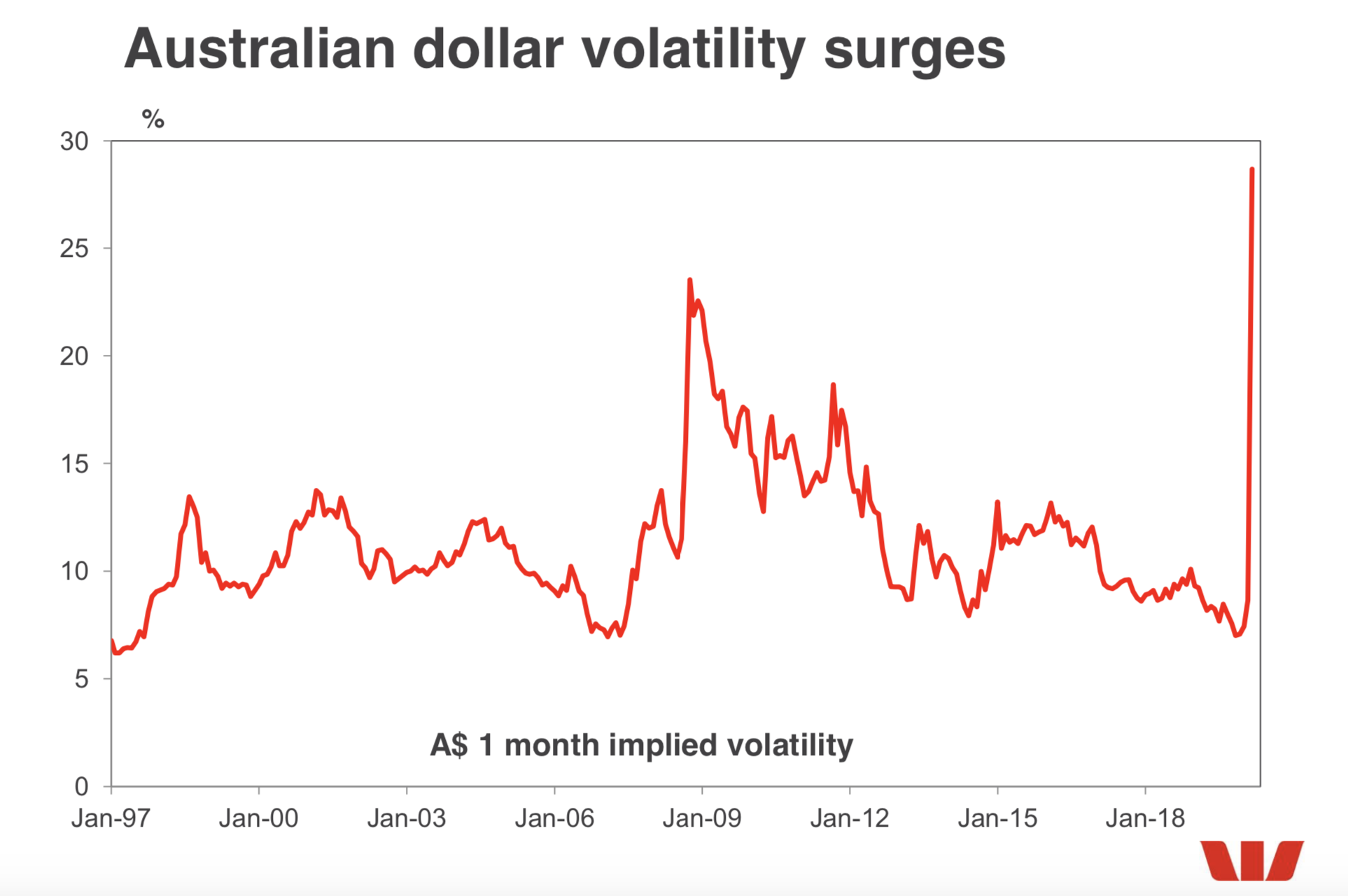

The Australian dollar has had a wild week, especially on Thursday when it traded a 4 ½ cent range before closing only slightly lower. This helped drive Aussie dollar 1 month volatility to its highest levels since the depths of the global crisis in 2008.

But while the Aussie has moved sharply in both directions, overall it has succumbed to the US dollar surge and deepening concerns over both Australia’s and the global economies. The Aussie is down almost 8% over the week, including a low of 0.5510, its weakest point since October 2002.

The extent of the Aussie’s depreciation may be excessive, given China’s continuing recovery from the virus, presenting hope for regional growth and Australian commodity exports in coming months.

Short term however, after this week’s brutal price action, it is hard to call a low for the likes of the Aussie, Kiwi and British pound. This week sterling slumped to lows since 1985.

RBA governor Lowe was asked whether the bank might intervene in FX markets given the steep plunge of recent days. Lowe said intervention was possible if markets were dysfunctional, as was the case in the GFC, but that he didn’t regard current FX conditions as worrisome.

The RBA was instead focused on supporting the Australian economy by delivering what appears to be its final rate cut, to a 0.25% cash rate, along with a new target for the 3 year Australian government bond yield, also 0.25%. This was accompanied by a new term funding facility to help banks boost business lending.

