Australian Credit is strapped to a 60% V-Shaped Rocket

The Australian Treasury expects that 60% of the economy can be recovered once we achieve Stage 3 of National Cabinet’s re-opening plan. This correlates with the RBA’s recent ‘Upside Scenario’ and provides a safe margin away from the most severe downside scenarios used by our major banks for stress testing purposes. When the recent consumer confidence figures are also considered, Australia is looking at a healthy recovery, at least in the early stages. The Australian non-financial corporate bond and RMBS markets don’t seem to have fully realised this as yet.

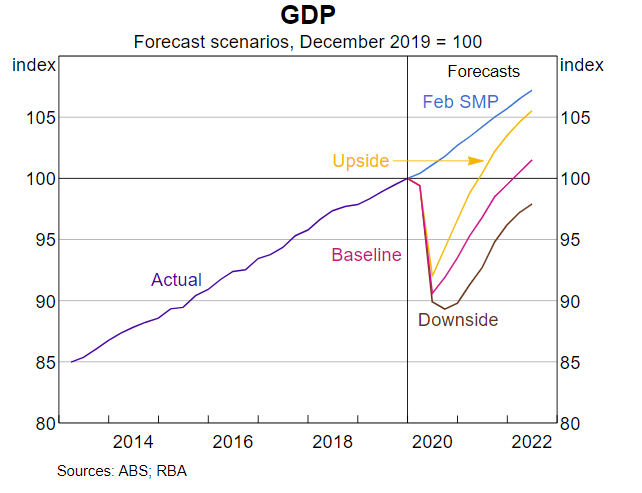

The RBA and the Upside Scenario

The RBA released a set of plausible economic scenarios in its recent Statement of Monetary Policy which was released on May 8th. The Baseline scenario envisaged that most restrictions would be lifted by the September quarter. The Upside scenario envisaged a faster recovery where most containment measures were phased out over the coming months:

The day after the SoMP was released, National Cabinet issued a roadmap to re-open the economy in 3 steps. PM Scott Morrison indicated that consideration for each progressive step would be separated by approximately 3 weeks. This timeline pointed to most restrictions being lifted by July. The plans suggested that the remaining restrictions would be related to large gatherings and international travel. The 4sqm rule would remain a feature.

Estimates were provided in relation to the economic impact of each stage. The announcement converted the RBA’s Upside Scenario into the new Baseline.

The Ministerial Statement

Whilst the Federal Budget was delayed, Treasurer Josh Frydenberg made a Ministerial Statement on May 12th where he outlined the state of the economy and elaborated further on the economic estimates. Under Step 3 arrangements, approximately 850k people are expected to return to work. This compares to the projected unemployment level of 1.4m as at 30 June, a figure which would be even higher were it not for a large number of discouraged workers who will leave the workforce entirely.

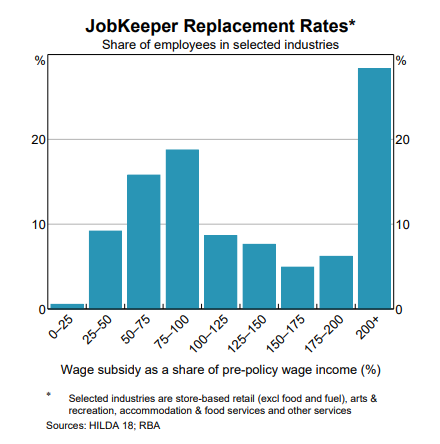

Economic activity at Step 3 would recover approximately 60% of GDP per month lost through the impact of COVID, which is estimated at $4bn a week. Even so, many businesses will continue to be supported by Job Keeper which has more than 5.5m workers enrolled, many of whom are earning more than they had prior to the pandemic:

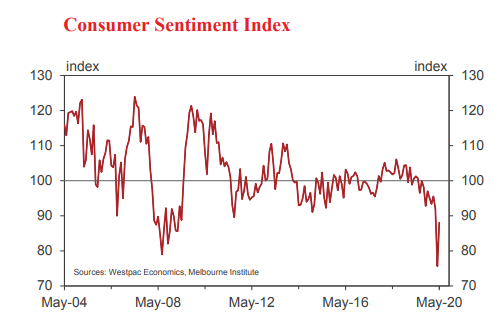

Consumers are much more optimistic

In surveys taken by Westpac and the Melbourne Institute, prior to the release of the National Cabinet’s roadmap, a significant recovery in sentiment was noted:

The index has retraced most of the sharp downwards move which was recorded in April. Over the month, consumers became much more optimistic about economic conditions in the coming year. They are more likely to buy a major household item and far more inclined to buy a house.

Given this pent up demand, it is likely that consumer demand will spring back along a V-Shape as envisaged by the RBA’s Upside scenario, which approximately encapsulates the Treasurer’s Statement.

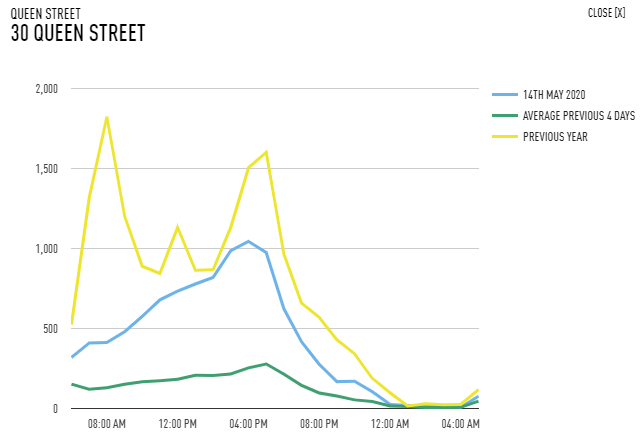

We can look to New Zealand for an early indication of the kind of optimism we may encounter here. They have also successfully contained COVID at this time. Their restrictions were more onerous, but they have re-opened to a level which Australia does not contemplate doing for a few weeks. This makes New Zealand an excellent lead indicator of what pent up demand may exist and how consumers may react.

The following shows foot traffic statistics in the shopping district of Auckland. In New Zealand, they clearly want to shop again. I expect Australians will be similarly inclined:

If Australian consumers do act in this way, it would be consistent with the way in which SARS impacted some Asian economies. In the case of SARS, these economies experienced a three month period of weakness before recovering almost all of it in the subsequent three months. COVID will be different as the pandemic will likely remain with us for some time yet, but we also have much more significant official support. The longer term implications are yet to be settled. However, the shorter term implications appear relevant. A 60% V-shaped recovery for the balance of 2020 looks viable.

Unemployment and Housing Prices

Based on the Treasury and RBA figures, unemployment will likely be around 8% at year end. The RBA scenario suggest that this may fall below 6% by the end of 2021, which would be a remarkable outcome if so. Nonetheless, the forecast level is clearly an elevated figure and more credit-related stresses than normal will be evident.

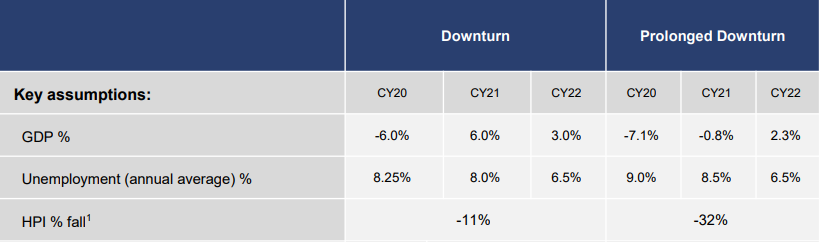

What movements in house prices might represent plausible outcomes with this in mind? With banks reporting their earnings results recently, we can draw upon their scenario stress tests to provide some guide about the downside risk. These are the CBA stress test scenarios:

Source: CBA

The projected economic outcomes are to the optimistic side of CBA’s ‘Downturn’ scenario. It suggests that a large scale housing price (HPI) downturn is not expected. This general observation is true of the other banks as well.

