Australian Banks: Are we there yet?

With Australian Banks representing 17% of the S&P/ASX 300 Index, most Australian investors are interested in the outlook for Australian Banks. In the last 5 years the pain associated with owning Australian banking shares has been pronounced with the sector underperforming the broader market by 45%. The sector has come under pressure on a range of fronts including greater regulation and scrutiny, slowing loan growth, slowing housing market, the royal commission and most recently COVID-19. In this monthly note we take a closer look at the outlook and opportunity set for the Australian Banking sector. We ask the question “Are we there yet?”

The continued underperformance of the Australian banks has created some medium term valuation support for the sector. Figure 1 below highlights the 12 month forward price to earnings multiple for the Australian banking sector relative to history. As illustrated it is currently trading below its long term average.

Figure 1. Australian Banking index valuations as represented by the forward price to earnings ratio

Source: Thomson Reuters, State Street Global Advisors as at 30 April 2020. P/E = Price to Earnings Ratio Past performance is not a reliable indicator of future performance. This information should not be a recommendation to buy or sell any security or sector shown. It is not known whether the sectors shown will be profitable in the future.

Further when we consider a range of valuation measures relative to the market and peer stocks we agree the sector does offer medium term value. As at 30 April 2020 we give the Australian banking sector a value score of 70 out of 100. Of course value is only one of many considerations and in order to assess the return and risk of the sector we must consider the quality of the banks and the outlook as well as the risk profile.

COVID-19 impacts cut deep, pressuring capital and increasing risks

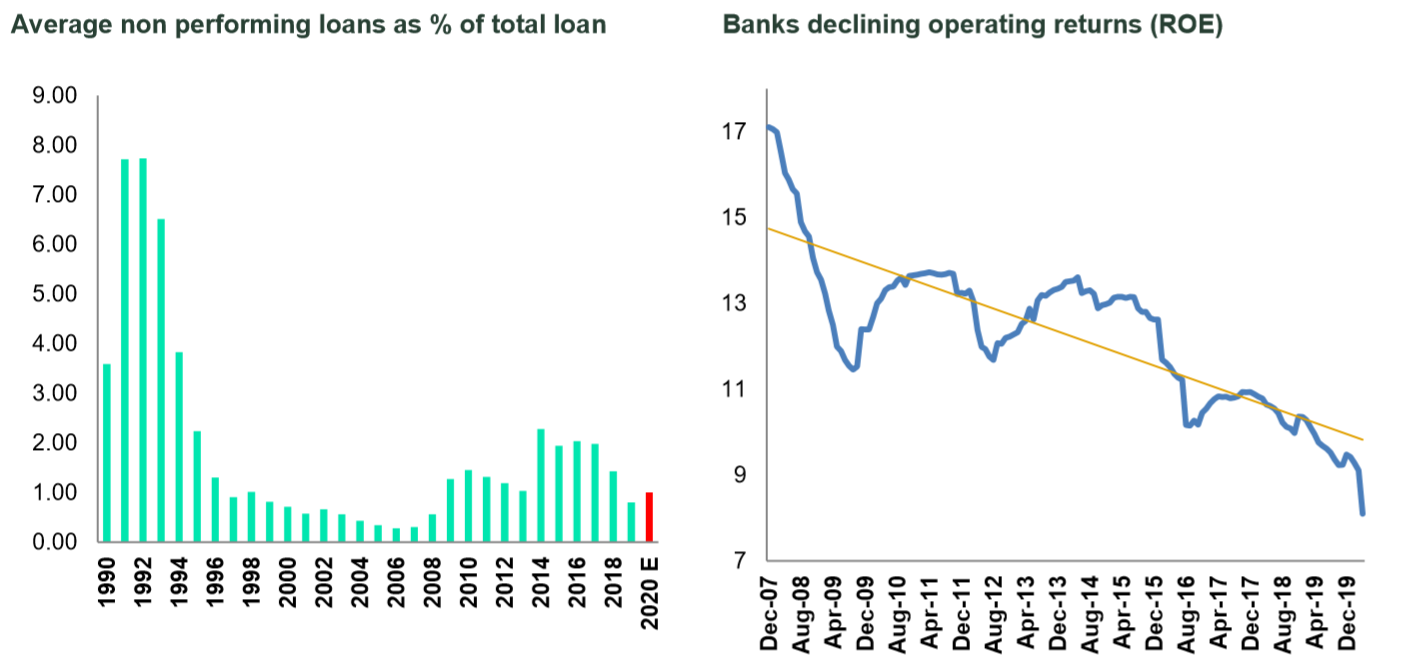

As we know COVID-19 is having significant impacts on the economy, slowing economic growth and increasing unemployment which is placing financial stress on households and businesses. In this difficult economic environment the banks have provisioned for increased impairment charges. Currently the banks are provisioning for increasing impairments in the order of 1% of total loans. At these levels the impact should be contained but should expectations for economic growth deteriorate then further provisions will be required which will put downward pressure on earnings, dividends and capital. APRA has already flagged that the banks can have some temporary flexibility in terms of their capital ratios and some have already indicated they are likely to utilise this flexibility. Figure 2 below highlights the expectations for non-performing loans for the big four banks compared to the last 30 years.