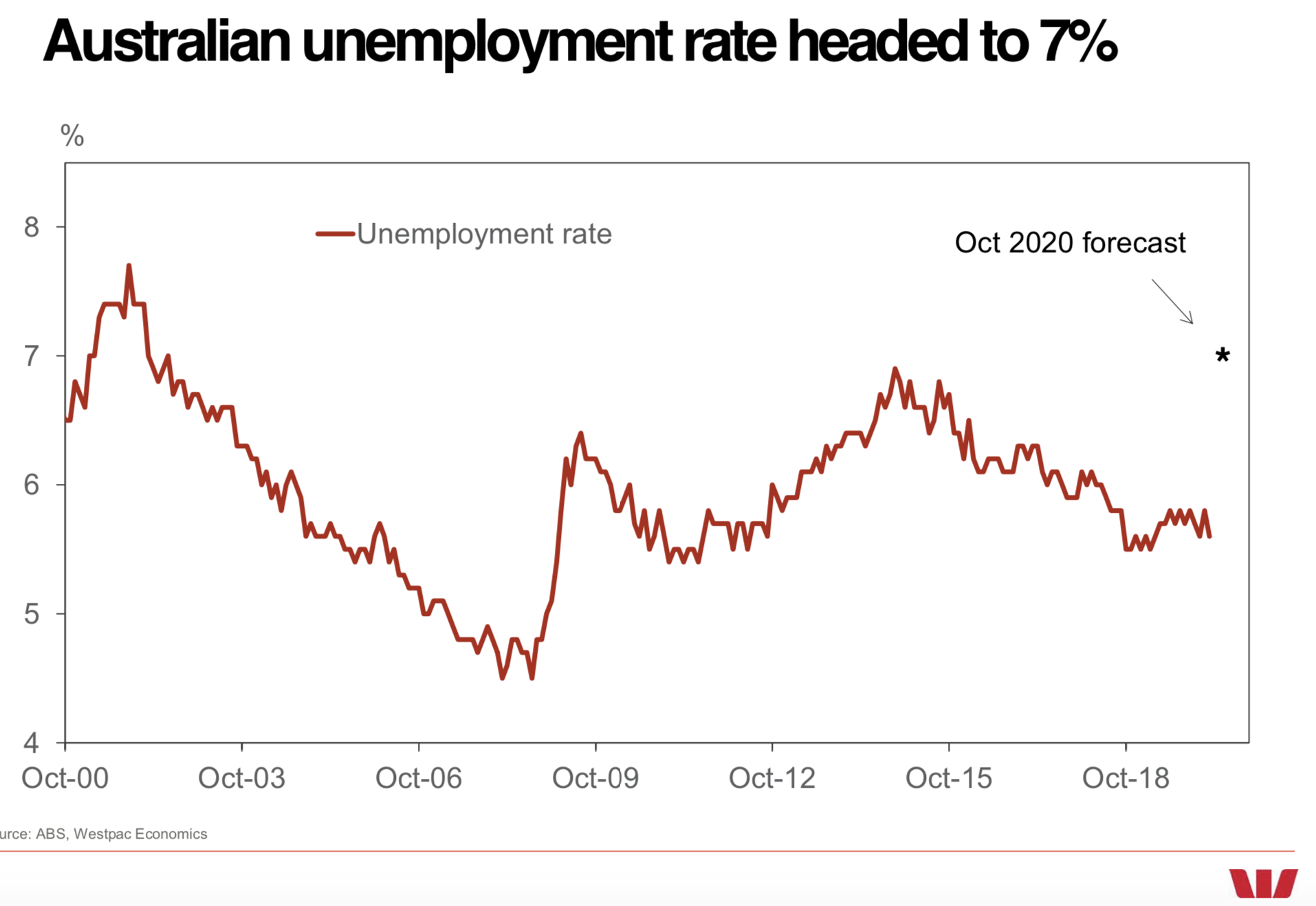

Almost lost in the market volatility was Australia’s February labour force data, which showed a drop in the unemployment rate to 5.1%. Unfortunately Westpac expects unemployment to surge to 7% by October.

In the week ahead, markets will keep monitoring the daily barrage of global news on coronavirus cases, travel restrictions, business closures et cetera. The data focus is on timely indicators such as sentiment surveys and US weekly jobless claims.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Sean Callow is Westpac Bank's Senior Currency Strategist, based in Sydney. Sean focuses on the Australian dollar and other G10 and Asian currencies. He has worked in strategy and economics roles in New York, London, Singapore and Melbourne.

1 topic

Sean Callow

Senior Currency Strategist

Westpac Bank

Sean Callow is Westpac Bank's Senior Currency Strategist, based in Sydney. Sean focuses on the Australian dollar and other G10 and Asian currencies. He has worked in strategy and economics roles in New York, London, Singapore and Melbourne.

Expertise

Sean Callow

Senior Currency Strategist

Westpac Bank

Sean Callow is Westpac Bank's Senior Currency Strategist, based in Sydney. Sean focuses on the Australian dollar and other G10 and Asian currencies. He has worked in strategy and economics roles in New York, London, Singapore and Melbourne.

Expertise

Comments

Comments

Sign In or Join Free to comment