The ‘Prolonged Downturn’ scenario is consistent with a 2nd wave onset which requires our economy to remain at something like step 2 (restricted work, gatherings of 20, some interstate travel) through to the end of next year.

Outlook for Residential Mortgage Backed Securities

Although RMBS and structured mortgages have attained a poor reputation from the GFC, the market has performed well in Australia since inception. Nonetheless, one of the outcomes of the GFC was that the subordination levels and other terms required to support a rating were increased.

When running stress tests through recent structures brought to the market, we find that all rated notes remain whole under conditions which are worse than even the CBA ‘Prolonged Downturn’ scenario. Despite this, the market requires the support of facilities operated through the Australian Office of Financial Management to provide liquidity in order to facilitate ongoing loan creation in the non-bank market.

Whilst issuance activity has been impaired, necessitating official intervention, AAA-rated notes on non-conforming mortgage pools were placed very recently and still offer a healthy margin of 2.75% per annum over swap. This compares to 1.75% in January. BBB-rated notes currently offer 5.75% (4.00% in January). Transactions involving conforming pools would be at slightly lower however no transactions have recently come to market.

For comparison, the senior unsecured bank floating rate notes currently trade at a margin of approximately 80bps. These are generally rated AA- for major banks.

To some extent the wider spreads on RMBS may reflect uncertainty as to the extent to which mortgagees can resume scheduled payments after the period of COVID relief has passed and the rate at which loans will be paid down. Pricing has also been impaired by the exit of transient foreign holders and uncertainty relating to near term demand on the part of domestic institutional participants. Nonetheless, if even the most severe bank scenarios are insufficient to impair the credit performance of these pools, spreads look over-compensated.