Figure 2. Non Performing loans and the declining return on equity for the Banks

Source: Thomson Reuters, State Street Global Advisors as at 30 April 2020. ROE = Return on Equity Past performance is not a reliable indicator of future performance. This information should not be a recommendation to buy or sell any security or sector shown. It is not known whether the sectors shown will be profitable in the future. 2020 E = estimate only, estimated by the Australian Banks Q3 2020 trading updates as at 15 May 2020. Forward estimates are based on certain assumptions and analysis made by the provider. There is no guarantee that the estimates will be achieved.

Prior to COVID-19 the banks were already seeing lower declining return on equity. A combination of greater regulation and higher capital requirements, lower loan growth, declining interest rates and increased competition has contributed to lower operating returns for Australian banks. How likely are those trends to reverse in the current environment?

Operating environment remains negative

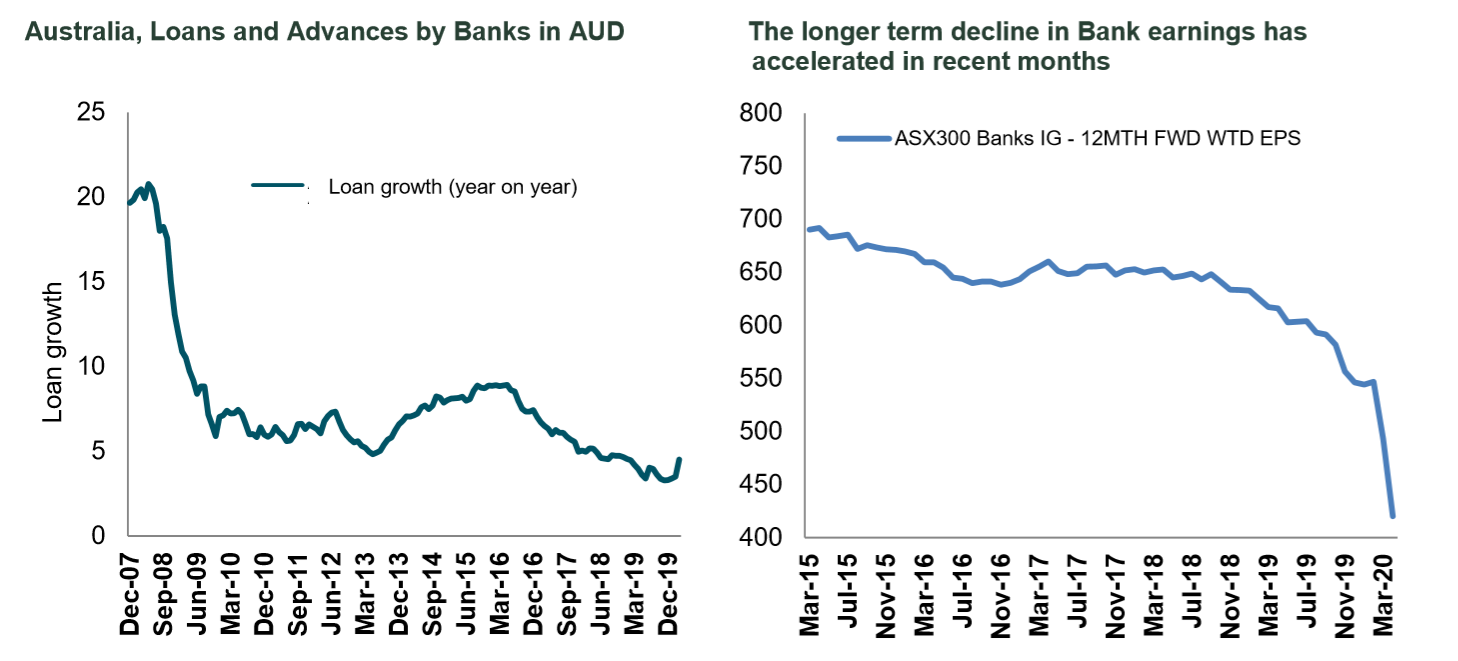

The current environment remains difficult for the banks globally and Australian banks are no exception. Lower rates put downward pressure on net interest margins. Loan growth has stepped down in recent years and continues to be significantly lower than prior periods (see figure 3 below). Interestingly loan growth did pick up temporarily in March due to many businesses drawing down on credit facilities to sure up their liquidity positions. Not the reason you want loan growth to increase!

Figure 3: Historical non-performing loans and the declining return on equity for the banks

Source: Thomson Reuters, State Street Global Advisors as at 30 April 2020. Past performance is not a reliable indicator of future performance. This information should not be a recommendation to buy or sell any security or sector shown. It is not known whether the sectors shown will be profitable in the future.

With economic activity subdued, the majority of households and corporates are less likely to take on new debt obligations. Should house prices decline further we would anticipate this to place downward pressure on loan growth. In the current environment it is less palatable for the banks to drive lower expenses with reductions in staff especially as they are currently experiencing a higher level of staff servicing from existing customers.

The Bottom Line

The underperformance of the banks has opened up some medium term valuation return potential but we assess that it is still too early at this point in time. Are we there yet? Sorry, not yet. The economic back drop has deteriorated and is especially uncertain and will likely flow through to negative news with regards to operating returns, greater loan loss provisions and pressure on lower dividends. Until sentiment stops deteriorating it will be difficult to see a sustained re-rating for Australian Banking stocks.

Learn more

Stay up to date with our latest thoughts by clicking follow below and you'll be notified every time we post content on Livewire.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

........

Issued by State Street Global Advisors, Australia Services Limited (AFSL Number 274900, ABN 16 108 671 441) (“SSGA, ASL”). Registered office: Level 14, 420 George Street, Sydney, NSW 2000, Australia · Telephone: +612 9240-7600 · Web: www.ssga.com. State Street Global Advisors, Australia, Limited (AFSL Number 238276, ABN 42 003 914 225) (“SSGA Australia”) is the Investment Manager. Investors should read and consider the relevant Product Disclosure Statement (PDS) for a Fund carefully before making an investment decision. A copy of SSGA’s Managed Fund PDSs are available at www.ssga.com.au This general information has been prepared without taking into account your individual objectives, financial situation or needs and you should consider whether it is appropriate for you. You should seek professional advice and consider the product disclosure document, available at ssga.com, before deciding whether to acquire or continue to hold units in the Funds. The views expressed in this material are the views of the SSGA Australian Active Quantitative Equity Team through the period ended 8 April 2020 and are subject to change based on market and other conditions. The information provided does not constitute investment advice and it should not be relied on as such. All material has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. This document contains certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Volatility management techniques may result in periods of loss and underperformance, may limit the Fund's ability to participate in rising markets and may increase transaction costs. Actively managed funds do not seek to replicate the performance of a specified index The fund is actively managed and may underperform its benchmarks. An investment in the Fund is not appropriate for all investors and is not intended to be a complete investment program. Investing in the Fund involves risks, including the risk that investors may receive little or no return on the investment or that investors may lose part or even all of the investment. Standard & Poor’s and S&P are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”) and Dow Jones is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”) and have been licensed for use by S&P Dow Jones Indices LLC and sublicensed by SSGA. The S&P/ASX 300 Index is a product of S&P Dow Jones Indices LLC, and has been licensed by SSGA. SSGA’s Funds are not sponsored, endorsed, sold or promoted by S&P Dow Jones Indices LLC, Dow Jones, S&P, their respective affiliates, and none of S&P Dow Jones Indices LLC, Dow Jones, S&P, nor their respective affiliates make any representation regarding the advisability of investing in such product(s). Investing involves risk including the risk of loss of principal. Risk associated with equity investing includes stock values which may fluctuate in response to the activities of individual companies and general market and economic conditions. This material should not be considered a solicitation to apply for interests in the Funds and investors should obtain independent financial and other professional advice before making investment decisions. There is no representation or warranty as to the currency or accuracy of, nor liability for, decisions based on such information. The whole or any part of this work may not be reproduced, copied or transmitted or any of its contents disclosed to third parties without SSGA Australia’s express written consent.

1 topic

4 stocks mentioned

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Investment Management

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Head of Portfolio Management – Australia, Active Quantitative Equity

State Street Investment Management

Bruce is Head of Active Quantitative Equity - Australia, for State Street Global Advisors. He has over 20 years' experience, covering Australian and global equites, long and short equities as well as global macro strategies.

Comments

Comments

Sign In or Join Free to comment