Outlook for Corporate Credit

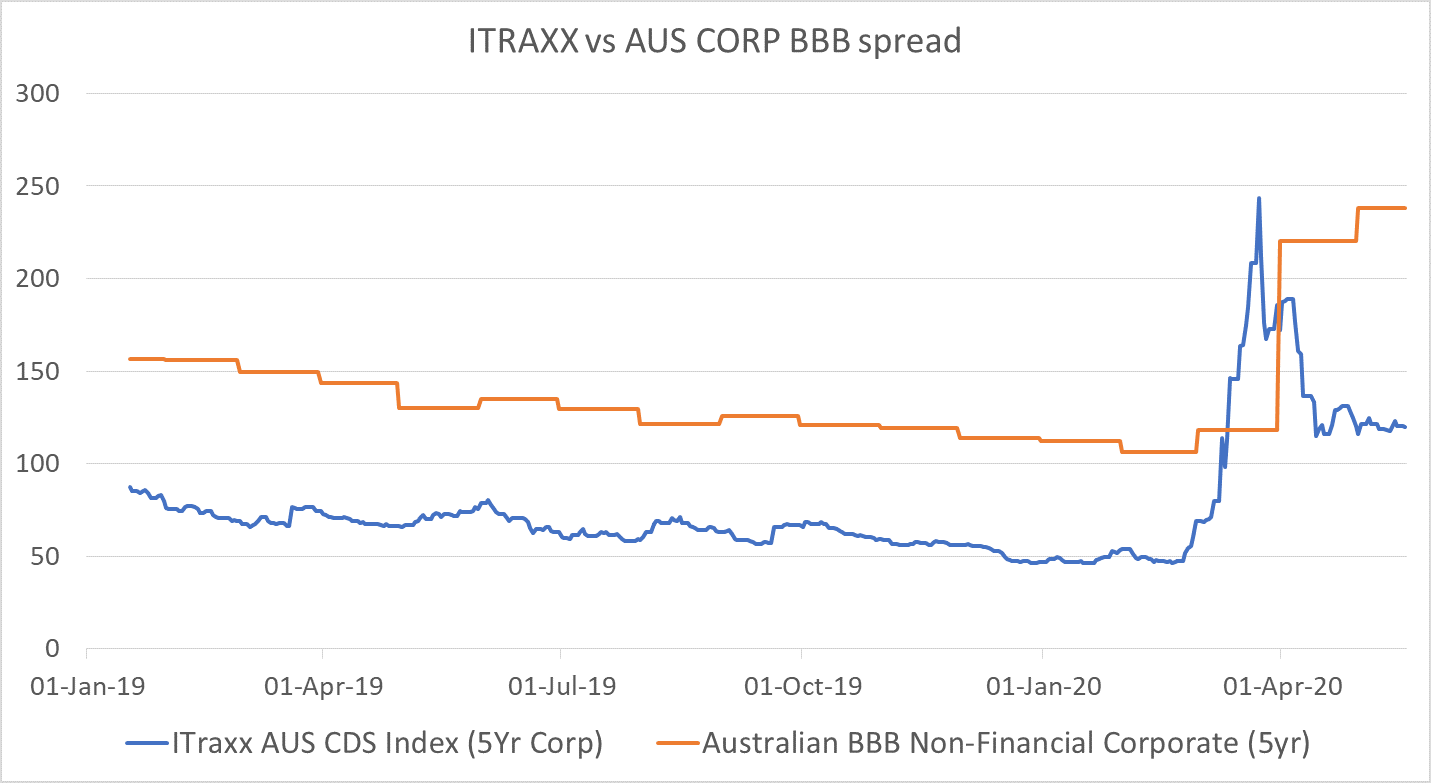

The pricing of bank-issued credit has significantly recovered from the COVID lows. However other investment grade Australian corporate bonds have not recovered as much as might be expected.

Whilst the estimated default risk, as encapsulated in the pricing of credit default swaps, has declined significantly for BBB-rated Australian corporate credit, the prices for those securities have not adjusted:

Source: Author

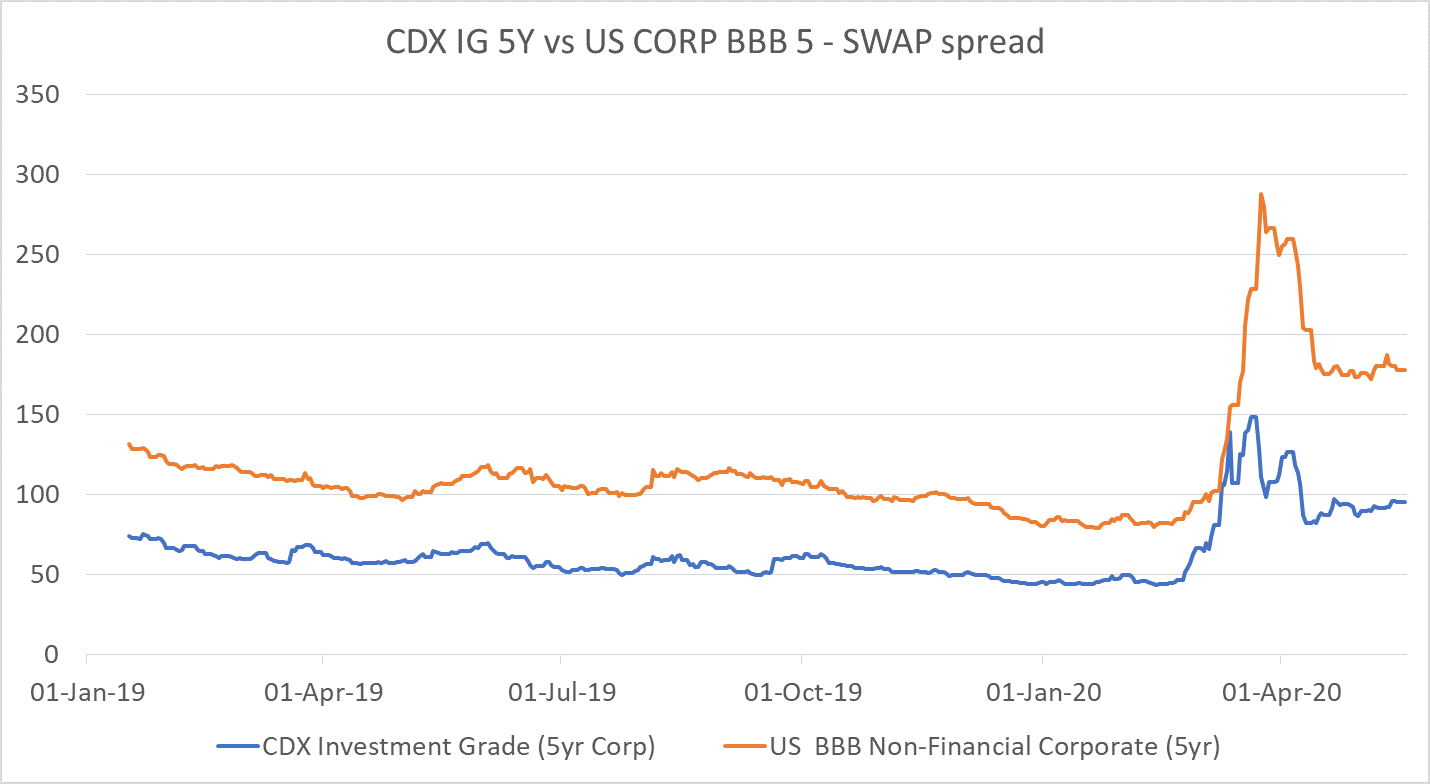

In other jurisdictions like the US and Europe, the central banks added investment grade credit directly to their balance sheets which provided more confidence in market liquidity and helped narrow spreads as default risk receded. For example, the spreads on US BBB-rated corporate debt has moved much more in unison with estimated default risk:

Source: Author

Whilst the spreads on investment grade non-financial corporate bonds in some other major jurisdictions have narrowed along with the estimated default risk, Australia’s market has not done so. In contrast to other central major banks, RBA Governor Lowe has expressed reticence to impact pricing beyond government related debt. Although the acceptable collateral for bank repo facilities was recently expanded to include non-financial corporate investment grade credit, this has had a very small impact on market pricing so far.

Australian non-financial corporate credit continues to trade wide despite the improved outlook. This could be considered as an overcompensated liquidity premium or a significant buffer against an unexpected deterioration in default risk. It will be eroded eventually.

Summary

Australia’s 3-step recovery plan is expected to produce a set of economic outcomes which were much more favourable than might have been imagined just a month ago. Consumers are looking forward to the re-opening of our economy and, if New Zealand and recent surveys are any guide, will spend from day 1. The Treasurer expects 60% of the economic impact from COVID can be recovered at Step 3 of the re-opening roadmap, which is due to be implemented by July. If accurate, Australian RMBS and non-financial corporate credit look exceptionally good value.

Never miss an update

Enjoy this wire? Hit the ‘like’ button to let us know.

Stay up to date with my current content by

following me below and you’ll be notified every time I post a wire

Ken is a partner at Realm Investment House. He was Head of Investment Research at Mercer and Chief Investment Officer of Domestic Equities at BlackRock.

........

Disclaimer: This document should be regarded as general information only rather than advice. In preparing this document, no account was taken of the investment objectives, financial situation or particular needs of any individual person. Any opinions expressed in this document are the author’s alone and may be subject to change. The information must not be used by recipients as a substitute for the exercise of their own judgment and investigation.

3 topics

Ken is a partner at Realm Investment House. He was Head of Investment Research at Mercer and Chief Investment Officer of Domestic Equities at BlackRock.

Expertise

Ken is a partner at Realm Investment House. He was Head of Investment Research at Mercer and Chief Investment Officer of Domestic Equities at BlackRock.

Expertise

Comments

Comments

Sign In or Join Free to comment